A pandemic is the extensive spread of infectious diseases over many countries and continents, resulting in significant mortalities and morbidities (Hiscott et al., 2020). For more than one year, the world has existed in uncertainty and vagueness because of the coronavirus disease. The COVID-19 pandemic has had numerous negative consequences across the globe. The unexpected and rapid spread of the disease worldwide affected countries in different ways; economically, politically, and socially. Countries enforced stringent measures such as lockdowns, travel restrictions, prohibition of celebration and social gatherings, closure of borders, closure of learning institutions, and curfews to control the rapid spread of COVID-19. PCR testing to detect the virus intensified to detect, manage, and control the spread of the disease. All these efforts were enforced with the primary objective of controlling the rapid spread and protect the human population. Although the primary role of these stringent measures was humane, the economy suffered negatively. Organizations and corporate sectors experienced adverse effects of the pandemic, including reduced functioning, uneventful closure, and losses amounting to millions (Hiscott et al., 2020). Consequently, the open organizations were forced to lay off their staff resulting in loss of jobs and income and high unemployment rates, further worsening the economy. High rates of fraud heightened during the pandemic. The following article discusses the role of internal audits during the pandemic.

COVID-19 Impacts Lifecycle

The COVID-19 pandemic created a public health crisis with adverse social and economic implications. According to the Martin et al. (2020), the number of needy people surviving with less than $1.90 per day increased by substantially throughout the world. Governments and international aid organizations had to escalate contributions to help needy people to survive the pandemic. The global economy suffered terribly because of stringent measures such as travel restrictions (Hiscott et al., 2020). The International Monetary Fund (IMF) estimated that the global economy would dip downwards by 4.4% in 2020 (Martin et al., 2020). To maximize profits, increase the confidence of stakeholders, and ensure business run, as usual, the organization had to ensure efficient and effective use of its resources.

COVID-19 and Fraud

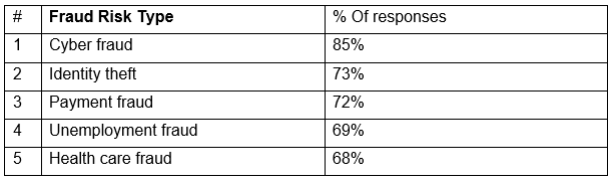

Fraud is defined as "an illegal act characterized by deceit, concealment, or violation of trust." The Fraud Triangle is a framework used to explain and infer an individual's reasons behind fraud. The framework outlines three concepts, opportunity, rationalization, and incentive, which contribute to fraud. The COVID-19 pandemic significantly influenced the increasing numbers and rate of fraud reported worldwide. Of the 1,712 survey responses collected by the Association of Certified Fraud Examiners (ACFE), 79% of the participants indicated that the pandemic was to blame for the escalation of fraud cases (Rashidian et al., 2012). According to the ACFE report, the following five categories of fraud risks were common until November 2020:

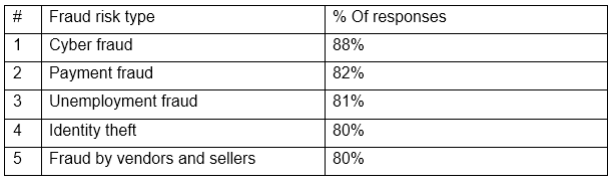

During the COVID-19 pandemic, the Association of Certified Fraud Examiners survey indicated that the following were the commonest fraud risk type for the next 12 months:

The survey above from Association of Certified Fraud Examiners (ACFE) showed categories of fraud risks that can affect organization operations. With such knowledge, organizations can detect, investigate, and prevent these frauds from materializing.

COVID-19 and Internal Audit Activity

Internal audit is an independent and objective activity that adds value to the organization by providing assurance and interventions to improve governance, risk management, and internal controls. Internal audit plays a fundamental role in protecting organizational assets and properties. The audit is vital in ensuring that organizations are effectively meeting their objectives and goals. The Three-Line Model clarifies the role of internal audit in the third line as independent assurance activity (Hut-Mossel et al., 2017). The Chief Audit Executive (CAE) communicates and reports directly to the governing body about audit findings within the third level. With the COVID-19 pandemic becoming a menace, internal audits can be pivotal in cushioning organizations against risks, including fraud. Internal audit departments have the responsibility of dealing with threats created by this crisis in the following ways:

Detect High-Risk Areas

According to Dirani et al. (2020), internal auditors (IAs) should be alert to potential risks, which can affect organizations. IAs are supposed to think ahead, weigh on how the pandemic affects organizations and which areas are weak points that should be addressed or be prioritized. Internal audit departments must identify and assess the high-risk areas and topics brought about by the COVID-19 pandemic. Internal auditors should communicate directly with the top management about the identified high-risk areas.

Fraud Investigation

Based on the ACFE report, fraud appetite increased because of the pandemic and its negative consequences. Internal auditors should have adequate facts about possible frauds that might be committed through risk assessment. As mentioned in the standard (1210.A2) of International Standards for the Professional Practice of Internal Auditing, “internal auditors must have sufficient knowledge to evaluate the risk of fraud and how the organization manages it” (NCA Self-Study Committee, 2020) internal audit departments have to be ready to evaluate internal controls for fraud and anti-fraud systems in the organization.

Clear Communication

Internal auditors have to ensure that organizations have a straightforward procedure to share all necessary information, facts, figures, and data regarding their findings. Flexibility and accurate sharing of information with all employees prevent the circulation of fake information that can disrupt business in a pandemic.

Commit to Ethic Management System

All organizations should have an ethical management system or committee that oversees the implementation of rules, regulations, values, and norms that govern the running of the organizations. This system attempts to reduce the rate of corruption and degeneration in the organization. Therefore, internal auditors should ensure that all staff are committed to the organization’s code of conduct to shrink and eliminate unethical behaviors. Internal auditors should work closely with the ethics committee to ensure that employees and employers maintain high ethical standards preventing unhealthy behaviors such as fraud.

Conclusion

The COVID -19 pandemic has both positive and negative implications. Businesses and organizations have to learn from this pandemic and develop measures that cushion them against uncertainties and risks, including fraud. Internal audit departments are responsible for ensuring organizations are prepared for risks such as pandemics and financial constraints. Internal auditing activities should focus on preemptive actions and tasks to protect the organization against opposing forces that disrupt business.