Mr. Gilbert Simson Gattang,

Protocol Analyst, Leadership Secretariat Bureau

Mr. Hendru Priasukma,

competency development analyst

Mr. Eko Nugroho,

junior auditor in BPK

Abstract

The rapid advancement of Artificial Intelligence (AI) has significantly influenced the auditing sector, particularly within Supreme Audit Institutions (SAIs). This paper explores the implementation of AI in the audit process from the perspective of auditors at Indonesia's Audit Board (BPK RI). Through qualitative descriptive analysis and survey data, the study examines how AI enhances audit efficiency, effectiveness, and decision-making. However, challenges such as lack of understanding, regulation, and infrastructure are identified as barriers to adoption. The findings underscore the necessity for comprehensive training, regulatory frameworks, and infrastructure development to unlock AI's potential fully. The study also highlights the strategic role of AI in achieving sustainable development goals, improving audit accuracy, and enhancing the quality of audit reports. The paper concludes with recommendations for overcoming challenges and maximising AI benefits for auditing practices at BPK RI and other SAIs globally.

Keywords

Artificial intelligence, Auditing, BPK RI, Challenges, Opportunities.

Introduction

The ongoing transformation of Supreme Audit Institutions (SAIs) external environment is changing the demands and expectations of its stakeholders. The changing environment triggered by technological advancements, increased demand for accountability, and transparency, means a change in the way auditing is done (Otia & Bracci, 2022). One of the most significant triggers in influencing changes in the audit field is the introduction of Artificial Intelligence (AI) in the audit process. The development of AI has brought significant changes in various aspects of life. With technological advancements, AI is increasingly sophisticated and capable of performing tasks that previously could only be done by humans. This development of AI opens up new opportunities and challenges in various sectors, including the auditing sector (AICI, 2024).

Nowadays, the use of AI in audit process is proactively encouraged by the SAIs around the world. The second SAI20 Summit held at Goa under the aegis of India’s G20 Presidency has called upon the Supreme Audit Institutions (SAI) to take measures for suitable integration of artificial intelligence (AI) in audit processes and tasks for improved audit efficiency and effectiveness (Panaji, 2023). At the XXIII International Organization of Supreme Audit Institutions (INTOSAI) Congress, the Moscow Declaration also encourages Supreme Audit Institutions (SAIs) to nurture the auditors of the future, who can employ data analytics, Artificial Intelligence (AI) tools and advanced qualitative methods; enhance innovation; and act as strategic players, knowledge exchangers and foresight producers (Dotel, 2020).

In 2019, during the International Congress of Supreme Audit Institutions (INCOSAI), INTOSAI founded the Working Group on the Impact of Science and Technology on Auditing (WGISTA). This group assists SAIs in navigating the evolving landscape of auditing, particularly in response to emerging technologies and scientific advancements. WGISTA focuses on areas such as Blockchain, AI, machine learning (ML), data analytics, quantum computing, and 5G, helping SAIs adapt to these technological changes. (WGISTA, 2020).

The Audit Board of the Republic of Indonesia (BPK RI), as a member of WGISTA, is committed to supporting the work programs of WGISTA through the implementation of shared values and objectives, particularly those of INTOSAI. Furthermore, BPK RI's commitment to achieving the Sustainable Development Goals (SDGs) by 2030 is continually pursued through the Medium-Term Government Plan and implemented via the Strategic Plan of BPK RI.

In conducting audits on public financial governance, especially in response to the impacts of COVID-19 on economic and fiscal developments, BPK RI provides recommendations aimed at mitigating risks of losses due to ineffective public financial management amid the pandemic. This includes considerations for fiscal sustainability post-pandemic, addressing budget deficits, and implementing risk management strategies by the Government. In its audit activities, BPK RI has integrated technological advancements such as artificial intelligence, cloud computing, paperless documentation, and virtual communication and coordination. These innovations are expected to enhance business processes across all types of audits and improve the competencies of auditors, particularly in relation to Information Technology.

In the future, BPK RI will continue to advance in addressing current challenges to ensure a stronger BPK RI by adopting several key strategies. First, by producing audit results that are responsive to strategic issues of concern to stakeholders, fostering cross-sectoral and regional development synergy, and supporting the implementation of the SDGs through recommendations and opinions that offer both insight and foresight. Second, by conducting high-quality audits aligned with established standards and best practices. Third, by enhancing the effectiveness of audits through the utilisation of big data analytics. Fourth, by increasing stakeholders' trust in BPK RI's performance in preventing and combating corruption. Fifth, by providing SMART recommendations that are actionable by the audited entities and ensuring high rates of follow-up completion. Finally, by ensuring that stakeholders experience tangible impacts from the audit outcomes (BPK RI, 2020).

Considering the big and significant the use of AI is in audit sector, especially for SAIs, the issues related to the use of AI are very interesting issues to be discussed. This research paper aims to give fundamental knowledge about the implementation of AI in audit process conducted by BPK RI, especially from the perspectives of the auditors. By knowing the challenges and the future benefits, hopefully, this research paper can give some recommendations for enhancing the implementation of AI for the audit process in BPK RI and point of view for the other SAIs.

Literature Review

The Role of AI in Auditing Recently

The practice of auditing is more than a century old. Although the types and methods or models of auditing have evolved over time, the auditor community still faces significant problems. The auditor’s role in the Digital Age needs to evolve and adapt in a manner in which audits are a mechanism to identify patterns and trends from large data sets. These insights provide support for risk assessments, project scoping, and proactive and early identification of potential issues, among other things. In today’s rapidly evolving technology landscape, existing AI and ML techniques not only detect fraudulent transactions and identify high-risk issues such as unknown system activity from user endpoints, but learning models can also be built from such interventions (Menon, 2021).

Artificial Intelligence (AI) is described in the report as a technology that combines processing power with extensive access to data, enabling it to analyse large datasets and uncover patterns or anomalies. This capability allows AI to handle tasks that would otherwise be time-consuming and repetitive for auditors. In an audit, AI can be used in a variety of ways, including performing journal entry testing by identifying unusual transactions among a large pool of unstructured data and analysing those transactions for patterns and anomalies (Dennis, 2024). By automating these mundane processes, auditors are freed to focus on more critical aspects of their work, such as applying their professional skills, knowledge, and judgment. This shift not only increases efficiency but also significantly improves the overall quality of audits, allowing auditors to deliver more accurate and insightful results (CA ANZ, 2019).

However, in its implementation, the use of AI in the audit process has various advantages and challenges that must be considered.

The Challenges of AI Implementation in Audit

There are five major ethical challenges of AI-based decision-making in accounting including objectivity, privacy, transparency, accountability and trustworthiness. Related governance as well as internal and external auditing processes need to be adapted in terms of skills and awareness to ensure ethical AI-based decision-making (Lehner, Ittonen, Silvola, & Strom, 2022). There are also several obstacles to using AI in audits, such as the auditor's lack of understanding of AI technology. According to the AICPA Audit Standards Boards Technology Task Force, there are some reasons why audit teams do not use AI including Lack of Training and Infrastructure, the cost is expensive, not useful, inability to access usable client data, difficulty to use, etc (Dennis, 2024). The use of AI in auditing also has some risks such as Accuracy and Reliability, Transparency and Explainability, Security, and Data Protection (Gopal, 2024).

How to overcome the challenges?

Auditors must realise the value of AI technology, the various possibilities it unlocks, and the potential downsides of not adopting it and committing to transforming processes. The barrier to adopting technology is usually being made aware of the technology and its benefits. Educate yourself on the potential of AI to be leveraged across audit stages. Few concrete steps you could take as an auditor to get into the game such as investing in education and training, collaborating & Learning, leveraging AI tools, and maintaining data quality and privacy (Gopal, 2024). There are also challenges that need to be overcome, such as the need for auditors to develop new skills and regulatory adaptation to the use of AI in audits. (Silaen & Dewayanto, 2024).

Benefits of AI for Audit

Most organisations deem AI as crucial for external audits and highly value its automation and data analytics capabilities (KPMG, 2024). AI has the potential to significantly improve the efficiency, accuracy, and effectiveness of the audit process (Silaen & Dewayanto, 2024). According to Gopal (2024), there are also some roles of AI in the audit process including:

1. AI can help analyse historical and real-time data, Leveraging ML algorithms to identify patterns and predict potential risks allows for better audit planning;

2. AI, with Optical Character Recognition (OCR), can scan and interpret documents. It can categorise documents accurately, such as invoices, bank statements, etc;

3. AI with advanced algorithms can help with real-time insights, flagging issues, and intervention in these cases; and

4. AI-first insights can complement human insight to make more effective recommendations.

Research Methods

1. Type of Research

This research paper used qualitative descriptive analysis. Descriptive studies are undertaken to understand the characteristics of organisations that follow certain common practices (Sekaran & Bougie, 2010).

2. Type and Sources of Data

The type of data gathered in this research paper was primary data. Primary data refers to information obtained first-hand by the researcher on the variables of interest for the specific purpose of the study (Sekaran & Bougie, 2010). The sources of the data come from the auditors in BPK RI.

3. Data Collection Methods

The data collection method used in this research was a survey. The survey was conducted with the auditors in BPK RI to get their perspectives on the implementation of AI in the audit process.

4. Data Analysis

This research paper used data reduction and data display as qualitative data analysis. Data reduction refers to selecting, coding, and categorising the data. Data display refers to ways of presenting the data. A selection of quotes, a matrix, a graph, or a chart illustrating patterns in the data may help the researcher (and eventually the reader) to understand the data (Sekaran & Bougie, 2010). To make sure that the conclusions of this research paper are reliable and valid, data triangulation is used. Data triangulation means are collected from several sources and/ or at different periods. Triangulation is a technique often associated with reliability and validity in qualitative research. The idea behind triangulation is that one can be more confident in a result if the use of different methods or resources leads to the same results (Sekaran & Bougie, 2010).

Results

Demographic Overview of Respondents

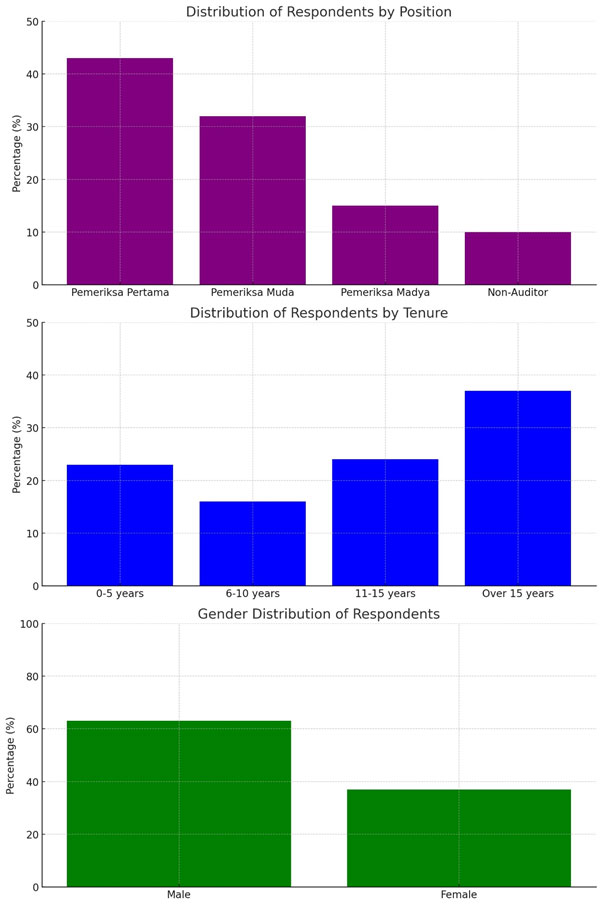

The study surveyed 100 respondents to explore their perspectives on the integration of Artificial Intelligence (AI) within the auditing processes at BPK RI. These respondents were categorized based on their roles and levels of experience within the institution, offering a diverse range of insights. The majority of the respondents held the position of Pemeriksa Pertama (43%), followed by Pemeriksa Muda (32%), and Pemeriksa Madya (15%). Additionally, 10% of the participants were non-auditor BPK employees who had been involved in auditing processes, thus providing a wider spectrum of opinions and experiences. This diversity in roles allows for a comprehensive understanding of how AI is perceived across different tiers within BPK RI, capturing insights from both more experienced auditors and those relatively new to the institution. This wide range of perspectives is crucial in presenting a nuanced view of AI’s integration in the audit field.

The respondents' tenure within BPK RI also varied considerably, with 23% having worked for 0-5 years, 16% for 6-10 years, 24% for 11-15 years, and 37% for over 15 years. These statistics indicate that the majority of respondents (61%) have over a decade of experience in the auditing profession. This longevity provides significant insight into the impacts of AI on long-established auditing practices and how these professionals view the changes brought about by new technologies. The study also revealed a gender distribution of 63% male and 37% female respondents, which provides a balanced representation of perspectives from across genders, further enriching the study’s findings.

The variation in experience levels is particularly significant when considering the integration of AI into the audit processes. As discussed in the introduction and literature review, the use of AI in Supreme Audit Institutions (SAIs) worldwide has been increasing due to the demand for greater efficiency, accuracy, and risk detection in auditing. Within BPK RI, the respondents' different experience levels serve as an important contextual factor for understanding the challenges and opportunities presented by AI. Respondents with over 15 years of experience are likely to have witnessed considerable shifts in auditing methodologies, including the transition toward AI-based processes. Their insights are valuable in highlighting how traditional auditing practices have been reshaped by AI and the extent to which these technologies have been incorporated into daily auditing operations.

Conversely, respondents with less than five years of experience may offer newer perspectives on the adoption of AI tools, particularly in terms of how these technologies are being integrated into their workflows and how the institution manages training and adaptation to AI. These varied perspectives, when analys ed through qualitative research methods, allow for a more thorough exploration of the perceived benefits and challenges associated with the integration of AI in auditing. The findings of this survey, thus, align well with the study’s analytical approach, providing a well-rounded understanding of how AI is impacting auditing practices within BPK RI.

Demographic Overview of Respondents

Understanding Respondents' Awareness of AI in the Audit Process

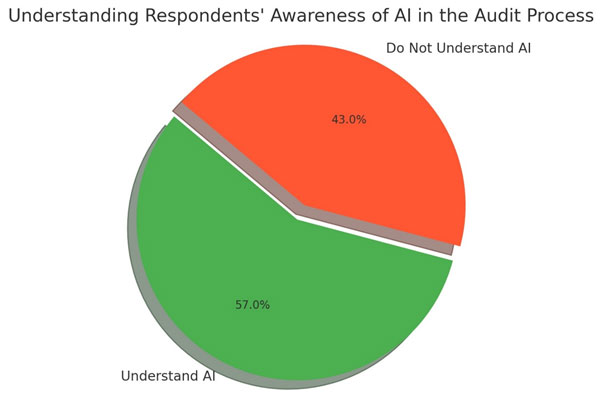

The survey results reveal that 57% of respondents have a clear understanding of the role and utility of Artificial Intelligence (AI) in the audit process, while 43% remain unaware of its application. This division in awareness highlights a notable disparity in knowledge regarding AI technology among the auditors and staff at BPK RI. The majority of those familiar with AI are likely to be more experienced auditors or individuals who have had direct exposure to advanced audit tools. In contrast, the remaining respondents, who are less informed, may consist of newer employees or those whose roles have not yet required interaction with AI-driven systems.

This gap in knowledge underscores the critical need for comprehensive training programs and targeted communication to ensure that all personnel are equipped to leverage AI technologies in their auditing roles. As the adoption of AI continues to accelerate globally, ensuring that all auditors, regardless of their tenure or position, have access to relevant information and skills will be vital for enhancing audit quality, efficiency, and effectiveness. In turn, this would support BPK RI's broader strategic goals and further align the institution with global best practices in auditing. Closing this awareness gap will not only foster a more cohesive approach to AI integration but also drive long-term innovation and performance improvements across the organisation.

Understanding Respondents' Awareness of AI in the Audit Process

Respondents' Experience in Using AI During the Audit Process

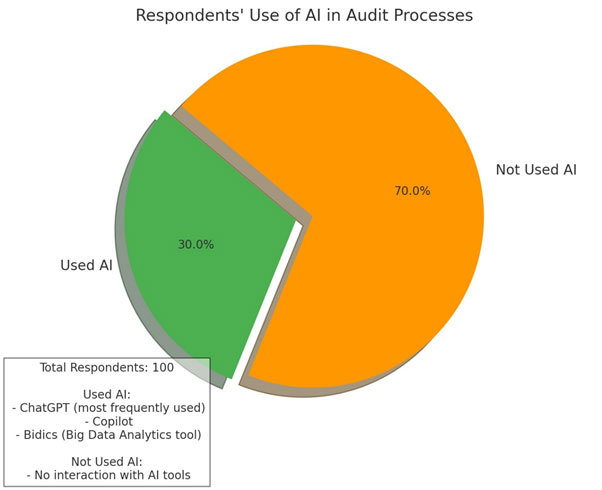

Out of 100 respondents, 30% reported having used Artificial Intelligence (AI) in their audit processes, while the remaining 70% indicated they had not yet incorporated AI into their audit work. Among the 30% of respondents who had used AI, the most frequently utilised tool was ChatGPT, underscoring the growing relevance of natural language processing tools in auditing. In addition to ChatGPT, respondents also reported using other AI applications such as Copilot and Bidics, a Big Data Analytics tool developed internally by BPK RI.

Respondents' Experience in Using AI During the Audit Process

The data highlights a trend where self-learning plays a significant role in the adoption of AI in auditing. Of the respondents who have used AI, a notable 77% learned to incorporate AI into their work through self-study, showcasing the auditors' initiative to adapt to new technologies independently. Meanwhile, 12% gained their knowledge through knowledge-sharing forums organised by BPK RI, and 10% learned from similar forums held by external entities. A small portion (1%) indicated they acquired AI knowledge through other media or platforms.

These findings illustrate that while a significant portion of auditors are yet to integrate AI into their processes, those who have are primarily self-taught or have taken advantage of learning opportunities provided by BPK RI or external sources. This highlights the importance of fostering structured learning opportunities and resources to ensure a more widespread and consistent adoption of AI technologies within BPK RI. By broadening access to formal training and knowledge-sharing platforms, BPK RI could accelerate the adoption of AI, potentially improving audit efficiency and accuracy across the organisation.

Challenges in implementing AI in audit process

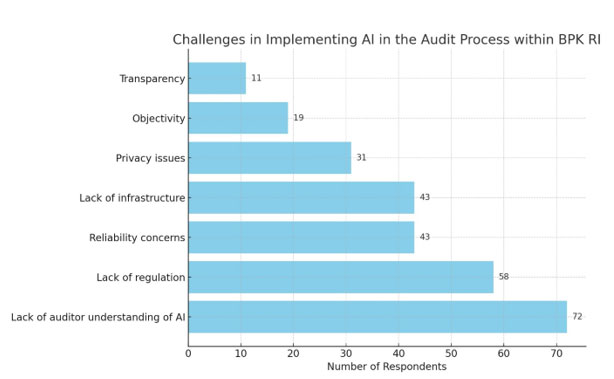

The challenges in implementing Artificial Intelligence (AI) in the audit process within BPK RI are clearly illustrated in the survey results. The data indicates that 72 of the respondents identified the lack of auditor understanding of AI as the most significant barrier. This points to a knowledge gap that could hinder the effective use of AI tools in audit practices. Alongside this, 58 of the respondents cited the lack of regulation as another major obstacle. The absence of clear guidelines or regulations may be contributing to uncertainty in how AI should be applied in auditing tasks, slowing its adoption.

In addition to these dominant challenges, 43 of the respondents highlighted reliability concerns regarding AI systems, emphasising the need for trustworthy AI tools that auditors can rely on. 43 of the respondents also raised issues around the lack of infrastructure, indicating that even if AI tools are available, the technological infrastructure within BPK RI may not be fully equipped to support their effective deployment.

Other concerns, though less frequent, include privacy issues (31 of respondents), objectivity (19 of respondents), and transparency (11 of respondents), reflecting broader worries about the ethical and operational impacts of AI in auditing. While these are not the most pressing issues according to the data, they still suggest that AI integration must be approached with caution, ensuring that technological advancements align with fundamental auditing principles.

These findings underscore the need for comprehensive training, robust infrastructure development, and clear regulatory frameworks to successfully implement AI in auditing. Without addressing these key challenges, the full potential of AI to enhance audit efficiency and accuracy will remain unrealised.

Challenges for implementing AI in audit process

Potential Benefits of Implementing AI on Audit Process

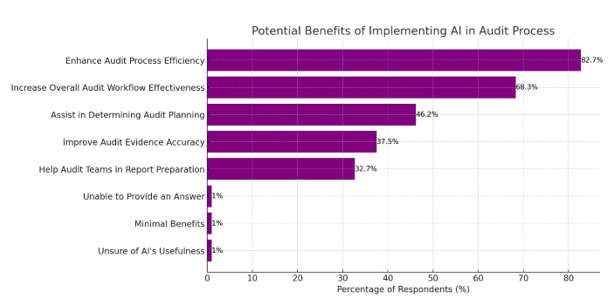

The survey results provide a comprehensive overview of the potential benefits associated with the implementation of Artificial Intelligence (AI) in the auditing process, as perceived by the respondents.

The potential benefits of implementing Artificial Intelligence (AI) in the audit process are strongly highlighted in the survey responses. A significant portion of respondents—82.7%, or 86 individuals—stated that AI could substantially enhance the efficiency of audit processes, marking it as the most prominent advantage of AI adoption in this context. This overwhelming consensus underscores the belief that AI has the capacity to streamline audit workflows, reduce time-consuming manual tasks, and accelerate the completion of audit procedures.

Closely following this, 68.3% of respondents (71 individuals) believed that AI could greatly improve the overall effectiveness of audit operations. This suggests that beyond improving efficiency, AI tools are perceived as having a transformative impact on how audits are conducted, potentially leading to more thorough and insightful audits. The ability of AI to manage complex datasets and provide deeper analysis might explain why such a large percentage view it as a game-changer in audit practices.

In addition, 46.2% of respondents (48 individuals) mentioned that AI could play a vital role in determining audit planning. The integration of Artificial Intelligence (AI) into auditing is anticipated to have strategic value in enhancing decision-making processes. AI is expected to assist auditors in selecting areas of focus, assessing risks, and prioritis ing audit tasks. By adopting a data-driven approach facilitated by AI, audit teams could potentially improve the planning phase, leading to more precise and efficient audits.

Moreover, 37.5% of respondents (39 individuals) recognised AI's ability to improve the accuracy of audit evidence. A potential benefit of implementing AI in auditing lies in its ability to ensure audits are grounded in reliable and accurate data. AI-driven tools for data validation, anomaly detection, and error identification are predicted to contribute to a more accurate representation of financial information, thereby reducing the likelihood of oversight or human error.

Additionally, 32.7% of respondents (34 individuals) believed that AI could assist audit teams in preparing reports. AI is projected to enhance the reporting phase by automating tasks such as drafting, data analysis, and insight generation. This capability is expected to allow auditors to dedicate more time to strategic responsibilities, ensuring that reports could potentially be more accurate and delivered within the required timelines.

However, despite the overall optimism, a small minority of respondents (1%) expressed uncertainty regarding AI's potential benefits. One respondent was unable to provide an answer, another viewed the advantages as nearly nonexistent, while a third remained sceptical of AI's usefulness in auditing. This hesitation could be due to a lack of familiarity with AI technologies or concerns about their reliability and effectiveness in practice. These concerns highlight the need for further education, hands-on training, and demonstration of AI's capabilities in real-world auditing scenarios.

In conclusion, while the majority of respondents recognised AI's potential to revolutionise the audit process, there remains a degree of scepticism among a small group. Addressing these doubts through clearer regulatory frameworks, improved infrastructure, and comprehensive training programs will be essential to fully realise the benefits of AI in auditing. The findings from the survey reveal that AI offers promising opportunities for increased efficiency, accuracy, and strategic decision-making in audits, but overcoming the existing barriers will be key to unlocking its full potential.

Conclusion

According to the results of the survey conducted on auditors at BPK RI to find out their perspectives on the use of AI in the audit process, it is known that out of 100 respondents who gave answers, 57% of respondents have a clear understanding of the role and utility of Artificial Intelligence (AI) in the audit process. These results are a positive thing as a foundation for BPK RI to implement AI in the audit process in the future. However, this understanding is not directly proportional to the level of use of AI in the audit process, because it turns out that only 30% of the total respondents have used AI in their audit process.

The lack of use of AI in the audit process at BPK RI is influenced by several things that are seen as challenges by auditors to implement AI in the audit process, including lack of auditor understanding, the lack of regulation, reliability concerns, lack of infrastructure, privacy issues, objectivity, and transparency.

Therefore, it is important for BPK RI to immediately take strategic steps to enhance the use of AI in the audit process. This is considering that according to the perspectives of auditors, the use of AI in the audit process has potential benefits in the future, including: enhancing audit process efficiency, increasing overall audit workflow effectiveness, assisting in determining audit planning, improving audit evidence accuracy, and helping audit teams in report preparation.

In addition to addressing the challenges in adopting AI, BPK RI's active participation in the field of auditing on a global scale is also noteworthy. As a member of INTOSAI (International Organization of Supreme Audit Institutions), BPK is committed to continuously improving its audit practices in line with international standards. INTOSAI plays a key role in supporting Sustainable Development Goals (SDGs), particularly through its Working Group on the Impact of Science and Technology on Auditing (WGISTA), where BPK also participates. This working group is focused on exploring the potential of innovative technologies, including AI, to enhance the efficiency and quality of audits.

The use of AI aligns with BPK's vision to contribute significantly to the achievement of the SDGs by 2030, particularly in strengthening public institutions, ensuring accountability, and promoting transparency. By incorporating AI into its audit processes, BPK can play a more proactive role in monitoring the progress of SDG-related programs, ensuring that public funds are used effectively and that policy goals are met in an efficient manner.

Recommendations

By considering the large potential benefits of the use of AI in the audit process, BPK RI needs to take actions to overcome the challenges. In this research paper, the author also collects perspectives from auditors regarding what things can be done by BPK RI to overcome the challenges to enhance the use of AI in the audit process.

A remarkable 82 of participants underscored the necessity of organising training and development programs aimed at enhancing the skill set of auditors in utilising AI technologies effectively. This significant endorsement reflects a widespread acknowledgement among auditors of the critical role that continuous education plays in adapting to technological advancements. The rapid evolution of AI tools necessitates that auditors not only become familiar with these technologies but also develop the expertise required to leverage them for more efficient and accurate audits.

In addition to training, a substantial 73 of respondents highlighted the importance of formulating clear regulations governing the use of AI in auditing practices. The establishment of such regulations is crucial for addressing potential ethical dilemmas, ensuring data privacy, and maintaining accountability in AI-driven processes. Clear guidelines can help auditors navigate the complexities associated with AI implementation, thus fostering a culture of compliance and ethical conduct in audit operations.

Moreover, 71 of the respondents pointed out the necessity of providing adequate infrastructure to support the effective integration of AI tools within auditing workflows. This includes the availability of advanced technological resources, robust data management systems, and secure networks that can accommodate the computational demands of AI applications. A well-developed infrastructure not only facilitates smoother operations but also instils confidence among auditors in utilizing AI as a reliable resource for data analysis and decision-making.

In terms of collaborative learning, 70 of the participants expressed their support for organizing knowledge-sharing forums. Such platforms enable auditors to exchange insights, experiences, and best practices related to AI applications, fostering a community of learning and innovation within the auditing profession. Furthermore, 61 of the respondents advocated conducting benchmarking studies to assess the effectiveness of AI in auditing, thereby facilitating a comparative analysis of AI utilisation across different organisations. This approach encourages continuous improvement and adaptation of AI technologies tailored to the unique needs and challenges of the auditing environment.

Overall, these findings emphasise the importance of a multi-faceted approach to successfully integrate AI into auditing practices. Targeted actions—such as investing in training, establishing clear regulatory frameworks, enhancing infrastructure, and promoting collaborative learning—are essential to unlock the full potential of AI in enhancing audit efficiency, accuracy, and overall effectiveness. By prioritising these areas, auditing institutions can position themselves to thrive in an increasingly data-driven and technologically advanced landscape.

References

AICI. (2024, September 24). Perkembangan AI: Inovasi Terbaru dan Ke Depan. Retrieved from Artificial Intelligence Center Indonesia: https://aici-umg.com/article/perkembangan-ai/#:~:text=Perkembangan%20AI% 3A%20Inovasi%20Terbaru%20dan%20Ke%20Depan%201,menjanjikan%20integrasi%20yang%20lebih%20dalam %20dengan%20kehidupan%20sehari-hari.

BPK RI. (2020). Strategic Plan of BPK 2020-2024. Jakarta: BPK RI.

CA ANZ. (2019). Audit and Technology. CA ANZ.

Dennis, A. (2024, February 01). What AI Can Do for Auditors. Retrieved from Journal of Accountancy: https://www.journalofaccountancy.com/issues/2024/feb/what-ai-can-do-for-auditors.html

Dotel, R. P. (2020). Artificial Intelligence: Preparing for the Future of Audit. International Journal of Government Auditing, 32-34.

Gopal, L. (2024, August 14). Artificial Intelligence in the Audit Process. Retrieved from Nanonets: https://nanonets.com/blog/using-artificial-intelligence-in-audits/

KPMG. (2024, May 20). How AI is transforming auditing and financial reporting. Retrieved from KPMG: https://kpmg.com/au/en/home/insights/2024/05/ai-transforming-auditing-and-financial-reporting.html

Lehner, O. M., Ittonen, K., Silvola, H., & Strom, E. (2022). Artificial intelligence based decision-making in accounting and auditing: ethical challenges and normative thinking. Accounting, Auditing & Accountability Journal Vol. 35 No. 9, 109-135 DOI 10.1108/AAAJ-09-2020-4934.

Menon, S. (2021, June 30). How Can AI Drive Audits? Retrieved from ISACA: https://www.isaca.org/resources/isaca-journal/issues/2021/volume-4/how-can-ai-drive-audits

Otia, J. E., & Bracci, E. (2022). Digital transformation and the public sector auditing: The SAI’s perspective. Financial Accountability & Management 2022;38., 252–280 DOI: 10.1111/faam.12317.

Panaji. (2023, June 14). The Hindu Business Line. Retrieved from SAI20 Summit Communique . Integrate AI in audit processes and tasks, SAI20 tells Supreme Audit Institutions: https://www.thehindubusinessline.com/economy/integrate-ai-in-audit-processes-and-tasks-sai20-tells- supreme-audit-institutions/article66968804.ece

Sekaran, U., & Bougie, R. (2010). Research Methods for Business : A Skill Building Approach, Fifth Edition. West Sussex: john Wiley & Sons Ltd.

Silaen, R. P., & Dewayanto, T. (2024). Penggunaan Berbagai Artificial Intelligence pada Proses Audit - A Systematic Literature Review. DIPONEGORO JOURNAL OF ACCOUNTING Volume 13, Nomor 2, Tahun 2024, 1-15.

WGISTA. (2020). Welcome to WGISTA Website. Retrieved from WGISTA: https://wgista.uaeaa.gov.ae/en/ Pages/default.aspx