Dr. Hendra Susanto, ST, M.Eng, MH, CFrA, CSFA

Board Member I

The Audit Board of the Republic of Indonesia

Dr. Susanto graduated from Sriwijaya University in 1997 with a bachelor's degree in Civil Engineering and completed a master’s degree in International Institute of Infrastructure, Hydraulic, and Environmental Engineering, Delft, the Netherlands in 2004. Then, he accomplished a Master of Business Law degree at Gadjah Mada University in 2016. Later, he completed Doctoral Degree in Accounting from the Economics and Business Program, Padjadjaran University in 2019, with the research subject on Digital Forensic Study.

He also holds a Certified Fraud Auditor and a Certified State Finance Auditor. His specialization is investigative and forensic audits. The author was mostly engaged in performing public works and infrastructure audits. In addition, he was an expert witness in numerous cases in Court.

Abstract

Infrastructure provision is an important goal in SDG's goal. Also, infrastructure development is a priority agenda in the 2020-2024 Medium Term Development Plan (RPJMN) of the Republic of Indonesia. The 2016-2020 Audit Board of the Republic of Indonesia (Badan Pemeriksa Keuangan, BPK) Strategic Plan seeks to make the RPJMN the reference and direction of the audit policy, including audit on infrastructure. To meet these needs, BPK needs to prepare the professional competence of auditors according to the regulations in the State Financial Audit Standards (SPKN). To obtain quality infrastructure audit results, BPK needs to prepare adequate human resources for auditors through education, training, and certification. BPK may also hire experts from outside BPK. Besides, the implementation of the talent pool can also contribute to fulfilling the need for qualified auditors.

A. Introduction

Infrastructure is crucial for development. It provides the services that enable society to function and economies to thrive from transport systems to power-generation facilities and water and sanitation networks. The importance of infrastructure puts infrastructure at the very heart of efforts to meet the Sustainable Development Goals (SDGs) (The Economist Intelligence Unit, 2019). Infrastructure improvement is a priority of development agendas in The Medium-Term Development Plan (RPJMN) IV for 2020-2024 of the Republic of Indonesia. The Indonesian government allocates Rp415 trillion for infrastructure spending in the 2019 government budget (16,9% of total state expenditure).

However, Indonesia is still facing significant challenges in providing quality infrastructure. The existing procurement ecosystem and institution hinder the provision of quality infrastructure compared to developed countries. The Audit Board of the Republic of Indonesia (BPK), as the state auditor, has a role in improving state financial governance and further contributing to the achievement of the national development agenda. Therefore, the BPK also anticipates what the government will do by making the RPJMN one of the references (which also coherent with SDG's goal) and the direction of the audit policy.

In the 2016-2020 BPK Strategic Plan, BPK also focuses on infrastructure themes, including examining maritime and marine themes and strengthening national connectivity through land, air, and rail transportation. Later, the BPK's 2020-2024 Technocratic Plan refers to one of the development agendas, namely strengthening infrastructure aimed at supporting economic activity and encouraging equitable national development, with the following objectives: (a) increasing national connectivity; (b) increasing the Information and Communication Technology (ICT) development index; (c) improved governance and utilization of water resources; (d) the fulfillment of decent, safe and affordable housing and settlements for households; and (e) the fulfillment of national energy needs (Badan Pemeriksa Keuangan, 2019b).

- Thematic. BPK will align the theme of the audits to be carried out with the development agenda so that the results of the BPK audit will be more actual and more optimal in guarding the government's strategic programs.

- Holistic. BPK audits will be carried out comprehensively, starting from the planning stage to monitoring and evaluation, by seeking to see the implementation of all development priorities to make it easier for BPK to identify root causes and provide more comprehensive recommendations.

- Integrative. The BPK audit assesses and evaluates Government policies in an integrated manner across all ministries/agencies across sectors. Thus, it is necessary to have a synergy of all the resources owned by the BPK following their respective portfolios so that the audit conclusions and recommendation can cover all ministries/agencies that involved in the policies/programs;

- Spatial. The BPK audit will pay attention to the spatial or spatial layout in which the policy/program is implemented to ensure the success of the policy/program in each region.

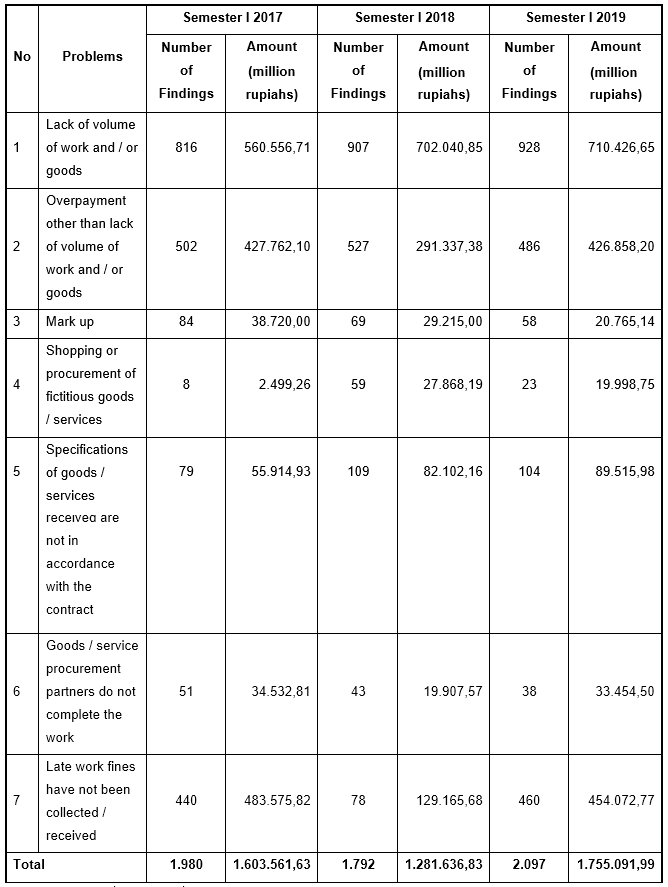

Construction activities such as road construction, buildings, ports, and airports are the main object of BPK's infrastructure audit. The audit result reveals findings such as 1) shortage of work volume, 2) overpayment, 3) late work fines, and 4) specifications of goods/services that do not comply with the contract often occur and are of material value. These audit findings show that the internal control system weakness in construction activities. On the other hand, lawsuits against the results of BPK's audits have started to emerge in the last few years. In 2016, for example, the Jambi City Asphalt Mixed Processing Unit sued the Jambi BPK Representative regarding the BPK Audit Report, which found a state financial loss of IDR 5.1 billion. The Jambi City Asphalt Mixed Processing Unit claimed that BPK had conducted errors regarding the audit mechanism. Another example, in 2014, the Sukoharjo Regency Government project partner PT. Ampuh Sejahtera sued the BPK Representative of Central Java regarding the audit results of the market construction. They also claimed that there had been procedural and calculation errors during the audit process.

The two examples above show that BPK is at risk of being sued related to the results of the audit that has been published. Therefore, BPK needs to improve the infrastructure audit strategy, especially in the construction sector. In addition to the macro audit strategy included in the BPK Strategic Plan, it is also necessary to formulate a micro audit strategy that emphasizes improving the competence of auditors and audit procedures.

As a response to such a risk, this paper aims to discuss issues and ideas concerning how to reduce such a risk by improving the audit strategies on infrastructure audit, especially that related to the construction sector. The discussion will be framed by answering the following questions:

As a response to such a risk, this paper aims to discuss issues and ideas concerning how to reduce such a risk by improving the audit strategies on infrastructure audit, especially that related to the construction sector. The discussion will be framed by answering the following questions:

- How can the audit team collectively meet the professional competence related to infrastructure inspection, especially in the construction sector?

- How to improve the BPK audit approach in the construction sector?

B. The Importance of Infrastructure Audit

The Indonesian government gives high priority to infrastructure development. The government has spent capital expenditures amounting to Rp 1, 887.7 trillion from 2014 - 2019. In 2019 alone, the allocation of the infrastructure expenditure budget was 16.9% of state expenditure or Rp415 trillion. This number has increased by 264% compared to the 2014 budget (Directorate General of Budget, 2019). Meanwhile, the regional expenditure budget also shows a similar priority agenda. The portion of capital expenditure in the 2018 APBD was relatively high, amounting to Rp223.6 trillion or 19.4% of the total regional expenditure of Rp1, 153.9 trillion.

The Ministry of Transportation carries out significant central government infrastructure development programs. From 2014-2019, The Ministry of Transportation built 15 new airports, developed 100 existing airports, the addition of 3,258 km of railway lines, developed 100 seaports, the construction of Mass Rapid Transit (MRT), Light Rail Transit (LRT), High-Speed Train (HST). ) as well as 199 terminals and ferry piers.

If one looks at the realization of the government's capital expenditure in the 2016-2018 period compared to the total expenditure, it shows that the percentage of realization exceeds 12%, and specifically, the Ministry of Transportation, the percentage of realized capital expenditure exceeds 57%. Table 1 shows the number and percentage of capital expenditure realization of the central government's total expenditure and Ministry of Transportation.

Table 1. Comparison of Realized Capital Expenditure and Total Expenditure

Realization of the Central Government and the Ministry of Transportation

| Last | Handle | ||||||

|---|---|---|---|---|---|---|---|

| Year | Realized Capital Expenditure (Rp) | Total Expenditure Realization of the Central Government (Rp) | % | Realized Capital Expenditure (Rp) | Total Expenditure Realization of the Ministry of Transportation (Rp) | % | |

| 2016 | 169.474.230.324.273 | 1.154.018.222.035.100 | 14,69 | 18.249.612.993.171 | 31.773.338.071.233 | 57,44 | |

| 2017 | 208.656.670.235.846 | 1.265.359.428.745.510 | 16,49 | 27.351.001.026.526 | 41.405.517.365.629 | 66,06 | |

| 2018 | 184.127.627.500.274 | 1.455.324.879.227.610 | 12,65 | 27.082.448.210.488 | 45.075.741.354.758 | 60,08 | |

The increase in the capital expenditure account follows the increase of total both central government and local government expenditure, which became the object of BPK's Audit, namely through Financial Statements audit and Examinations with Specific Purposes audit. One of the capital expenditures is construction and infrastructure activities through the procurement of government goods and services. Based on the Summary of Semester Inspection Results (IHPS) I 2017 - IHPS I 2019, it is known that construction findings such as shortage of work volume, overpayment, late work fines, and specifications of goods/services not following the contract are findings that often occur and are of great value. Table 2 shows the details of the examination findings.

Apart from the ability of the BPK auditor to carry out infrastructure audits, as previously explained, the BPK audit results also face several risks, namely the risk of BPK's audit results and recommendations for infrastructure audits being sued in court and cannot be followed up.

C. Auditor Competence in the Infrastructure Audit Assignment

BPK Regulation No. 1 of 2017 concerning State Financial Audit Standards (SPKN) in the Conceptual Framework paragraph 50 states that the BPK ensures that the auditor has the necessary expertise. The audit Team must collectively have the knowledge, experience, and competence required for the audit. This knowledge and practical experience of the audit project include understanding standards and statutory provisions, understanding the entity's operations, and the ability and experience to exercise professional judgment. A specialist expert may assist the auditor in carrying out their duties m based on need analysis for audit, assurance of competence and independence, and quality of work results as described in paragraph 52.

Paragraph 13 of General Standard states that the auditor collectively must have sufficient professional competence to carry out the audit task. Then paragraph 14 explains that the BPK must determine the competencies needed to ensure auditors have the appropriate skills to carry out audit assignments. BPK may use experts or auditors outside the BPK according to the competencies required in the audit as stipulated in paragraphs 16, 17, and 18.

The statement in the SPKN is critical, especially in the practice of field inspections. If BPK's auditor fails to meet the audit standard (SPKN) while conducting the audit procedures, BPK is prone the face lawsuit regarding the audit findings/results. What has been done by BPK so far to meet the demands of the SPKN in terms of the competence of the inspection team and is a good practice are: 1) recruiting auditors with a bachelor's degree in engineering, especially in construction; 2) provide training in construction inspection; 3) include auditors with a background in construction in the inspection team; 4) using construction experts from universities; 5) use a laboratory to test the results of field checks.

However, this is still not sufficiently proven by the existence of lawsuits that question the audit approach by the BPK. Besides, the existing practices show that the BPK has not paid enough attention to the fulfillment of the SPKN through carrying out good audit practices.

Therefore, the BPK needs to fulfill the SPKN in the construction field inspection by doing the following actions:

- Establishing adequate guidelines (operational guidelines/technical guidelines) regarding the inspection in the construction sector. Currently, the Research & Development Directorate of BPK is preparing one of the technical guidelines for the construction sector;

- Ensuring the audit team has an auditor with expertise in the construction field when the audit team need for the object of inspection related to the construction sector;

- Ensuring the availability of experts, if needed, in order to support the BPK audit.

D. Infrastructure Audit Approach

The audit approach or the inspection procedure in the construction sector carried out by BPK is to compare the existing contracts and the realization or facts in the field. This approach emphasizes the presence aspect of construction work. Every auditor can implement this procedure because of its simplicity; therefore, it does not require an auditor with a construction background. However, the weakness of this approach is that it will not fully disclose the violations that have occurred.

For this reason, BPK needs to design a more comprehensive audit approach and procedure in the audit technical guidelines. The BPK audit will later be directed systematically to test the existence and to assess the price, quality, quantity, and delivery of construction development. BPK audits must also pay attention to all stages in construction work, starting from the planning, procurement, and implementation stages of work.

In the planning stage, the auditor must review and understand planning documents such as the Detailed Engineering Design (DED), Engineer's Estimate (EE), and Own Estimated Price (HPS). The law violation and cheating have usually been committed at this stage. However, the problem is that it is not easy for an auditor who does not have a background in construction to analyze these documents. An expert or experienced auditor is required to perform this analysis.

In the procurement stage, the auditor will review documents such as tender documents and direct appointment documents. The auditor must ascertain whether the procurement process has been carried out according to the provisions and identify possible fraud. Apart from using the Presidential Decree on the Procurement of Goods and Services, the auditor must also pay attention to the Civil Code regarding the legal terms of the contract. Fraud in the procurement process is a violation of the legal conditions of the contract, namely lawful causes. Article 1320 of the Civil Code states that in order for a valid agreement to take place, four conditions need to be fulfilled: (1) their agreement which binds itself; (2) the ability to make an engagement; (3) a specific subject; (4) a cause that is not forbidden.

In the work implementation stage, the auditor will review the contract documents and work, including sub-contract documents, to ensure that the work is carried out following existing contracts and regulations. Auditors also test contract compliance with existing regulations. The auditor also examines the payment documents to ensure that payment for the work is following the provisions and job performance. The results of the BPK examination also showed a high risk of violating regulations and unfair prices when using subcontractors. There is also the risk that job pay is not compatible with job performance.

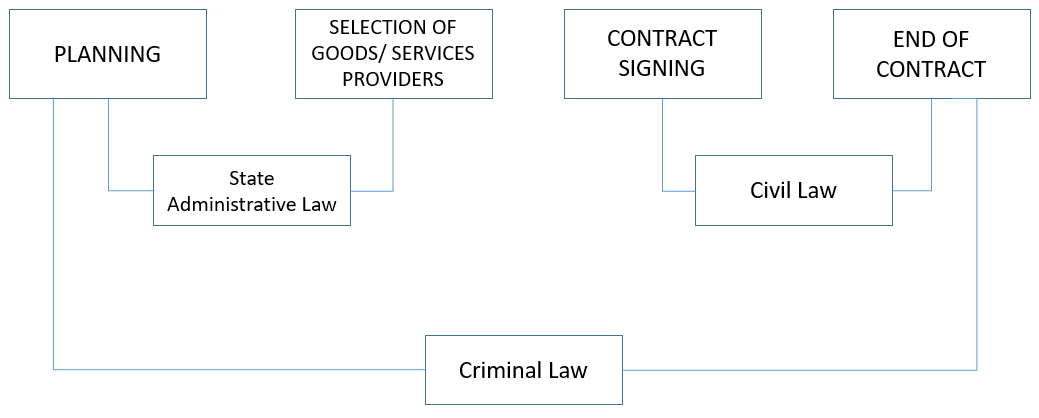

The auditor must also accompany the integrated audit approach above that the audit in the construction sector should be directed to the existence of work and the execution of work that is right on price, good quality, correct quantity, and timely. The diagram below can assist the auditor in inspecting the construction sector:

Figure 1. Law Application in Government Procurement

In general, construction problems include infrastructure development between agencies that have not been integrated. There is work overlap and inefficiency, inadequate work planning, outrageous price (markup), pro forma auction, quality of work not up to standard, work tardiness, and not yet subject to fines.

E. Use of Experts

The above analysis shows the importance of increasing the auditor's competence improvement and experts in auditing the construction sector by the BPK.

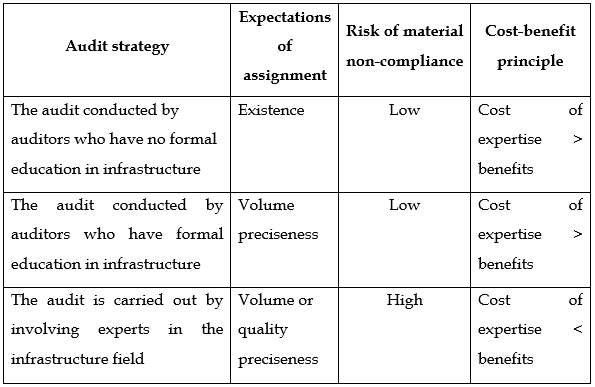

There are two options that BPK can take in carrying out infrastructure inspections, namely increasing audit competence through education, training, and certification, as well as the use of experts as stipulated in the SPKN. Based on the concept of the Study on the Use of Experts in Examination of construction activities, it is known that the use of experts is influenced by the inspection strategy, assignment expectations, risk of non-compliance, and the principle of cost-benefit as described in the following table.

Table 3. Parameters for the Use of Experts in Infrastructure Inspection

BPK auditors can perform infrastructure inspections to test the presence and accuracy of volumes with low non-compliance risk identification results. However, if the assignment expects to test the volume accuracy or quality assessment with a high risk of non-compliance, BPK needs to use experts according to the required field competence.

The next option is to increase auditors' capacity to carry out volume accuracy testing and be encouraged to have certification according to expert standards. This option can encourage BPK to carry out comprehensive infrastructure checks starting from the planning, implementation, and evaluation stages according to BPK's strategic policies. Besides, there is an urgency for implementing Strategic Initiatives for the formation of a Talent Pool. The talent pool can suffice the collective capability in a special infrastructure audit team according to the needs and expectations of the assignment. Following the Technocratic Design of the 2020-2024 Strategic Plan, the scope of the pool of talents has been identified, and software consisting of Talent Management Guidelines, Talent Management POS in Auditor Functional Positions, and Talent Management POS in Managerial Positions during the 2016-2019 period.

Conclusion

Below are the conclusions based on the description and discussion above:

1. The infrastructure development agenda in the RPJMN IV for 2020-2024 places a reasonably high portion, and the BPK Strategic Plan also emphasizes the focus of infrastructure inspection considering the importance of this, which is also shown by the large infrastructure sector budget in 2019 amounting to 16.9% of State expenditure or Rp415 trillion. Meanwhile, the infrastructure sector budget in the 2018 APBD is 19.4% of the total regional expenditure of Rp1.153,9 trillion.

2. The BPK also prepares policy directions and strategies to be able to carry out comprehensive and integrated inspections in the construction sector starting from the planning, procurement, and implementation stages of work that leads to the existence of work and implementation of work that is right on price, good quality, correct quantity, and on time.

3. BPK auditors are encouraged to have the capacity in infrastructure audits through education, training, and certification. BPK may use external experts if the audit expectation is higher as regulated in the SPKN. Also, the implementation of the talent pool is urgently needed to meet the needs of auditors in conducting infrastructure inspections.