About the Author

Mr. Vugar Ibrahimov is the Head of Staff of the Chamber of Accounts of the Republic of Azerbaijan

In modern times, all countries of the world, regardless of the level of development, have public debt at one level or another. The maintenance of macroeconomic balance in connection with the processes taking place in the global financial and economic system has led to a corresponding increase in borrowing. This has resulted in a significant increase in demand for debt capital compared to previous years. Research on public borrowing remains relevant. In many economic literatures, debt, especially public debt, is characterized as a serious economic and social problem. In fact, reality and truth, along with these ideas, include other areas of economic development. From this point of view, public debt is an integral part of economic policy, including fiscal policy. It is true that in all cases, when we say debt, as well as public debt, the obligation is understood. However, the fact that any entity, including the state, carries obligations for a certain period of time does not yet indicate that there is a problem. These liabilities become serious problems when they are not fulfilled in a timely manner (existing debts are replaced by new debts (more difficult conditions), the term- period is not chosen correctly) and the debt is directed only to current consumption expenditures.

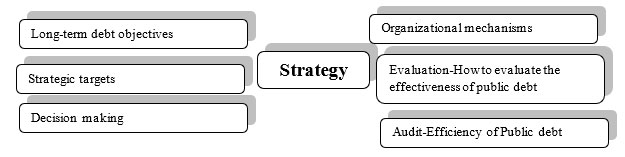

2. The approach of International Financial Institutions to borrowing and its management in the global world - Public Debt Management Strategy.

In the modern world, public debt plays an important role in the financial policy of any country. Thus, on the one hand, there are close relations with developing countries with international financial institutions, on the other hand, there is a constant market for government securities in these countries. Thus, all this expands the scope of public debt relations and significantly increases its role in the financial system of the state.

International financial institutions act as the main lending entities in foreign debt relations. Thus, the share of these institutions in the external debt of the world is very large. Foreign debt and foreign aid agencies have been set up to finance developing countries. At present, there are financial and credit institutions operating both internationally and regionally. According to international practice, the first step in public debt management is to create and manage a debt strategy that constantly monitors public debt and considers it necessary to ensure its sustainability, which in turn leads to long-term borrowing (IMF). The establishment of a public debt management strategy can be seen as a necessity for other purposes, such as the development and improvement of the public securities market or a reduction in the ratio of public debt to GDP.

The importance of the following indicators of the public debt management strategy during the audit of public debt management has been demonstrated in international practice;

2.1 Importance of debt strategy;

- The strategy identifies methods for public debt management purposes,

- Determines the characteristics, composition and mandate of debt management of the desired portfolio,

- Reflects key elements of transparency and accountability,

- Supports the sustainability and discipline of debt management,

- Includes efficiency indicators for debt management.

One of the main goals of the public debt management strategy is to more transparently examine and assess the risks that may arise in the organization of public debt, as well as to reduce the risks to an appropriate level. In making important borrowing decisions and reducing these public risks, the government should monitor financial and other public risks at all times and assess their resilience. To do this, it must first manage and assess the risks associated with foreign currency, short-term and variable interest rate debt.

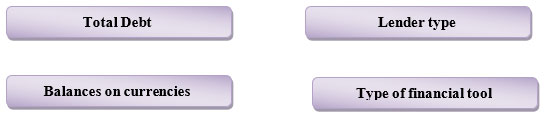

When developing a public debt management strategy, in international practice, debt managers (debt management agencies or councils) are faced with the following options (financial characteristics of debt):

- - Debt portfolio denominated in local and foreign currencies.

- - Organizational structure and liquidity of debt by maturity.

- - Debt interest rate or term-period sensitivity.

Public debt management strategy is a plan to implement debt management goals. Thus, one of the main goals of the strategy is to bring the complex debt structure to the desired state of the state. The debt management strategy should focus on managing the risks to which factors in the portfolio are exposed, in particular the potential fluctuations in the cost of debt service and its impact on the budget and debt levels. The implementation of the strategy also requires new borrowing issues and liability management operations.

In the public debt management strategy, the country must set long-term strategic goals. As a result, the debt management strategy should include certain activities to achieve these goals. According to international practice, the main purpose of debt management is to extend the required amount of financing from the medium to long term at the lowest possible cost, as well as to reduce the existing risk to a stable risk level and achieve concessions on timely repayment of liabilities.

In addition, improving the local credit market is also one of the main goals of the debt management strategy.

In general, in addition to the implementation of low-cost financing, which is the main goal of the debt management strategy, the main priority should be to formulate the debt burden portfolio to reduce the impact of external macroeconomic shocks on the budget and future long-term expenditures. The financing strategy should draw up a plan to raise the required funds in the coming years, and the goals of the strategy should coincide with the goals of the country's main medium-term and long-term debt management strategy. Any arrangement of debt instruments in the portfolio should be reflected in the debt management strategy documents. Because, as shown in this international practice, a comparative assessment of the organizational structure of the portfolio, pre-compiled on debt management documents, is carried out with debt management activities.

The importance of a debt management strategy is that the lack of this strategy could lead to further problems in the country's external borrowing capacity.

It is clear from experience that during the compilation of the debt burden profile, it was necessary to pay attention to the specific weight of variable interest rates in the portfolio and keep it at a nominal level in subsequent strategic planning. Under the above circumstances, the government should thoroughly analyze and formulate a debt management strategy, financing strategy and cost and risk reduction.

Two main borrowing strategies are developed in the development of the Public Debt Management Strategy; Domestic and External Debt Strategy.

Internal Debt Strategy;

Key Objectives for Domestic Debt Management;

- - Extension of the domestic debt portfolio to change the risk of re-borrowing and the current situation. - Proper timing profile.

- - Improving the functions of primary and secondary markets for the purchase and sale of government securities. (Initially, the reorganization of the broker and dealer system)

- - Announcing pre-issue programs to investors and financial institutions for the next financial year.

External Debt Strategy;

Key Objectives for External Debt Management;

- - Extending the medium term to reduce the risk of refinancing.

- - Proper timing profile.

- - Formation of currency complexity in the external debt portfolio due to the country's foreign exchange reserves and the impact on exports.

Debt Burden Portfolio and its analysis (Risk indicators on Term, Currency, Interest and Debt Burden)

The importance of portfolio evaluation is that its design and implementation of goals is an important component of the debt management function, as it plays an important role in determining the accepted levels of risk and implementing the following decisions:

- - In making decisions on the loan portfolio in connection with various parameters such as currency, maturity, interest rate and choice of financial instruments.

- - Making adjustments by the debt portfolio manager (institution, board, etc.) in response to changes in the market, depending on the market situation.

- - In making decisions related to the use of risk management tools as financial derivatives.

- - Implementing significant controls over debt management.

- - Increasing transparency and accuracy in public debt management.

Debt portfolio, poorly organized by currency or interest rate, has historically been one of the most important factors in the spread of economic crises in many countries. Portfolio analysis of current debt and its flow or recognition is one of the most important tools in risk assessment and is generally a starting point in the development of debt strategy. This has been identified as a key factor in managing the World Bank's and the IMF's effective debt strategy.

This information must first be obtained in order to review the aggregate portfolio;

Risk management and debt burden in debt management should be analyzed. This analysis can facilitate the recognition of risk and the cost of debt (cost) in debt management. What is included in the measurement of value; Interest expense (key to budgeting), Interest / GDP or Interest / Income (covers the debt burden of the economy), the current value of debt / GDP (includes increasing the debt burden). In connection with the assessment of a variable risk factor; it is necessary to pay special attention to market risk (exposure to interest rates and exchange rates).

The most important factor in the debt management function is to determine the risk management in the debt portfolio. In an area where exchange rates and interest rates fluctuate, fluctuations in market prices cause fluctuations in debt service costs. Exchange rate fluctuations cannot be explained by a single local exchange rate fluctuating against a credit exchange rate, this fluctuation can even change in response to cross-currency movements in global markets. For example, the appreciation of the Japanese yen against the dollar may increase the dollar value of foreign debt denominated in the Japanese yen. The risk can be significant if the debt is reflected in a variable interest rate. For example, when the contract is concluded with LIBOR interest rate. For this reason, the variable interest rate debt burden in the loan portfolio should be examined and the total risks arising from the increase in interest rates should be monitored and managed.

Debt Sustainability Analysis (Borrowing Needs, Contingent Liabilities, Domestic Market Improvement Measures and Measures to be Taken in the Event of Increased Borrowing)

In order to achieve effective public debt management in accordance with the principles of the United Nations Conference on Trade and Development, the government must develop a debt management strategy and conduct a debt sustainability analysis. Debt Sustainability Analysis assesses the country's current debt level and how expected new borrowing will affect its solvency in the future.

The government can achieve debt sustainability in the absence of any exceptions to borrowing or future adjustments in the balance of income and expenses. Borrowing decisions often require a systematic assessment of the emergence of debt burden indicators under different scenarios. Thus, in order to achieve medium- and long-term debt sustainability and the state's development goals, the government must take into account the risks of the public debt portfolio, which is severely shocked by interest rate risk, currency risk, refinancing risk. This should take into account not only the current expenditures of the public debt portfolio, but also the future expenditures of the state, which will be paid to creditors in the future.

Debt sustainability analysis is also an important part of debt management. Debt sustainability analysis is the most important financial tool in identifying, preventing and resolving potential crises. Debt sustainability analysis assesses a country's current debt level and how expected new borrowing will affect its ability to service its debt in the future. It consists of three main sections;

- - Assessment of the current debt situation, its distribution over time, whether the interest rate is stable or variable.

- - Identify vulnerabilities in debt management to make policy adjustments before difficulties arise in payments.

- - Development of an alternative debt stabilization policy in case of debt emergencies.

Debt sustainability primarily affects a country's solvency, liquidity, and regulation (future-oriented changes);

- - A country becomes solvent only if the present value of its future income flows is at least equal to the present value of its future expenditures.

- - A country is considered liquid if the country can regulate the term of its debts correctly or efficiently.

- - Fiscal policy can be effectively regulated if political and social constraints play a special role in adjusting the country's expenditures and revenues for the future.

Debt Sustainability Analysis by the International Monetary Fund (IMF), WB (World Bank), as well as ADB (Asian Development Bank) and other financial institutions, based on the identification or application of financial changes needed to maintain or reduce the debt-to-GDP ratio was adopted. The main condition for developed countries is to determine the estimated values of the debt-to-GDP ratio for the 5-year period based on the latest macroeconomic estimates and assumed fiscal policy. One of the main reasons for preparing a debt sustainability analysis is the fluctuations in debt service costs. The reasons for this fluctuation are as follows;

- - In case of non-refinancing by international organizations, states or other donors in the form of loans or grants to finance the country's budget deficit.

- - When the cost of domestic public debt service is very high.

However, in many low-income countries, external public debt is the main source of funding, while domestic public debt is considered insignificant as a source. High interest rates and short maturities of domestic debt in low-income countries expose the country to changing risks (shocks). Given the problems caused by the shocks of the macroeconomic environment, the importance of developing and implementing a Debt Sustainability Analysis has also been expressed in international practice.

Debt sustainability analysis consists of two broad parts;

- a) Preparation of Debt Sustainability Analysis.

- - Preparation of debt sustainability analysis in accordance with the recommendations and basic principles of International Financial Institutions should be in the form of an annual program for each country and agreed for medium-term or long-term development.

- b) Debt Sustainability Assessment.

- - Calculation of current and future debt burden indicators under the basic principles.

- - Development of alternative scenarios and stress tests to be included in the debt sustainability analysis and identification of country-specific factors.

- - Provide feedback on the improvement of debt burden indicators over time and the assessment of their sensitivity to shocks.

- - Comparison of external debt burden indicators with the limits of the corresponding debt burden indicators.

- - Assess the extent to which other factors, such as domestic debt or contingent liabilities, can affect a country's future debt solvency.

- - Defining a country-appropriate borrowing strategy and adequate policy.

For example, an audit of public debt efficiency was conducted in Georgia, and the audit identified a number of shortcomings:

- Georgia's reported public debt does not include the debt of state-owned enterprises that form part of its hidden contingent liabilities. Therefore, in the event of an enterprise's indebtedness / bankruptcy, there is a risk that the government's assets will decrease or its liabilities will increase. This, in turn, could have a negative impact on the country's financial situation. If contingent liabilities are not taken into account in various analyzes (for example, debt sustainability analysis), the risks and risks associated with public debt management may not be fully assessed.

- The Ministry of Finance does not have a public debt management strategy document. Based on international experience, the existence of such a document is important in ensuring medium and long-term debt sustainability. The importance of a debt management strategy is growing given the existing problems with borrowing opportunities.

- The creditor selection process is not documented and the explanatory note attached to the draft government decree does not contain information and analysis of alternative sources of funding. Therefore, the information provided in the explanatory note does not ensure the transparency of the borrowing process and does not create an informed decision-making environment.

- Risk assessment and debt sustainability analysis are not conducted on a regular basis. This, in turn, increases the risk of untimely detection and prevention of potential threats.

- Stable issues of government securities are not enough for the development of the domestic credit market. More than 90 percent of government securities were purchased by commercial banks, indicating a low level of diversification of the investor base. According to international best practices, one of the most important conditions for the development of the government's securities market is the existence of a diversified investor base.

- There is no formal rule or methodology describing the planning process to determine the General Borrowing Requirements. Within the Ministry of Finance, the process is regulated by the ministry's charter. Thus, the document does not clearly define the functions of other institutions involved in this period, except for the Department of Public Debt and External Finance. As a result, the process of determining debt needs for a planning year is not carried out in accordance with pre-defined and officially approved rules / procedures.

In connection with the above, the Georgian JSC offers the following recommendations to improve public debt management in Georgia:

- The IR must fully disclose the characteristics of the debt instrument, including holders of confidential contingent liabilities assumed by the public sector;

- When conducting macroeconomic analysis of public debt, the IR should take into account the amount of contingent liabilities and pay close attention to assessing the risks arising from them;

- Amend Georgia's Public Debt Law to bring the concept of public debt into line with international standards.

- The Ministry of Finance should develop a debt management strategy that is consistent with the entire development strategy of the country and will facilitate the achievement of the intended goals.

- A detailed comparative analysis of available funding opportunities should be prepared by the IR and attached to the draft Government Decree, along with other relevant documents.

- The Ministry of Finance of Georgia should conduct regular, at least annual, debt sustainability assessments and monitor the risks in the debt portfolio.

- The IR, in accordance with the NBG, should develop a development strategy for the local government securities market and analyze potential incentives / activities that will lead to further development of the domestic securities market.

- The MoE should apply rules / procedures to identify debt needs that will formally carry out the debt needs assessment process;

- The General Charter of the IR should be amended to define the exact roles and responsibilities of each department involved in the debt needs assessment process.

In international practice, the country's financial condition and sustainability are determined by the ratio of debt to GDP. There are many reasons to confirm the importance of this ratio. Experience shows that some countries face difficulties with low debt levels, but some countries do not experience any borrowing stress, including long-term extensions with high levels of borrowing. For example, in Argentina, the debt-to-GDP ratio was declared bankrupt at 60%, but in Japan, high debt sustainability continues, despite the fact that the highest debt is more than 200%. From this point of view, the level of debt sustainability indicates the need to define specific thresholds, taking into account the general indicators with an individual approach to each country. The maximum level of debt sustainability in a country depends on the factors specific to that country. These include: 1) The country's ability to generate surplus 2) Growth prospects 3) The cost of debt affecting the interest rate of debt and the country's market perception (ie future debt) .4) The date on which debt obligations are realized. 5) Sensitivity to shocks. 6) Investment, etc. includes.

Debt burden and liability management includes the analysis of debt sustainability, the creation of alternative scenarios and stress tests, the identification of country-specific factors (internal indicators) and the assessment of sensitivity to external shocks. coordination of term budget expenditures, further increase of efficiency in public debt management, prevention of risks in the state budget, which plays an important financial role in the country's economy, and taking preventive measures, strengthening the coordination of monetary and fiscal policy.

As a result, good public debt management combines many positive economic benefits. First, good public debt management can reduce the public debt burden in many ways. For example, a well-designed and well-implemented borrowing program can build investor confidence so that financial institutions can achieve a reduction in the difference between borrowing and borrowing rates under normal circumstances. Second, good public debt management can also help develop local financial markets. The gain of the local financial market is the acquisition and use of financial instruments that belong to the financial market, which can play a special role in investing in these instruments or in determining the prices of other financial instruments. A developed local financial market can lead to economic growth and make the economy more resilient to external shocks, such as capital outflows. Third, the practice of effective public debt management can reduce the sensitivity of the economy to financial and economic shocks.

5) Contingent Liabilities

Contingent liabilities have a significant impact on debt sustainability and fiscal resilience and should therefore be included in the debt sustainability analysis in conjunction with stress tests. Contingent liabilities are not, as is well known, liabilities, but are liabilities that arise from certain individual events that may or may not occur. These can be open or closed. Explicit contingent liabilities may be recognized as legal or contractual, and their payment may be required under the terms of the contract. Concealed contingent liabilities may be exercised not under a legal or contractual arrangement but after the conditions or events that have taken place.

What distinguishes these obligations from other obligations is that one or more conditions and events can be performed before the transfer or any transaction begins. These liabilities have become important in the analysis of public finances and the assessment of the financial condition of the government, as failure to appear when the government is in good financial condition may subsequently create the risk of financial shock or borrowing. Problems that may arise with contingent liabilities.

- - The legal status of a contingent liability in national legislation and its classification.

- - Calculation and accountability of contingent liabilities and availability of special financial resources.

- - Contingent liabilities management system as well as the existence of a strategy for contingent debt and the existence of a special agency for monitoring contingent liabilities.

- - The role of JSC in the audit of contingent liabilities.

- - Informing the public about the contingent liability and its audit results.

According to international practice, in many countries the obvious contingent liabilities are not reflected in the balance sheet. In addition, if any contingency is contemplated in the future and any rights or obligations are required, failure to specify contingent liabilities could lead to a critical financial and economic situation in the country. Contingent liabilities may increase when banks are given internal or overt guarantees, when public and private enterprises are under stress, and when the government intervenes in the financial system.

6) Risk Assessment and Debt Burden Indicators

Debt management is conditioned by risk indicators and debt burden analysis. This analysis can facilitate the recognition of risk and the cost of debt (cost) in debt management.

- - What is included in the measurement of the cost of debt (cost);

- a) Interest expense (key to budget preparation),

- b) Interest / GDP or Interest / Income (covers the debt burden of the economy),

- c) Current value of debt / GDP (includes increasing the debt burden).

- d) in connection with the assessment of a variable risk factor; it is necessary to pay special attention to market risk (exposure to interest rates and exchange rates).

- - Effective debt management risk means risk management that reflects refinancing risks and operational risks;

- Refinancing risk refers to the exposure of the debt portfolio to the risk of the refinancing debt at high interest rates: Extremely, if the risk is too high, the debt manager will not be able to change the term obligation.

- Operational risk Classification of different types of risks: Operational errors that may occur at different stages of management or registration operations: Inadequacy in the system or internal control and service: image risk: legal risk; protection risk; or natural disasters, which may affect the ability of the debt manager to obtain assets to achieve the objectives of debt management. Based on this, the debt manager had to identify the weaknesses of the existing debt. The duration of this risk depends on risk factors, such as changes in interest rates and exchange rates, exposure to risk, the share of domestic debt, the share of short-term debt, the variable rate of debt.

One of the key points in debt management is risk assessment. When assessing risks, debt burden indicators are classified under four broad headings;

- - Market risks.

- - Debt change risk.

- - Market liquidity.

- - External and financial sensitivity.

Market risks.

In general, market risks arise from the fluctuations of different types of economic variables, which depend on completely different currency and interest rates, the value or quantity of goods. For example, in many countries, limited adjustments may be made in the production of some strategic products (oil and other natural resources), which are the main source of goods or budget revenues as the main source of tax revenue. In this case, any decline in both prices and quantities of products will be reflected in the cost of debt service.

Foreign exchange fluctuations can adversely affect a debtor's solvency, e.g. As a result of the devaluation of the local currency, the debt in foreign currency will increase the cost of debt service. Also, fluctuations in the major foreign currency, which has the largest share of government external debt, can lead to fluctuations in debt service costs for debtors.

Interest rate risk arises from changes in interest rates. The mentioned changes; Income curve risk, the risk arising from refinancing for fixed interest rates, renewals for variable interest rates, and changing options in financial instruments.

a) Interest rate risk indicators.

- - “Macaulay Duration”

- The most commonly used interest rate risk indicator in public debt management is the Macaulay Term Index, the main purpose of which is related to securities. The purpose of this indicator is how long the price can be paid at the expense of income (domestic cash flow) from the security. This proved once again that long-term securities are less risky than short-term securities.

- - “Modified Duration”

- The adjusted period measures changes in the price of fixed interest rate securities in the case of different types of variable interest rates. Because changes in interest rates affect its income as well as its maturity, it measures how its price changes as a result of each interest rate change in the price of the security.

b) Exchange rate risk indicators.

One of the most commonly used indicators is the share of external debt in total debt. In developed countries, foreign currency borrowing is not recognized as a significant indicator. This is due to the fact that many developed countries, for example; France, Germany, Japan and the United States almost do not borrow in foreign currency. Experience has shown that countries borrowing in foreign currency divide their debt portfolios according to the economic situation of the country in their debt strategies in relation to foreign and local currencies. For example; Percentage of borrowing in foreign currency set in their debt strategies for selected countries.

c) Debt change risk

Debt change risk is the risk of debt refinancing. The risk of debt change arises when a country or a company re-applies for a new loan if it is unable to meet its obligations on time. If interest rates rise, then the debt will be refinanced at a higher interest rate and more interest will be paid in the future.

D) Market liquidity risk

Market liquidity risk is the ability to buy and sell government securities or stocks without any significant change in market prices.

E) External and Financial Sensitivity Risk

Information on various economic variables is required to improve debt and liquidity management policies, which are the most important element in preventing a crisis. The information that can be obtained in this area can be important in policy or management development and risk assessment.

Debt burden indicators for measuring public debt performance are grouped under three groups of indicators.

- - Indicators measuring the risks arising from the public debt created by the current economic situation.

- - Indicators measuring the risk of the government meeting contingent liabilities in unforeseen circumstances.

- - Financial indicators showing the activity of the liability market.

Each group of indicators has its own characteristics, which in turn are the main factors that distinguish them from each other. First, the sensitivity analysis requires the emergence of indicators that prevent and measure any situation that would hinder the payment of debt under current conditions. These indicators are usually static.

- - External debt service cost / export ratio - This ratio measures a country's ability to repay its external debt at the expense of income from trade in goods (foreign).

- - Public debt service cost / income ratio - This ratio mainly measures the country's solvency.

- - External debt / GDP ratio - This is a measure of the growth rate of debt by the ratio of debt to total resources. Debt growth should be lower than GDP growth.

- - Public debt / GDP ratio - This is the most commonly used indicator. According to the Maastricht agreement, EU countries consider this ratio to be acceptable at 60%. This ratio should also be considered individually according to the characteristics of each country.

- - Public Debt / Local Budget Revenues - This ratio measures a country's level of borrowing according to its ability to pay.

- - The ratio of public debt to service expenditures / local budget revenues - This ratio measures the country's ability to repay debt with local resources.

In general, macroeconomic shocks create some fiscal problems with debt in developing countries, the main reason for which is the low level of debt burden. In international practice, the proposed debt burden levels are determined on an individual basis for each country. Low or high levels of debt burden are causing many fiscal problems in countries. Although many countries have high controls, they have lower debt burden than the recommended rate. To determine this, it is necessary to assess the possible weaknesses:

On the other hand, several countries with higher debt burden than the recommended level can be classified as low control. These may be countries that have sufficient liquid assets or they have the mitigation of significant risks arising from high debt burdens.

Debt burden and debt profile risk rates.

For market economy countries, the regulation of standards on two different elements of debt sustainability analysis is used: 1) Rates for debt profile risk indicators 2) The use of debt burden rates in risk assessment.

Recognition of debt stress events For developing countries.

- 1. Bankrupt; Balances of principal and interest payable to creditors.

- 2. Restructuring; Any activity that will change the terms of a creditor or receivable agreement.

- 3. IMF financing; Liquidity issues related to public debt difficulties.

For developed countries

- 1. Bankrupt; Non-current government debt obligations. (S&P recognition)

- 2. Restructuring; Any activity that will change the terms of a creditor or receivable agreement.

- 3. IMF financing; Exceeding 100% of the price.

- 4. Inflation; if it is more than 35% per annum.

Debt burden and debt profile risk indicators.

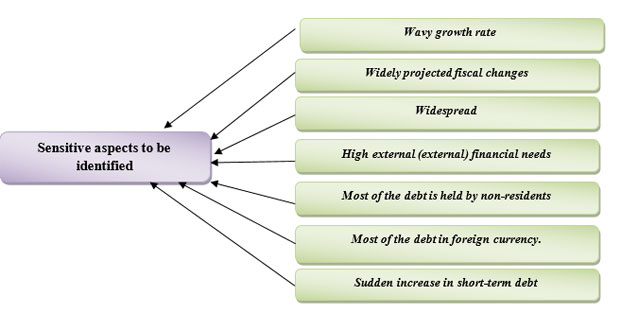

Debt profile risk indicators for developing countries.

- 1. The ratio of external financial demand (Gross) to GDP as a percentage.

- 2. Part of public debt in foreign currency in total public debt.

- 3. Change in short-term public debt in total public debt.

- 4. Share of non-residents in total public debt.

- 5. Term distribution of bonds in the emerging securities market.

Debt profile risk indicators for developed countries.

- 6. The ratio of external financial demand (Gross) to GDP as a percentage.

- 7. Change in total public debt short-term public debt.

- 8. Share of non-residents in total public debt.

- 9. Distribution of bond yields over time.

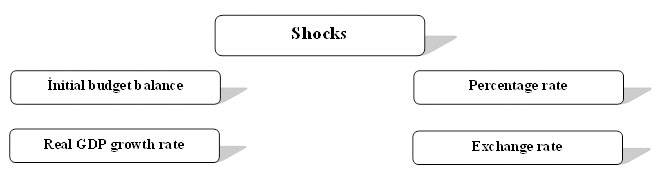

7) Shocks and Stress tests

The impact of shocks on macro-fiscal variables may result in a deterioration in debt dynamics. This is important because the module complements the basic sustainability assessment with an assessment that combines macro fiscal risks. In particular, this module assesses the importance of the initial (budget) balance, GDP growth, interest rates and exchange rates for debt sustainability affected by shocks. Lists the shocks in the example applied to the four variables shown in the following example;

- Stress tests are designed to standardize and establish balance according to country-specific circumstances. For example, the use of country-specific estimates of income and expenditure elasticity is encouraged when this is possible, and especially when the country applies fiscal rules. Estimates of the relationship between the initial budget balance and the production deficit can also be used. If inflation is sensitive or particularly volatile to the production deficit, then a larger decline in inflation should be considered. The magnitude of interest rate and exchange rate shocks can be adjusted in cases where most of the historical chronology is not convincing, as they reflect significant difficult periods that are unlikely to be repeated. Amendments should be presented and explained in a transparent manner when reviewed and recorded in the staff report.

- Also, a shock scenario is created automatically. In the sum of individual shocks, it should be taken into account that the impact of individual shocks affecting many variables is not doubled. For example, a country may be sensitive to increasing shocks and initial balance shocks. As a result, the combined shock includes the effects of all individual shocks on all relevant variables (real GDP growth, inflation, initial budget balance, exchange rate and interest rate).

- If the proposed stress tests do not adequately cover country-specific risks, or if the macroeconomic framework includes an alternative scenario, then private alternative public debt sustainability analysis scenarios should be developed. The analysis of alternative scenarios is more effective in the new example, which allows flexibility in creating scenarios for the following variables: real GDP growth, Inflation, the ratio of income to GDP, the ratio of non-interest government expenditures to GDP, Interest rate, and Exchange rate. For example, alternative scenarios could be implemented taking into account the impact of external shocks (macro and / or financial) related to the crisis in another country on the country's debt sustainability, or demonstrate a policy change scenario. In addition, the established alternative scenario can be expressed as collateral, for example, an assessment of the scope of adverse effects between the public and financial sectors or the impact of a sudden cessation of capital inflows. For major commodity producers, the impact of shocks and commodity prices on key public debtors must be taken into account in the first instance, and a specific scenario must be written to measure that associated risk.

8) Borrowing Need

It is very important to correctly determine the need for borrowing in accordance with the financial situation of the country. Determining the need for public borrowing in subsequent years is not only a complex activity, but also requires information on the level of importance and coordination between government agencies involved in various activities. A transparent estimate of the need for borrowing will save the country from excessive borrowing, otherwise it could worsen the country's financial situation. Low borrowing needs can also lead to a liquidity crisis in a country; Borrowing Need = Amount of principal debt + Budget deficit + Initial cost of financial asset + Contingent liability

- In general, a transparent estimate of borrowing needs should include the following financial components: Debt to be incurred during the year + Estimated budget deficit + Initial cost of the estimated financial asset + Estimated contingent liabilities. Many countries use different types of models to model the need for borrowing for years to come. For example; The Organization for Economic Co-operation and Development (OECD) countries use only the budget deficit (required amount) and the debt to be received during the year (debt to be covered) in the formulation of the need for borrowing.

- According to international practice, the Ministries of Finance of the countries are responsible for the preparation of the annual borrowing plan and its inclusion in the draft annual budget. The budget deficit is agreed with the next year based on the borrowing needs drawn up on the basis of the draft budget.

- We would like to emphasize that the body that oversees the implementation of investment projects is responsible for determining the amount of investment debt. Also, the Public Debt and the relevant agency are responsible for determining the amount of debt directed to the budget deficit. v In international practice, countries have their own guidelines for determining the need for borrowing, and these guidelines have been formally developed and approved in the course of the document. As a result, it is recommended that the Ministry of Finance develop guidelines and guidelines for the transparency of the borrowing process that include the stages of formal borrowing procedures.

Results and Suggestions

1. Development of a new debt strategy that constantly monitors public debt and deems it necessary to ensure its sustainability.

According to international experience, public debt management is primarily the creation and management of a debt strategy that constantly monitors public debt and considers it necessary to ensure its sustainability, the lack of which may lead to further problems in the country's external borrowing opportunities. Experience has shown that a debt management strategy is a key condition for effective debt management.

We consider it expedient to develop and create a methodology from the legal point of view and to carry out the following procedures.

- - More transparent inspection and assessment of risks that may arise in the organization of debt.

- - Bringing the debt portfolio to the desired state.

- - Assess the potential fluctuations in debt service costs and their impact on the budget and its level of debt. - Extending the required amount of funding from the medium to long term at the lowest possible cost, as well as reducing the existing risk level to the reserve risk level and achieving concessions in the timely payment of liabilities.

- - Improving the local credit base.

- - Reducing the impact of external macroeconomic shocks on the budget and future long-term expenditures of the debt burden portfolio.

- - Development of a plan to attract the required funds and its coordination with the country's medium and long-term development prospects.

- - Any arrangement and arrangement of debt instruments in the portfolio should be reflected in the strategy documents.

- - Comparative assessment of the organizational structure of debt.

Objectives of the internal debt strategy.

- - Extension of the domestic debt portfolio to change the risk of re-borrowing and the current situation.

- - Improving the functions of primary and secondary markets for the purchase and sale of government securities.

- - Stabilization of the financial sphere of the state and adaptation of money supply to the current economic situation, development in a strategic direction as a single mechanism, in conjunction with monetary and fiscal policy.

- - Formulation of expenditures on the basis of targeted programs based on the end result and formation of the optimal ratio in the structure of state budget expenditures on the basis of efficiency.

- - Expansion of the investor network, formation of a competitive environment and regulation of interest rates in order to attract more money.

- - Announcing pre-issue programs to investors and financial institutions for the next financial year.

2. Objectives of the External Debt Strategy.

- - Proper timing profile.

- - Formation of currency complexity in the debt portfolio due to the country's foreign exchange reserves and the impact on exports.

- - Prolongation of the medium term to reduce the risk of borrowing.

- - Adjustments in the loan portfolio to respond quickly to changes in market conditions (currency, maturity, interest rates, selection of financial instruments, etc.)

- - Periodic analysis of the debt burden in accordance with the risk indicators.

- - Periodic monitoring of variable interest debt burden on the loan portfolio.

3. Debt Sustainability Analysis.

As a result, good public debt management combines many positive economic benefits. First, good public debt management in many ways reduces the public debt burden and increases debt sustainability. For example, a well-designed and well-implemented borrowing program can build investor confidence so that financial institutions can achieve a reduction in the difference between borrowing and borrowing rates under normal circumstances. Second, good public debt management can also help develop local financial markets. The gain of the local financial market is the acquisition and use of financial instruments that belong to the financial market, which can play a special role in investing in these instruments or in determining the prices of other financial instruments. A developed local financial market can lead to economic growth and make the economy more resilient to external shocks, such as capital outflows. Third, the practice of effective public debt management can reduce the sensitivity of the economy to financial and economic shocks.

- - Assess the current level of the country's debt and how the expected new borrowing will affect its solvency in the future.

- - Assessment of the current debt situation, its distribution over time, whether the interest rate is stable or variable.

- - Identify vulnerabilities in debt management to make adjustments in management before difficulties arise in payments.

- - Development of an alternative debt stabilization policy in case of debt emergencies.

- - Assessing the impact of debt sustainability primarily on the country's solvency, liquidity and regulation (future-oriented changes).

- - Investigation of the causes of fluctuations in the cost of debt service and its regulation.

- - Calculation of current and future debt burden.

- - Development of alternative scenarios and stress tests to be included in the debt sustainability analysis and identification of country-specific factors.

- - Improving debt burden indicators over time and assessing their sensitivity to shocks.

- - Assess the ability of other factors, such as domestic debt or contingent liabilities, to affect a country's future debt solvency.

- - Defining a country-appropriate borrowing strategy and an adequate policy.

3. Risk indicators in debt management.

- - Risk indicators facilitate the analysis of the debt burden, as well as facilitate the recognition of the value of the debt.

- - Classification of debt burden indicators (market risks, debt change risk, market liquidity, external and financial sensitivity) during risk assessment.

- - Carrying out a classification to measure public debt performance, including measuring the risks posed by public debt created by the current economic situation, measuring the risks of contingent liabilities by the government in the event of unforeseen circumstances, and financial performance of the liability market.

3. Determining a transparent estimate of borrowing needs in accordance with the country's financial situation.

In international practice, countries have their own guidelines for determining the need for borrowing, and these guidelines have been formally developed and approved in the course of the document.

As a result, it is recommended that the Ministry of Finance develop guidelines and guidelines for the transparency of the borrowing process that include the stages of formal borrowing procedures and include the annual debt, estimated budget deficit, estimated cost of the asset and contingent liabilities. development of regulations governing the need for unifying Borrowing.

3. Prospects for effective operation of the state debt policy

The optimal threshold in the field of public debt should be limited to borrowing directly directed to the production sectors and public capital investments in the social sphere. We consider it expedient to pay special attention to the following issues in the field of forecasting and management of public debt;

- The flexibility of public debt plans must be ensured.

- Public debt plans should be both mandatory and guiding.

- By forecasting inflation and other macroeconomic imbalances in the country, they must control the negative effects they can have on public debt management.

- The process of collecting financial information should be fully ensured in order to improve public debt planning.

The experience of developed countries is of great importance for the establishment of public debt relations. Thus, the experience of these countries in the field of public debt must be studied in depth and must be used in the development and implementation of economic reform programs. Along with all this, the peculiarities of the national economy must be taken into account. Because in international practice, any reform that has yielded positive economic results can lose its effect under the influence of demographic, national, psychological factors within the national economy. It is considered expedient to have the following main directions of the state debt policy;

Foreign loans attracted as public debt should be directed mainly to real production and services, which are more important in terms of economic development. This is mainly important in terms of public debt management in line with the requirements of the current situation.

a. The predominance of domestic public debt is also favorable due to a number of other features. As it is known, the state, as a borrower, pays for its loans. The payment of these funds to domestic entities creates conditions for them not to leave the country, and this aspect is beneficial for economic growth.

b. The country's economic needs for credit should be met not through government loans, but through banks and other credit institutions. This is due to another form of economic policy of the state - credit policy. Commercial banks and non-bank credit institutions must meet a large part of the country's credit needs. In addition, specialized banks should be established in the country, which should offer cheap and soft loans in accordance with the requirements of each sector. Although this policy is not directly related to public debt, it also reduces public debt by reducing the amount of public credit directed to the economy.

C. It is necessary to increase confidence in government securities by paying off debts on government securities in a timely and full manner, to issue securities in accordance with the current economic situation, thus ensuring the development of the government securities market.

In modern conditions, in most developing countries, public debt is repaid through public borrowing. This means replacing one problem with another, even if it prolongs the term of the obligation in terms of public debt. Thus, loans to production and services should be repaid at the expense of the profits of these sectors, so as not to become a heavy burden for the state. Based on the experience of developed countries, the role of financial regulators, especially taxes, in public debt policy is not insignificant. This is especially true for loans in a number of areas, as well as state-guaranteed loans. Thus, the state, in addition to controlling the activities of these enterprises in connection with borrowed funds, will improve their financial situation by easing the tax burden, and ultimately ensure the full repayment of loans. As a result, it is expedient to define specific methods and techniques of organizing public debt relations through the development of a strong package of laws in the country, and at the same time to include in this task the methods of organizing the work of the Ministry of Finance.

4. Contingent Liabilities

According to international practice, in many countries the obvious contingent liabilities are not reflected in the balance sheet. In addition, if any contingency is contemplated in the future and any rights or obligations are required, failure to specify contingent liabilities could lead to a critical financial and economic situation in the country. Contingent liabilities may also increase when banks provide internal or overt guarantees, when public and private enterprises are under stress, and when the government intervenes in the financial system.

Taking all this into account, based on international experience, we consider it expedient to apply the following procedures.

- - Given the significant impact of contingent liabilities on debt sustainability and fiscal resilience, it should be included in the debt sustainability analysis in conjunction with stress tests;

- - Development of regulatory rules for the purpose of constant control and effective management of contingent liabilities,

- - Management of debt burden and liabilities, including debt sustainability analysis, creation of alternative scenarios and stress tests, identification of country-specific factors (internal indicators).

- - According to international practice, in many countries, the lack of information on the measurement of contingent liabilities, terminology and their classification, as well as the non-disclosure of information about them in the financial statements violates the principle of transparency in the balance of public debt and incorrect classification of contingent liabilities.

Lack of information on contingent liabilities and their classification in terms of legal status can lead to serious problems in their management, monitoring and accountability. For the qualitative audit of public debt and contingent liabilities, first of all, the JCA requires the development of appropriate legislation and guidelines for the correct classification of contingent liabilities, and we would also like to note that it is advisable to take into account the country's goals and international experience.

- - Financial crises not only paralyze the economies of many different countries over time, but also turn them into direct debts in contingent debt. In this regard, a crisis protection system should be established;

First - the identification of potential risks

Second - effective monitoring.

Third - the detection and elimination of risky processes in debt management.

One way to effectively control the level of contingent liabilities (to determine the amount of contingent liabilities, to establish monitoring and evaluation guidelines) is to centralize all information related to contingent liabilities in a centralized manner by one financial institution.

5. Improving Public Debt Management.

One of the main sources of public debt management is to ensure control over the use of state-guaranteed loans. As it is known, while the users of these loans are various independent economic entities, the state is the entity responsible to foreign creditors for the return of these funds. Therefore, it is recommended that the relevant government agencies exercise strict control over the efficient use of borrowed funds to ensure their timely repayment and develop a new action plan to implement the above-mentioned issues of the public debt mechanism and implement it taking into account the existing economic conditions.