Mr. Ahmad Adib Susilo,

Senior Advisor in Environmental and Sustainable Development.

Mr. Muhammad Rafi Bakri,

Data and Finance Analyst at the Secretariat of the Senior Advisor for Environment and Sustainable Development

Ms. Ratna Wulandari,

Audit Board of Indonesia

Introduction

The development of Artificial Intelligence (AI) and Machine Learning (ML) has penetrated various sectors, including the public sector. The efficiency and accuracy offered by AI and ML encourage more governments and public institutions to adopt them.

AI and ML not only enhance operational performance but also improve public services. They expedite administrative processes and increase transparency and accountability. Additionally, the use of AI and ML enables predictive analysis that helps governments plan more effective programs and policies. Compared to other Information and Communication Technologies (ICT), AI and ML are believed to have a greater impact on citizens due to their application in the core functions of government organisations and their learning nature, which can enhance public sector performance over time and influence decision-making (Ho et al., 2020; Veale & Brass, 2019)

In the realm of auditing, the ability of AI and ML to analyse large data sets, identify patterns, and flag anomalies makes these technologies particularly suitable for audit purposes. Their suitability for auditing extends beyond improving accuracy and efficiency in financial reporting; it is also relevant in the context of sustainability audits. These technologies can help identify environmental practices and evaluate the social impact of an entity's operations.

AI and ML can analyse data from various sources, such as environmental sensors, company reports, and public data. Their ability to identify patterns in data helps uncover sustainability-related risks, such as potential violations of environmental regulations. These technologies also enable continuous monitoring of sustainability indicators, such as carbon emissions or energy usage. With real-time monitoring, auditors can detect issues earlier and provide timely recommendations.

This situation makes AI and ML highly reliable for auditing Sustainable Development Goals (SDGs) by the Supreme Audit Institution (SAI) of Indonesia or Badan Pemeriksa Keuangan (BPK). Sustainability issues are not only fundamental but also incredibly complex to audit. To ensure that sustainability audits yield impactful results for achieving the SDGs in Indonesia, we need assistance beyond human capabilities.

Basic of AI and ML

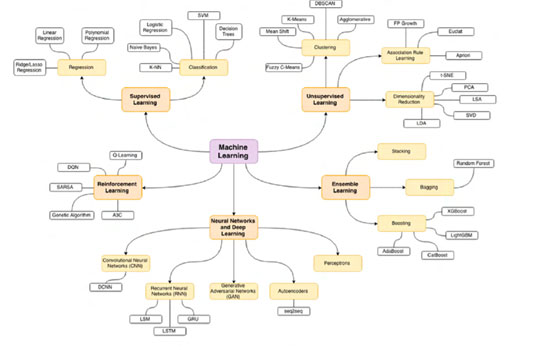

Figure 1 provides a structured overview of Machine Learning (ML), categorising key methodologies into distinct types. At the core, it divides ML into Supervised Learning, Unsupervised Learning, Reinforcement Learning, Ensemble Learning, and Neural Networks and Deep Learning. Supervised Learning is further classified into Regression and Classification techniques, with examples like Linear Regression, Logistic Regression, Decision Trees, and Naive Bayes.

Figure 1. Machine Learning Structure

Source: INTOSAI Journal (2023)

Unsupervised Learning is segmented into Clustering, Association Rule Learning, and Dimensionality Reduction methods. Clustering includes techniques such as K-Means and DBSCAN, while Dimensionality Reduction highlights methods like PCA and t-SNE. Reinforcement Learning lists techniques including Q-Learning, DQN, and SARSA, focusing on learning strategies through reward-based decision-making processes.

The figure also details Ensemble Learning, dividing it into Stacking, Bagging, and Boosting methods, with examples like Random Forest and XGBoost, emphasising model combination for improved accuracy. Additionally, Neural Networks and Deep Learning are represented with subtypes like Convolutional Neural Networks (CNN), Recurrent Neural Networks (RNN), Generative Adversarial Networks (GAN), and Autoencoders, illustrating the layered architecture and specialised applications of neural networks.

Machine Learning (ML) is a critical component of Artificial Intelligence (AI), forming a core part of how AI systems evolve and adapt. ML includes various techniques—such as supervised, unsupervised, and reinforcement learning—that enable AI systems to refine their performance continuously by incorporating new data. Each technique brings unique strengths, from identifying hidden patterns to optimising decision-making based on feedback, which greatly enhances AI's accuracy and relevance in complex, dynamic environments.

In essence, ML not only supports AI but serves as its dynamic backbone, empowering intelligent applications that can adapt and respond to new situations. From voice recognition systems to recommendation engines, ML fuels AI's capabilities, expanding what AI can accomplish. As a result, ML is not only a part of AI but is fundamental to achieving the adaptive and intelligent behaviours that define modern AI technologies.

The Establishment of Sustainability Audit

With the increasing demand for the commitment to and support for Net Zero Emissions (NZE) and the Sustainable Development Goals (SDGs), sustainability audit has become imperative to provide progress report on the organizational compliance with the SDG and NZE targets. In Indonesia, sustainability reporting has been mandatory for financial institutions and publicly traded companies since 2019, with State-Owned Enterprises (SOEs) and listed companies brought into compliance in 2020 under Financial Services Authority Regulation No. 51/POJK.03/2017 and Ministerial Regulation No. PER-02/MBU/7/2017. Notably, the Audit Board of Indonesia (BPK RI) has set a precedent as the first and only government institution to voluntarily produce a sustainability report, hinting at the potential for other government bodies to adopt similar reporting practices to enhance transparency on organisational sustainability performance.

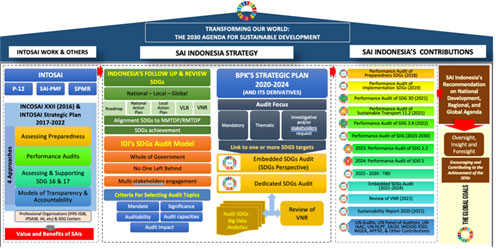

BPK addressed contemporary advancements by executing a performance audit of the government's sustainability initiatives. Figure 2 demonstrates that BPK has incorporated the sustainability audit plan into its strategy plan for 2020-2024. The BPK aims to persist in doing performance audits on sustainability initiatives until 2030.

Figure 2. BPK Framework in Auditing Sustainability

The BPK aims to persist in doing performance audits on sustainability initiatives until 2030 in accordance with globally recognized standards and principles, ensuring that the information disclosed is reliable, relevant, and transparent.

The Global Reporting Initiative (GRI) Standard is widely adopted, encompassing key economic, social, and environmental aspects critical to stakeholders (Bappenas, 2023). Additionally, the Sustainability Accounting Standards Board (SASB) provides sector-specific guidelines, enabling companies to disclose information most pertinent to investor interests. Other frameworks, such as the Task Force on Climate-related Financial Disclosures (TCFD) and ISO 26000, support organisations in recognising and communicating their sustainability impacts.

The recent introduction of sustainability reporting standards by the International Financial Reporting Standards (IFRS) Foundation, specifically IFRS S1 and S2, offers companies a cohesive framework for reporting on sustainability-related matters. By adhering to these standards, companies can present a more holistic account of their sustainability efforts and social responsibilities, resonating with a growing public expectation for corporate accountability.

As these standards gain traction, the likelihood of their application in the public sector increases. Should this shift occur, the BPK will expand its audit scope on sustainability, moving beyond performance audits to encompass financial audits. This transition will require public institutions to disclose sustainability-related issues in the notes of their financial statements, which BPK will then evaluate for accuracy and compliance with applicable standards and legislation. This integrated approach reflects a growing commitment to embedding sustainability in all facets of organisational accountability and governance.

The Needs of AI and ML-Powered Audit

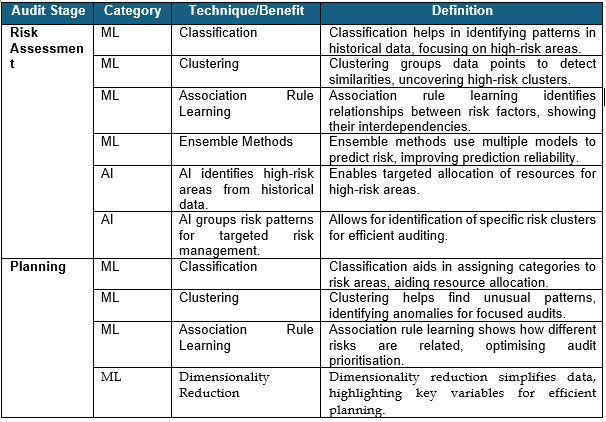

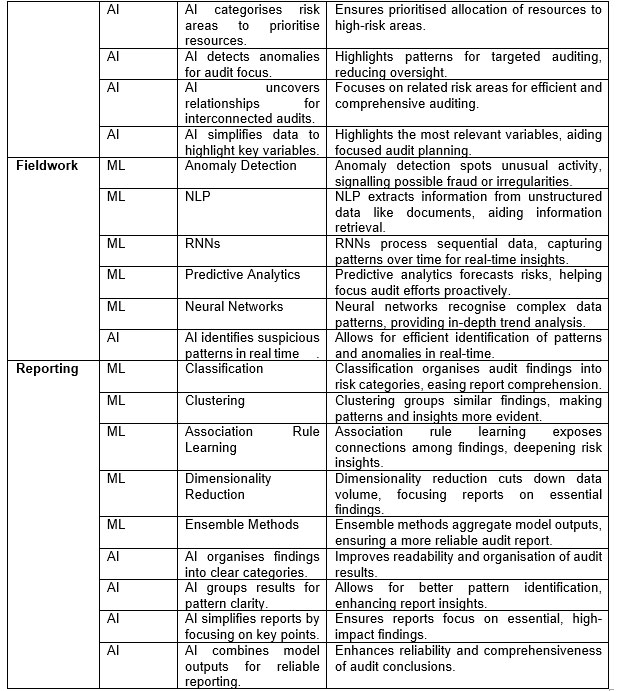

Integrating AI and ML into auditing sustainability initiatives brings new potential for enhancing accuracy, transparency, and the overall effectiveness of audits focused on environmental, social, and governance (Shivram, 2024). As companies face increasing expectations from stakeholders to report on their sustainability performance, AI-driven tools can help auditors validate sustainability metrics, detect anomalies, and ensure compliance with evolving sustainability requirements throughout the audit lifecycle—from risk assessment to reporting. Details of the use of AI and ML in sustainability audits can be seen in Table 1.

Table 1. Sustainability Audit Lifecycle with AI and ML

In the risk assessment phase, ML techniques provide robust capabilities. Classification algorithms, such as Decision Trees and Logistic Regression, facilitate the identification of high-risk areas by categorising data based on historical patterns. Clustering methods, like K-Means, enable the detection of similar risk patterns, improving targeted risk assessments. Association Rule Learning, such as the Apriori algorithm, reveals relationships between risk factors, offering insights into interdependencies. Ensemble techniques, including Random Forest and XGBoost, combine multiple models to increase predictive accuracy, while Recurrent Neural Networks (RNNs) process sequential data to forecast risk trends over time. Additionally, reinforcement learning, exemplified by Q-Learning, supports adaptive risk management by optimising decisions based on past outcomes. Collectively, these machine learning approaches enable BPK to conduct a proactive and data-driven assessment of potential risks, thereby strengthening the effectiveness and precision of the audit process.

During the audit planning phase, Generative AI and Large Language Models (LLMs) can help streamline the process of defining the scope and objectives for sustainability audits. Sustainability audits differ from traditional audits because they often involve non-standardized metrics and indicators, requiring customisation and specialised focus areas. Generative AI can assist auditors by generating initial documentation tailored to the unique aspects of sustainability audits, helping to establish a structured approach from the outset. Additionally, unsupervised ML techniques, such as clustering, are valuable for analysing sustainability-related data to identify patterns or anomalies. This can help auditors detect outliers, such as departments or facilities that significantly deviate in their sustainability metrics, warranting closer inspection. AI-based anomaly detection ensures that auditors focus on the areas with the highest potential for discrepancies, aligning their planning efforts with areas of greater risk or opportunity in sustainability.

Fieldwork is where AI and ML have a transformative impact on sustainability audits by enabling comprehensive analysis of vast and complex datasets. In sustainability auditing, data is often sourced from multiple channels, including operational data (e.g., emissions, water usage), supplier information, and third-party certifications. Traditionally, auditing a sample of this data might miss critical information, but with AI-powered full population testing, auditors can analyse every data point related to the organisation’s sustainability claims, improving the accuracy and completeness of their assessments. Descriptive analytics tools and low-code platforms make it possible for auditors to examine sustainability data without extensive technical expertise, allowing for in-depth, real-time analysis of all metrics across the organisation.

For example, ML algorithms can detect inconsistencies between an organisation’s reported emissions and its energy consumption data, highlighting discrepancies that may suggest misreporting or data inaccuracies. This level of scrutiny is essential for validating the credibility, as stakeholders increasingly demand robust, verifiable information on sustainability efforts. By using AI to support comprehensive data coverage, auditors ensure that all aspects of sustainability performance are rigorously evaluated, enhancing the reliability of the audit findings.

In the reporting phase, AI tools are invaluable for preparing sustainability audit reports that are both transparent and informative. Given the complex and diverse nature of sustainability data, summarising findings in a way that is understandable to a wide range of stakeholders is often challenging. AI-powered report generation can streamline this process by drafting initial versions of sustainability reports. This reduces the time required to prepare comprehensive reports and allows auditors to focus on refining insights and validating factual accuracy.

Additionally, AI visualisation tools can assist in presenting complex sustainability data in accessible formats, such as graphs and dashboards, to help stakeholders quickly grasp the organisation’s sustainability performance. AI can also ensure that the final report aligns with regulatory requirements and industry standards, helping organisations maintain transparency in their sustainability efforts. By automating parts of the reporting process, AI tools not only speed up delivery but also ensure consistency and clarity, allowing organisations to communicate their sustainability efforts effectively to stakeholders.

The Path to AI-Driven Audits at BPK

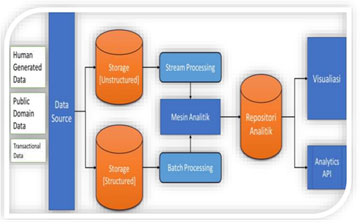

Implementing an AI-based sustainability audit is quite achievable for BPK, as it already has a Big Data Analytics platform (BIDICS) in place. Structured data, typically received by auditors, consists of clearly defined rows and columns in a table format. Unstructured data, on the other hand, lacks a clear structure and includes formats like text, images, audio, and video. Additionally, BIDICS can analyse semi-structured data, where the structure is embedded within the data itself, such as JSON, XML, or HTML files sourced from government websites or other organisations. Structured data is processed in batches, while unstructured data undergoes stream processing. The analytic engine applies statistical and mathematical algorithms to these data types, with results stored in an analytics repository and presented visually on a dashboard or accessed through APIs by applications like SiAP or office tools like Microsoft Excel.

Figure 3. Logical Architecture of BIDICS

BIDICS analyses both structured and unstructured data as seen in Figure 3.

Source: Grand Design Big Data Analytics BPK (2021)

However, challenges remain in applying AI to sustainability audits. The main challenge is the need for specialised training for auditors in understanding sustainability metrics and AI tools, as the non-financial data involved in sustainability audits can differ greatly from traditional financial data. Furthermore, sustainability data often comes from diverse sources, which may complicate data integration and increase the difficulty of applying standardised AI techniques. Ensuring transparency and explainability of AI algorithms is also crucial, as stakeholders need to trust that AI-driven conclusions are accurate and unbiased. Additionally, regulatory guidance on sustainability auditing with AI is still evolving, requiring auditors to remain adaptable and informed on best practices.

For organisations to maximise the potential of AI in sustainability auditing, they need to prioritise auditor training on sustainability metrics and AI concepts, fostering a workforce skilled in both sustainability issues and advanced data analytics. Low-code analytics platforms can support this transition by enabling auditors to apply AI in their audits without extensive technical knowledge. In time, as auditors become more proficient with these tools, they can leverage AI to deliver high-quality, objective, and impactful sustainability audits.

Conclusion

In summary, the integration of Artificial Intelligence (AI) and Machine Learning (ML) into sustainability auditing processes presents transformative potential for BPK, enhancing the integrity and credibility of sustainability reporting across diverse sectors. Embedding AI and ML at every stage of the audit lifecycle—from risk assessment and audit planning to full-population testing and reporting—enables BPK to adopt a rigorously data-driven approach. This technological advancement strengthens the precision, transparency, and efficiency of sustainability evaluations, allowing auditors to deliver robust, evidence-based insights and to hold organisations accountable with greater rigour.

As demands for verifiable sustainability efforts intensify, BPK’s adoption of AI-driven auditing not only advances accountability but also bolsters the reliability of sustainability disclosures, thus meeting the rising expectations of both national and international stakeholders. Realising these gains requires strategic investment in auditor training, data management systems, and compliance with evolving sustainability standards. By pioneering AI integration in sustainability audits, BPK can establish a national benchmark for transparency, efficiency, and integrity in sustainability reporting—reinforcing Indonesia’s commitment to sustainable development and solidifying trust among its citizens and global partners.

References

Bappenas. (2023). Laporan Pelaksanaan Pencapaian Tujuan Pembangunan Berkelanjutan 2023. Grand Design Big Data Analytics BPK, Pub. L. No. KEPUTUSAN SEKRETARIS JENDERAL BADAN PEMERIKSA KEUANGAN REPUBLIK INDONESIA NOMOR /K/X-XIII.2/8/2021 (2021).

Ho, D. E., Sharkey, C. M., & Cuéllar, M.-F. (2020). Government by Algorithm: Artificial Intelligence in Federal Administrative Agencies.

INTOSAI. (2023). Science and Technology in Audit. International Journal of Government Auditing, 50(Q2). Shivram, V. (2024). AUDITING WITH AI: A THEORETICAL FRAMEWORK FOR APPLYING MACHINE LEARNING ACROSS THE INTERNAL AUDIT LIFECYCLE. EDPACS, 69(1), 22–40. https://doi.org/10.1080/07366981.2024.2312025

Veale, M., & Brass, I. (2019). Administration by Algorithm? Public Management meets Public Sector Machine Learning. https://ssrn.com/abstract=3375391