Mokhamad Meydiansyah Ashari,

Auditor at The Audit Board of the Republic of Indonesia

Background

Climate change, largely driven by carbon emissions, has become an urgent global environmental issue. Its significant impacts, particularly in terms of global temperature rise, require immediate attention and action. One of the global initiatives to address this challenge is the Sustainable Development Goals (SDGs), an ambitious agenda encompassing 17 goals and 169 targets to be achieved by 2030, focusing not only on economic and social aspects but also on environmental concerns.

Indonesia, the world's largest archipelagic nation with over 17,000 islands, faces unique and serious challenges related to climate change. The impact of climate change in Indonesia is reflected in the trend of rising temperatures. The Indonesian Agency for Meteorology, Climatology, and Geophysics (BMKG) recorded that from 1981 to 2018, Indonesia experienced an average temperature increase of about 0.03°C per year (BMKG, 2020). While this figure may seem small, the cumulative temperature rise over several decades can have significant impacts on ecosystems and human life.

Moreover, Indonesia's geographical position makes it highly vulnerable to the impacts of climate change, particularly sea-level rise, which threatens coastal areas at a rate of 0.8-1.2 cm per year. Considering that about 65% of Indonesia's population lives in coastal areas, the impact of sea-level rise potentially poses serious consequences for a large portion of the population.

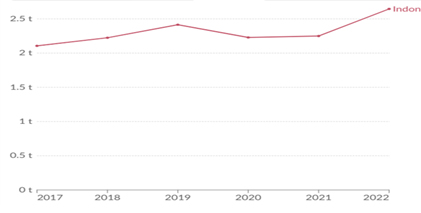

From 2010 to 2018, Indonesia's Greenhouse Gas (GHG) emissions experienced an upward trend of about 4.3% per year (KLHK, 2021). This increase aligns with the average temperature rise of 0.03°C per year recorded between 1981-2018 (BMKG, 2020). The latest data in Figure 1 shows the development of CO2 emissions per capita in Indonesia from 2017 to 2022, indicating an upward trend with an average annual growth of about 4.8%. Although there was a decrease in 2020-2021 due to the impact of the COVID-19 pandemic, a significant surge occurred in 2022, reaching 23.8% from the previous year. This pattern underscores the major challenges Indonesia faces in controlling CO2 emissions, especially as the economy recovers post-pandemic.

Figure 1: Trend of CO2 Emissions Per Capita in Indonesia

source: (ourworldindata.org, 2024)

Carbon Tax as a Climate Change Mitigation EffortFacing these challenges, Indonesia has contributed to global action by becoming a signatory to the Paris Agreement, committing to reduce greenhouse gas (GHG) emissions by 29% by 2030, or 41% with international support. This commitment was ratified through Law Number 16 of 2016. Subsequently, Indonesia developed a GHG reduction policy plan in the form of a Nationally Determined Contribution (NDC) in 2016, last updated in 2022. The 2022 NDC report states that the largest GHG contributors in Indonesia are the Forestry and Other Land Uses (FOLU) sector, followed by the energy sector (KLHK, 2022)

Various elements in Indonesia have taken proactive steps to effectively reduce GHG from these two sectors, notably by introducing a carbon tax policy. The carbon tax in Indonesia is seen as an effort to mitigate climate change while promoting sustainable economic growth. The implementation of this carbon tax is part of Indonesia's comprehensive strategy to reduce GHG emissions and adapt to the impacts of climate change, while maintaining economic growth (Pratama et al., 2022).

A carbon tax was introduced in Indonesia in 2021 through Law Number 7 of 2021 on the Harmonization of Tax Regulations. The law defines carbon tax as a tax imposed on carbon emissions that negatively impact the environment. To implement the carbon tax, two main prerequisites are required: the existence of a Carbon Tax roadmap and a Carbon Market roadmap. The Carbon Tax roadmap is a legal product between the president and the legislature that at least includes strategies for reducing carbon emissions and alignment with the development of new and renewable energy.

The law also sets a minimum rate of IDR30,000 (thirty thousand rupiah) per kilogram of carbon dioxide equivalent (CO2e). The government simultaneously issued Presidential Regulation Number 98 of 2021, which generally regulates Carbon trading in Indonesia with the following key points:

1. Carbon Trading can be conducted through domestic and/or international trade;

2. Emission Trading and GHG Emission Offset mechanisms as part of Carbon Trading; and

3. Carbon Trading can be conducted through carbon market mechanisms via Carbon Exchange and/or direct trading.

Challenges in Implementing Carbon Tax in IndonesiaDespite various advances Indonesia has made in climate change mitigation. However, there are still several areas for improvement before implementing the carbon tax. One of the main challenges is determining the right timing for this policy's implementation. Considering that Indonesia is still in the stage of economic recovery post-COVID-19 pandemic, inappropriate timing could cause significant economic distortions. Maghfirani et al. (2022) emphasise that the government needs to consider the potential impact on the prices of goods and services, as well as public consumption levels. The next challenge in implementation preparation is designing a fair mechanism that aligns with Indonesia's economic structure. This includes determining an effective tax rate and implementing an accountable Monitoring, Reporting, and Measurement (MRV) system.

Implementation preparation must also consider distributional impacts, especially on low-income households. The carbon tax policy has the potential to disproportionately burden this group of society, particularly in rural areas (Dian, 2016). Therefore, in the preparation stage, the government needs to design appropriate targeted compensation or assistance schemes. These could include income tax reductions, increased social assistance, or special incentives to encourage the use of clean energy among low-income communities (Maghfirani et al., 2022). Pratama et al., (2022) also highlight that the implementation of a carbon tax should be applied gradually and with the principle of prudence.

The Role of BPK in Preparing for Carbon Tax ImplementationDespite various advances Indonesia has made in climate change mitigation. However, there are still several areas for improvement before implementing the carbon tax. One of the main challenges is determining the right timing for this policy's implementation. Considering that Indonesia is still in the stage of economic recovery post-COVID-19 pandemic, inappropriate timing could cause significant economic distortions. Maghfirani et al. (2022) emphasise that the government needs to consider the potential impact on the prices of goods and services, as well as public consumption levels. The next challenge in implementation preparation is designing a fair mechanism that aligns with Indonesia's economic structure. This includes determining an effective tax rate and implementing an accountable Monitoring, Reporting, and Measurement (MRV) system.

Implementation preparation must also consider distributional impacts, especially on low-income households. The carbon tax policy has the potential to disproportionately burden this group of society, particularly in rural areas (Dian, 2016). Therefore, in the preparation stage, the government needs to design appropriate targeted compensation or assistance schemes. These could include income tax reductions, increased social assistance, or special incentives to encourage the use of clean energy among low-income communities (Maghfirani et al., 2022). Pratama et al., (2022) also highlight that the implementation of a carbon tax should be applied gradually and with the principle of prudence.

The Role of BPK in Preparing for Carbon Tax ImplementationUp to 2024, BPK has conducted at least two audits related to climate change: a Performance Audit on the Effectiveness of the Program to Increase the Contribution of New and Renewable Energy in the National Energy Mix in 2019 (BPK, 2020) and in 2023, a Performance Audit on Climate Change Mitigation and Adaptation Actions in the Forestry and Other Land Use Sector (BPK, 2024). Based on these two audits, several significant challenges were found regarding the readiness for carbon tax implementation:

1. The absence of established emission limits. Without a clear cap on emissions, the implementation of the carbon tax becomes problematic, and the development of a robust carbon market is hindered. This absence of emission limits creates uncertainty for businesses and makes it difficult to set appropriate tax levels that would effectively incentivise emission reductions.

2. Unclear economic projections related to carbon trading, particularly in the forestry sector. The ongoing revisions to regulations in this sector have made it difficult for the government to accurately project the economic potential of carbon trading. This uncertainty affects not only the forestry sector but also has implications for the broader implementation of the carbon tax policy.

3. Furthermore, the lack of definite and sustainable funding sources for renewable energy investment poses a significant hurdle. The transition to a low-carbon economy requires substantial investments in renewable energy infrastructure. However, without a clear and sustainable funding mechanism, this transition becomes challenging, potentially undermining the effectiveness of the carbon tax in driving long-term emission reductions.

Based on these findings, BPK then provided recommendations to the government, including the immediate setting of emission limits, acceleration of the revision process for regulations related to carbon trading in the forestry sector, and development of more concrete funding scenarios to support renewable energy development.

This proactive approach by BPK illustrates the evolving role of SAIs in climate policy implementation. By providing actionable recommendations based on comprehensive audits, SAIs like BPK are moving beyond traditional oversight roles to become key players in shaping effective climate policies. This shift in approach sets a valuable precedent for other SAIs worldwide, demonstrating how audit institutions can contribute significantly to addressing global environmental challenges.

Conclusion and Future OutlookThe implementation of the carbon tax in Indonesia is a strategic step in efforts to mitigate climate change and promote sustainable economic growth. The success of this policy greatly depends on thorough preparation and addressing the identified challenges. In this context, the role of SAIs like BPK becomes increasingly crucial and can serve as a model for other SAIs worldwide.

The Indonesian experience offers valuable insights for other SAIs within the ASOSAI community. One key lesson is the importance of capacity building within SAIs. Enhancing auditors' understanding of environmental issues and green economy concepts is crucial for conducting effective audits of climate change mitigation policies. This may involve specialised training programs, collaborations with academic institutions, or exchanges with other SAIs that have experience in this area.

Regular performance audits of carbon tax implementation and related policies are also important to assess policy effectiveness over time and provide input for necessary adjustments. SAIs in various countries can collaborate, and share knowledge & best practices in optimising audit approaches and evaluating policies related to carbon tax and climate change mitigation.

The role of SAIs in promoting transparency and accountability is also crucial. SAIs can encourage transparency in carbon emission reporting and the use of funds generated from carbon taxes, which will help increase public trust in policies and promote better compliance. Developing methodologies to evaluate the long-term impact of the carbon tax on emission reduction and sustainable economic growth can also be a focus for SAIs worldwide.

Based on audit findings, SAIs can provide valuable input in developing and refining policies related to carbon tax and climate change mitigation. The role of SAIs is not limited to oversight functions but also as strategic partners of the government in achieving sustainable development goals and carbon emission reduction. In the long term, the contribution of SAIs will be a key factor in ensuring that carbon tax policies not only achieve environmental objectives but also support a just transition towards a low-carbon economy. SAIs play a vital role in bridging environmental, economic, and social interests in climate change mitigation efforts.

The experience of BPK Indonesia in auditing carbon tax preparation and implementation serves as a valuable case study for the ASOSAI community. It highlights the importance of innovative audit methodologies, the need for capacity building within SAIs, and the strategic role that SAIs can play in addressing global environmental challenges. As countries across Asia and beyond grapple with the implementation of climate change mitigation policies, the insights and approaches developed by BPK Indonesia offer a valuable resource for the broader SAI community.

List of RegulationRepublic of Indonesia (2016). Law 16 of 2016 about Ratification of Paris Agreement To The United Nations Framework Convention On Climate Change. State of Secretary of Republic of Indonesia, Jakarta

Republic of Indonesia (2021). Law 7 of 2021 about Harmonization of Tax Regulations. State of Secretary of Republic of Indonesia, Jakarta

Republic of Indonesia (2021). Presidential Regulation 98 of 2021 about Implementation of Carbon Economic Value for Achieving Nationally Determined Contribution Targets and Control of Greenhouse Gas Emissions in National Development. State of Secretary of Republic of Indonesia, Jakarta

Reference

- BMKG. (2020). Rencana Strategis Badan Meteorologi, Klimatologi, Dan Geofisika Tahun 2020-2024. https://cdn.bmkg.go.id/Web/RENCANA-STRATEGIS-BMKG-TAHUN-2020-2024.pdf

- BPK. (2020). Laporan Hasil Pemeriksaan Kinerja atas Efektivitas Program Peningkatan Kontribusi Energi Baru Terbarukan Dalam Bauran Energi Nasional Tahun 2017 s.d. Tahun 2019.

- BPK. (2024). Laporan Hasil Pemeriksaan Kinerja Aksi Mitigasi dan Adaptasi Perubahan Iklim Sektor Kehutanan dan Penggunaan Lahan Lainnya Tahun Anggaran 2021 s.d. Semester I 2023.

- Dian, R. (2016). Indonesian Treasury Review Carbon Tax Sebagai Alternatif Kebijakan Mengatasi Eksternalitas Negatif Emisi Karbon Di Indonesia. Perbendaharaan, Keuangan Negara Dan Kebijakan Publik, 53–67.

- KLHK. (2021). INDEKS KUALITAS LINGKUNGAN HIDUP INDONESIA 2020. https://ppkl.menlhk.go.id/website/filebox/1156/230626140318IKLH 2020.pdf

- KLHK. (2022). Enhanced Nationally Determined Contribution Republic of Indonesia 2022. https://unfccc.int/sites/default/files/NDC/2022-09/23.09.2022_Enhanced NDC Indonesia.pdf

- Maghfirani, H. N., Hanum, N., & Amani, R. D. (2022). Analisis Tantangan Penerapan Pajak Karbon di Indonesia. Jurnal Riset Ekonomi, 4. https://doi.org/https://doi.org/10.53625/juremi.v1i4.746

- ourworldindata.org. (2024). Indonesia: CO2 Country Profile - Our World in Data. https://ourworldindata.org/co2/country/indonesia

- Pratama, B. A., Ramadhani, M. A., Lubis, P. M., & Firmansyah, A. (2022). Implementasi Pajak Karbon di Indonesia: Potensi Penerimaan Negara dan Penurunan Jumlah Emisi Karbon. Jurnal Pajak Indonesia, 6, 368–374.