Farizah Harman

Abstract

Public sector audits are essential to ensure the integrity and efficiency of the government. They improve financial management by identifying weak controls, reducing risks and improving budgetary oversight. Regular audits lead to better public services through the continuous improvement of government processes. AI integration increases auditing accuracy and accountability, rendering traditional methods obsolete as AI efficiently processes complex transactions. In addition, the prevalence of fraud through undetected activity is driving auditors to adopt AI to speed up audits and improve quality for stakeholders. By embracing AI in auditing, the public sector can stay ahead of the curve and avoid being left behind.

Keywords: Artificial Intelligence (AI), Public Sector Auditing, Accuracy, Accountability

Introduction

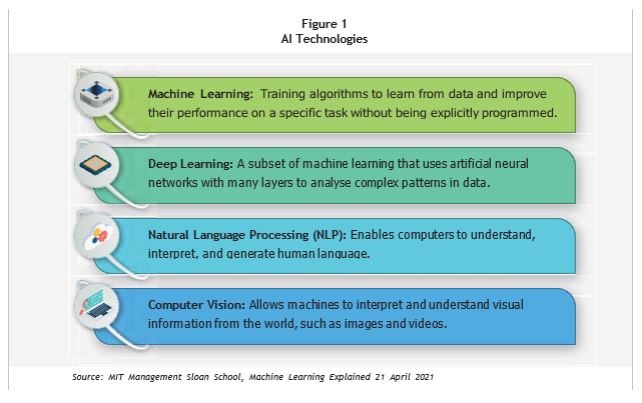

When talking about Artificial Intelligence, many people immediately think of ChatGPT or chat assistants from service providers that help with either Your Banking Application or ticketing needs as the most popular tools. However, AI can do much more, from the communication tools to the most complex business transactions. Today, AI involves with the creation of computer systems capable of performing tasks that normally require human intellect. These tasks include learning from experience, understanding natural language, recognising patterns, making decisions and solving problems. AI encompasses a wide range of technologies and approaches, as listed in Figure 1 below:

As mentioned above, AI is already being used in various applications, including:

- Virtual assistants such as Siri and Google Assistant;

- Recommendation systems on platforms like Netflix, Amazon and Capcut;

- Self-driving cars on Tesla automobile;

- Medical diagnosis and treatment;

- Fraud detection; and

- Customer service chatbots.

Overview of AI In Auditing

Artificial Intelligence (AI) is revolutionising the audit profession by improving efficiency, accuracy and the ability to quickly analyse vast amounts of data. AI tools can automate routine tasks, identify anomalies, and provide deeper insights through advanced data analysis, allowing auditors to focus on more complex and judgement-based aspects of their work. In the public sector, the importance of accuracy and accountability cannot be overstated. The assurance provided by audits means that public funds are being used appropriately and transparently, fostering trust among citizens. AI's ability to improve the accuracy and reliability of audits plays a critical role in maintaining this accountability, ensuring that government operations are conducted with integrity and in compliance with regulations.

The Role of AI in Public Sector Auditing

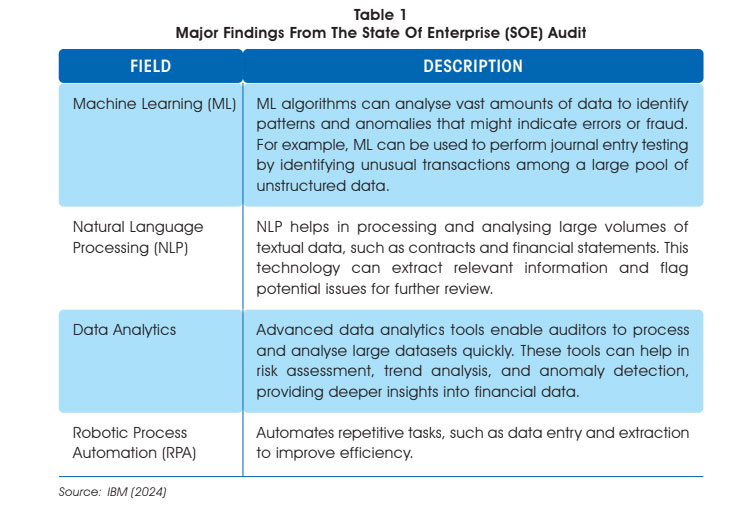

Artificial Intelligence (AI) in auditing refers to the use of advanced algorithms and machine learning techniques to improve the efficiency and effectiveness of audit processes. Some common AI technologies used in auditing as shown in Table 1 below:

Current Application of AI in Public Sector Audit

AI is increasingly being integrated into public sector audit to improve accuracy, efficiency and effectiveness, which has facilitated the overall audit work. Integrating artificial intelligence (AI) into the public sector is a transformative journey that promises to increase efficiency, improve service delivery and foster innovation. This improves the process of assessing, planning and executing audit work as follows:

i. Risk Assessment and Planning

AI can assist auditors in the planning phase by analysing historical data to identify high-risk areas that require more attention. It also improves risk assessment by providing deeper insights into data, allowing auditors to focus on relevant identification of high-risk areas. Thus, AI supports audit planning by automating risk assessments and identifying areas that require more attention.

ii. Anomaly Detection

AI algorithms can analyse entire datasets, enabling comprehensive scrutiny of all transactions. This capability enhances the detection of potential fraud and irregularities, ensuring a more thorough and accurate audit process. By leveraging AI, auditors can efficiently handle large volumes of data, uncovering patterns and anomalies that traditional methods might overlook. Previous practices often relied on sampling, which could potentially miss significant irregularities due to the limited scope of data reviewed. This approach was time-consuming and less effective in identifying subtle or infrequent anomalies compared to AI abilities.

iii. Automated Data Processing

AI can automate the processing of financial data, such as reading and reconciling bank statements and legal contracts (Anita Dennis 2024). This reduces the time and effort required for manual data entry and minimises errors. Manual processes in traditional audits are time-consuming because they require manual data collection, entry, verification and analysis, which are labour-intensive and repetitive tasks. These processes are also prone to human error, such as typing errors, misinterpretation of data and overlooked documents, all of which can lead to inaccurate audit results. The tedious nature of these tasks can lead to auditor fatigue, further increasing the likelihood of errors and oversights.

iv. Fraud Detection

By using data analytics and anomaly detection to analyse large volumes of financial data, irregularities and potential fraud can be detected more effectively than with traditional methods. With data analytics, auditors have access to 100% complete data, enabling them to make a deeper assessment of high-risk areas and examine historical trends to test against management's predictive assumptions, which are used to analyse future trends. Traditional audits typically rely on sample-based testing, which may not capture all anomalies or issues within the data. Because only a sample is tested, there's a chance that anomalies or problems in the untested data may go undetected. The sample selected may not be representative of the entire dataset, leading to inaccurate conclusions.

v. Continuous Monitoring

AI-powered continuous monitoring enables real-time analysis of financial transactions, allowing auditors to identify and address issues as they arise. This proactive approach not only improves the accuracy and reliability of financial reporting, but also significantly reduces the risk of fraud and error, ensuring a more secure and transparent financial environment. In contrast, traditional audit methods typically involve periodic reviews, often quarterly or annually, which means that any discrepancies or fraudulent activity may go undetected for months. This delay can result in significant financial loss and missed opportunities for corrective action.

Case Study and Examples of How AI is Being Used in Public Sector Organisation and Audits The National Health Service UK (NHS)

The NHS has used AI to analyse large datasets, including the National COVID-19 Chest Imaging Database, to improve healthcare outcomes and streamline review processes. By using AI, the NHS can efficiently process and interpret vast amounts of medical imaging data, leading to faster and more accurate diagnoses. For example, during the COVID-19 pandemic, AI algorithms were used to analyse chest X-rays and CT scans to identify patterns and abnormalities that could indicate COVID-19 infection. This not only accelerated the diagnosis process, but also helped to monitor the progression of the disease, enabling timely and effective treatment interventions. In addition, AI-driven analysis facilitated more efficient audits by automating the review of imaging data, ensuring consistency and reducing the workload of healthcare professionals.

Transport Canada

Transport Canada has integrated AI into its audit processes to improve efficiency, particularly when conducting risk-based reviews of air cargo records. By using AI, the department can quickly identify potential risks and anomalies in large volumes of data, allowing staff to focus on more strategic and valuable tasks. For example, AI can automatically flag shipments with unusual patterns or discrepancies, such as a cargo declared as low risk but originating from a high-risk region. This allows auditors to prioritise these flagged cases for further investigation, making a more effective and focused use of their expertise.

National Audit Office UK (NAO)

The NAO has adopted AI to improve its oversight of public spending by analysing vast amounts of data more efficiently than traditional methods. By using AI, the NAO can quickly identify patterns and anomalies within financial data, helping to identify inefficiencies, potential fraud and areas where public funds are not being used effectively. This advanced analysis enables the NAO to make more accurate and timely recommendations to improve financial management and ensure that taxpayers' money is spent wisely, ultimately contributing to better governance and accountability.

Information Commissioner’s Office UK (ICO)

The ICO conducts AI audits to ensure that organisations comply with data protection laws. These audits involve a thorough examination of how personal data is collected, processed and stored by AI systems. In this way, the ICO helps organisations identify and mitigate data protection risks and ensures that personal data is handled responsibly and ethically. This process not only helps organisations avoid legal penalties, but also builds public trust by demonstrating a commitment to protecting individuals' privacy. For example, a company developing a new AI-driven customer service chatbot could undergo an ICO audit to ensure that the chatbot's data handling practices comply with GDPR regulations, thereby protecting customer information and maintaining trust.

Royal Malaysian Police (RMP)

The RMP has integrated AI to streamline its administrative processes and improve service delivery. The Auxiliary Force, part of the RMP, has started using AI-powered body cameras equipped with facial recognition technology. These body cameras help identify suspects by comparing captured images with those in the police database. This technology not only helps with identification after an incident, but also increases transparency and accountability.

AI is used to analyse data to identify crime patterns and predict potential criminal activity. This helps the RMP to make informed decisions and deploy resources more effectively. The integration of systems such as the Police Reporting System (PRS) and the Cars Accident Reporting System (CARS) allows for the efficient handling of crime and accident reports.

Accountant General of Malaysia

The Accountant General's Department has achieved improved accuracy in automated document processing for a high volume of diverse documents using an AI document processing tool. This has led to significant improvements in operational efficiency and a reduction in processing errors, allowing for a more strategic reallocation of human resources. This process involves the management of financial data from ministries and departments, helping to produce reliable year-end financial statements and the basis for the preparation of the national budget.

National Audit Department of Malaysia (NADM)

In the case of Malaysia, one of the NADM’s initiative is the launch of a digital audit platform called the NADM’s Digital Public Infrastructure (DPI) service. The implementation of DPI prioritises the implementation of a centralised data storage solution to establish robust security protocols, improve data management practices and ensure data integrity. This project was launched in 2023 as part of the 12th Malaysian Plan development programme. The plan is in line with the MyDigital initiative launched by the Malaysian government, which focuses on a digitisation-driven programme to improve public sector auditing to make it more transparent and reliable.

To effectively integrate AI, it is critical that public sector organisations foster a cultural shift towards continuous learning and adaptability. Leaders must implement change management strategies to address resistance and promote the benefits of AI through open communication and engagement. Robust data management and governance frameworks are essential for AI integration to ensure data quality, security and privacy.

In addition, collaboration with private sector partners and other government agencies can accelerate AI integration by providing access to advanced technologies and expertise. For example, pilot projects allow AI applications to be tested on a smaller scale before full implementation, helping to refine policies and identify potential challenges. The NADM is currently making efforts to ensure the successful implementation of DPI, including the establishment of guidelines for auditing through the new digital platform and ongoing training for auditors on the specific topics to increase their capacity and competence.

Advantages of Artificial Intelligence in Public Sector Auditing

There are a few advantages that could be benefitted from the implementation of AI in the domain of auditing, such as enhancing the accuracy of the audit findings, boosting accountability towards the organisations that produce the audit reports, etc. The benefit of AI is discussed further as follows:

Enhancing Accuracy With AI

Audit findings are believed to be presented with a higher accuracy level with the emergence of AI. Several scholars in their studies proved that the process in finding audit evidence as well as undertaking necessary analysis would be much easier with the help of technologies in the process of gathering information and audit evidence. Among the benefits that could help in boosting the accuracy of audit findings via the emergence of AI could be viewed through the discussion below:

i. Data Analysis and Anomaly Detection

AI-driven data analysis and anomaly detection involves using advanced algorithms to sift through large data sets to identify patterns, trends and outliers. By automating this process, AI can quickly spot anomalies that could indicate errors, fraud, or other irregularities that could compromise the accuracy of the data. This has not only increases the reliability of the data, but also allows proactive measures to be taken to address potential issues before they escalate. Some of the notable examples of successful data anomaly use of AI as shown in Table 2 below:

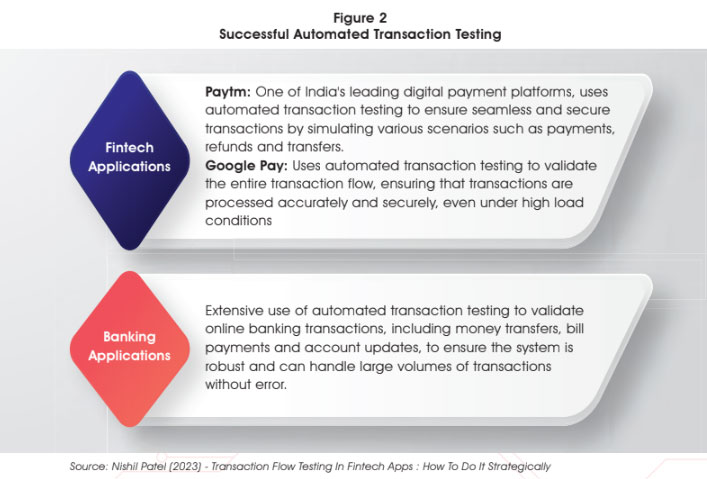

ii. Automated Transaction Testing

Automated transaction testing leverages AI to simulate and validate transactions within a system to ensure they are processed correctly. This involves creating test cases that mimic real-world scenarios and running them through the system to check for any discrepancies or errors. By automating this process, organisations can ensure that their transaction systems are robust, accurate, and reliable, reducing the risk of financial errors and enhancing overall data integrity. Some successful automated transaction testing came from Fintech and financial institutions as shown in Figure 2 below:

iii. Improving Data Accuracy and Reliability

Improving data accuracy and reliability involves implementing robust data validation processes, ensuring that data is consistently collected and maintained, and using advanced analytical tools to detect and correct errors. This can include regular audits, automated error-checking algorithms, and comprehensive training for data handlers. By improving these practices, organisations can ensure that their data is trustworthy, leading to more informed decisions, increased operational efficiency and better overall results.

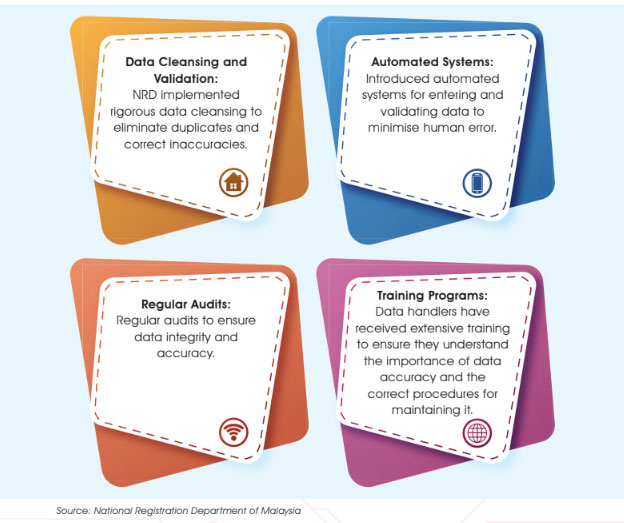

A notable example of improving data accuracy and reliability in Malaysia is the National Registration Department (NRD). The NRD undertook a comprehensive data governance initiative to improve the accuracy and reliability of its citizens’ records. This involved the following processes as shown in Figure 3 below:

As a result, the NRD has significantly improved the reliability of its data, which is critical to several government functions, including issuing identification documents and maintaining accurate population statistics. This initiative not only improved operational efficiency, but also increased public confidence in the department's services.

iv. Cost and Time Efficiency

AI-powered drones can significantly reduce the time and cost of traditional audits, particularly for inventory checks, infrastructure inspections and environmental assessments. They can cover large areas and account for assets such as vehicles or equipment, reducing the need for manual labour and travel. Drones capture high-resolution images and video from multiple angles, ensuring accurate data collection that minimises human error in audits. This enables auditors to perform 100% inventory counts.

For example, Ernst & Young (EY) and PricewaterhouseCoopers (PwC) have used drones to improve inventory audits. An EY project used drones to autonomously scan barcodes and QR codes in large warehouses. Meanwhile, PwC is using drones to measure the volume of coal piles. Traditionally, this task required auditors to climb over the coal piles, which was time-consuming and posed a safety risk.

Boosting Accountability Through AI

Public sector audit plays a vital role in ensuring the integrity and efficiency of government operations. By providing unbiased assessments, audits help to build trust between the government and its citizens by reassuring the public that their taxes are being used effectively and responsibly. In addition, audits improve financial management by identifying areas where financial controls can be strengthened, thereby reducing financial risks and improving budgetary control. They also promote accountability by holding public officials to account for their actions and decisions, ensuring transparency and performance. In addition, regular audits facilitate the continuous improvement of government processes and systems, leading to more effective and efficient delivery of public services. These important accountability functions can be enhanced through AI.

i. Transparency in Audit Processes

AI can significantly improve audit transparency by providing unbiased and comprehensive analysis of financial transactions, operational procedures and regulatory compliance. AI systems can quickly process large volumes of data, identifying anomalies or patterns that may indicate fraudulent activity or inefficiency. Machine learning algorithms allow these systems to improve over time, identifying new types of risks as they emerge. Coupling AI with blockchain technology ensures tamper-proof, transparent transaction records, improving compliance and building trust with investors, regulators and the public by ensuring that all actions are traceable and verifiable.

ii. Real-Time Monitoring and Reporting

By integrating AI with monitoring systems, organisations can continuously track operations and receive instant reports on various performance metrics and risk indicators. AI enables proactive management by immediately alerting relevant personnel when certain thresholds are exceeded, or unusual activity is detected. This real-time capability ensures that issues can be addressed promptly before they escalate into major problems. It also enables more dynamic decision-making based on current data rather than relying on historical reports. This continuous monitoring and instant reporting improve the organisation's ability to respond quickly to change and maintain operational efficiency.

iii. Reducing Human Errors and Biases

AI can significantly reduce human error and bias by ensuring consistent and objective performance. Unlike humans, AI does not suffer from fatigue or personal beliefs that might influence decisions. This consistency is particularly useful in tasks like data entry verification or complex decision-making, where impartiality is essential. Ultimately, AI delivers more accurate and fair results, boosting reliability and credibility.

Challenges And Limitations

Although the implementation of AI offers significant benefits, particularly for auditors, there are certain challenges that need to be addressed. Some of the notable characteristics identified include:

i. High Upfront Costs

Implementing AI audit tools can require a significant initial investment. Purchasing the necessary software can be expensive, especially if it involves advanced features or enterprise-level solutions. To support new software, organisations may need to upgrade their existing hardware, such as servers, computers and network equipment. For example, the cost to implement the NADM’s Digital Public Infrastructure (DPI) service to improve public services in line with the NADM's Digitalisation Strategic Plan for a period of five years from 2021 to 2025.

ii. Data Quality and Bias

Ensuring data quality and mitigating bias are critical challenges in AI-powered auditing. Poor data quality can lead to inaccurate insights, while biased data can lead to unfair or incorrect conclusions. For example, if an AI system auditing public health spending relies on data that is biased towards urban areas, it could miss discrepancies in rural health spending. This could lead to an unfair allocation of resources, further disadvantaging rural communities. To avoid such problems, auditors need to ensure that the data they use is accurate, comprehensive and representative of all demographic groups, thereby enabling fair and accurate audit results.

iii. System Reliability

The reliance on technology means that system failures or cyber-attacks can disrupt the audit process. Today, all public sector organisations rely heavily on technology to produce reports, especially when producing a full set of financial statements running into billions of ringgits. For example, the Employee Provident Fund (EPF) announces annual dividends to its contributors, based primarily on its financial performance. While the use of technology for data management is beneficial, the information must be protected from system failure to safeguard the interests of its nearly 16 million members.

iv. Integration Challenges

Implementing AI solutions within existing systems can be complex and time-consuming. Legacy systems may not support AI technologies, requiring significant modifications or even complete overhauls. AI tools may use different data formats or communication protocols, requiring custom interfaces or middleware. During the data migration phase, aligning data fields between legacy systems and new systems often requires detailed mapping and validation. Ensuring that data is transferred accurately and without loss or corruption can be a significant challenge for IT.

v. Data Security

Cyber-attacks typically involve malware, ransomware, phishing and other forms of cybercrime designed to steal or compromise data. Ensuring the security of sensitive data is a major concern when it comes to personal information such as social security numbers, credit card details and health records that should be kept confidential. Measures such as incorporating access control, preparing data for encryption, and regularly auditing and monitoring for suspicious activity and remediation of vulnerabilities. In addition, regular backup and recovery is required to ensure that data can be recovered in the event of a breach or loss.

The implementation of AI in public sector auditing should be supported by a defence system that can protect the platform and data from breaches and provide possible features for the entire system. The Malaysia Cyber Security Strategy (MCSS) 2020-2024, which consists of five core pillars, 12 strategies and 35 action plans, outlines the country's cyber security agenda, including legislative initiatives such as the Cyber Security Act, capacity building for cyber security professionals, promoting public-private collaboration and strengthening international relations. For example, the government is also in the process of tabling the Cybersecurity Bill in Parliament, which highlights the need to prepare for the continuous evolution of AI technology to maintain a proactive stance against cyber threats. The forthcoming legislation aims to provide a robust legal framework for cyber security, addressing issues such as cyber-crime, data protection and critical infrastructure security.

vi. Ethical and Legal Implications

The integration of AI in auditing raises significant ethical and legal challenges, particularly in relation to privacy and the potential misuse of AI technologies. Auditors must carefully protect sensitive personal data accessed during audits, ensuring that it is used only for its intended purpose and protected from unauthorised access. To maintain public trust, auditors must carefully navigate these issues and avoid surveillance that goes beyond the intended scope. By addressing these ethical implications, auditors can maintain the integrity of their profession while using AI to enhance their audit processes.

vii. Regulatory Framework

A comprehensive legal framework is essential for the oversight of AI applications in public sector audit. Such a framework must ensure compliance with legal standards, protect the privacy rights of individuals, and maintain the integrity of public trust. In practice, regulations could require clear disclosure of the algorithms used in AI-assisted audits, as well as the specific data being analysed. For example, if an AI system is used by a government agency to conduct audits, it would be required to transparently disclose the categories of data under scrutiny, as well as the objectives driving the audit process. This level of openness not only serves to increase public trust, but also ensures that there is a mechanism in place to hold these entities accountable for their use of technology in sensitive areas of the government.

viii. Skill Gaps

The readiness of AI applications for auditors to be trained in the use of these new digital tools, which can be a barrier to adoption. This includes the understanding of how data analytics work, cybersecurity and the use of specialised software for auditing. Training programmes and continuous learning need to be comprehensive, covering both theoretical knowledge and practical application. By mastering AI technology, it will make individual auditors be more productive. This will help companies to increase productivity per employee.

ix. Resistance to Change

There may be resistance from staff accustomed to traditional methods. Some auditors may be reluctant to adopt new technologies due to their comfort with traditional methods or fear of the unknown. Effective training can help mitigate this by demonstrating the benefits and ease of use of digital tools. Resistance may also come from management or auditees, where limited knowledge of AI and its benefits may lead to reluctance to adopt new technologies. For example, the public and other stakeholders may have trust issues with AI, fearing that it may not be as reliable or transparent, or concerned about who is responsible for the decisions being made by the AI system.

Future Prospects

Artificial Intelligence has significant potential to revolutionise public sector audit by improving efficiency, accuracy and openness. It can automate repetitive tasks such as data entry and analysis, allowing auditors to focus on more complex tasks. As AI continues to develop, its incorporation into public sector auditing is expected to strengthen audit processes and improve governance and accountability.

Emerging AI Technologies in Auditing

Emerging AI technologies in auditing such as advanced data analytics, machine learning algorithms and robotic process automation (RPA), are changing the auditing landscape. These technologies enable auditors to quickly and accurately analyse large data sets and identify anomalies or patterns that may indicate fraud or error. In Malaysia, where digital transformation is a national priority under the Malaysia Digital Economy Corporation (MDEC), AI can significantly improve auditing efficiency. For example, implementing RPA for routine compliance checks can free up human auditors to focus on the more complex tasks, improving overall audit quality and effectiveness.

Potential For AI To Transform Public Sector Audits

AI has the potential to revolutionise public sector audit by assisting in risk assessment, control testing and continuous monitoring of transactions. This shift can lead to more proactive and predictive, rather than reactive, audit processes. In Malaysia's public sector, where accountability and transparency are critical, AI can provide real-time insights into government spending and performance. In a practical scenario, AI-driven analytics could be used to monitor procurement processes across different government departments to identify inefficiencies and signs of corruption, thereby increasing transparency and trust in public administration.

Recommendations For Policymakers and Auditors

For policymakers and auditors in Malaysia considering integrating AI into their practices, several recommendations are essential. Investing in training programmes to develop the necessary skills to work with AI technologies is crucial. In addition, establishing clear guidelines on data privacy and ethical considerations related to the use of AI is essential. Policymakers should also create innovation-friendly regulations that encourage experimentation with new technologies, while ensuring robust oversight mechanisms. For example, developing a regulatory sandbox for AI in auditing could allow for controlled testing and refinement of AI applications, fostering innovation while maintaining high standards of accountability and transparency.

Malaysia's digitalisation policy, primarily driven by the My DIGITAL initiative and the Malaysia Digital Economy Blueprint, aims to transform the country into a digitally driven, high-income nation and a regional leader in the digital economy. The key objectives of Malaysia's digitalisation policy are to enhance economic growth through the use of digital technologies, improve the quality of life for all Malaysians through digital inclusion, and position Malaysia as a competitive force in the global digital economy. One of the objectives is to foster an integrated ecosystem that enables society to embrace the digital economy. There are three phases of the MyDIGITAL initiative, starting with Phase 1 (2021- 2022): Strengthening the basis for digital adaptation. Phase 2 (2023-2025) focuses on driving inclusive digital transformation, and Phase 3 (2026-2030) focuses on positioning Malaysia as a regional leader in digital content and cybersecurity.

There are also several guidelines and codes of ethics being developed for the public sector in relation to AI. The two main ministries involved are the Ministry of Digital and the Ministry of Science, Technology and Innovation (MOSTI). They are researching and developing an Artificial Intelligence Ethics and Governance Code (AIGE) to ensure the responsible development and implementation of AI. These guidelines emphasise principles that are in line with the country's religious, cultural, identity and legislative will. There is also the National Blockchain and Artificial Intelligence Committee (NBAIC), led by the Ministry of Higher Education, which is responsible for setting strategic goals and aligning and monitoring initiatives in the Pelan Hala Tuju Kecerdasan Buatan Negara 2021 - 2025. The guidelines include seven principles to help AI controllers while ensuring safe use for the public. The seven principles of AI include fairness, secondly trustworthiness, security and control, thirdly privacy and security, fourthly agility, fifthly continuity, sixthly accountability, seventhly human benefit and happiness.

Artificial Intelligence is revolutionising public sector auditing by improving accuracy and accountability through technologies such as data analytics, anomaly detection and automated transaction testing. These advances improve data reliability and reduce human error and bias, while real-time monitoring and transparency increase accountability. However, challenges remain, including data privacy, system integration and skills gaps. As emerging AI technologies continue to evolve, they have the potential to significantly transform public sector auditing, so it is critical for policymakers and auditors to stay informed and adapt accordingly.

Way Forward For AI in Public Sector Auditing

Integrating AI into public sector auditing in Malaysia offers a transformative opportunity to improve audit quality, efficiency and transparency. AI can quickly analyse large amounts of data, identifying patterns and anomalies that may be missed by human auditors. This capability allows for more comprehensive and accurate audits, leading to better detection of errors and fraud. In addition, AI can automate routine tasks, freeing auditors to focus on more complex and high-risk areas, increasing overall audit efficiency. Real-time monitoring enabled by AI can also ensure continuous auditing and timely detection of issues.

However, the successful implementation of AI in public sector auditing in Malaysia requires overcoming several challenges. Significant investment in training and education is required to equip auditors with the necessary digital skills. The initial setup and maintenance costs of AI systems can be significant, posing a financial challenge. In addition, robust governance frameworks need to be put in place to manage the implementation of AI, ensure data security and address ethical considerations. By investing in training, ensuring strong governance and fostering collaboration between government agencies, academic institutions and private sector experts, Malaysia can effectively harness the potential of AI to modernise public sector auditing.

To effectively integrate AI into public sector auditing, Malaysia should invest in comprehensive training programmes and foster a culture of continuous learning for auditors, establish robust governance and ethical frameworks with clear guidelines and stringent data security measures, encourage collaboration through public-private partnerships and pilot projects, and address financial constraints by securing funding and conducting cost-benefit analysis to ensure significant returns on AI investments.

References

Anita Dennis (2024) Journal of Accountancy AICPA & CIMA: What AI Can Do for Auditors : https://www.journalofaccountancy.com/issues/2024/feb/what-ai-can-do-for- auditors.html

IBM (2024) IBM, What is a machine learning algorithm? Centre for Technology and Management Education, What is Machine Learning? A Comprehensive Guide for Beginners 12 February 2024 : https://www.ibm.com/topics/machine-learning- algorithms

Nishil Patel (2023) Transaction Flow Testing in Fintech Apps: How to Do It Strategically

Swift (2024) Financial News UK – Swift to launch AI-Powered Fraud Defence to Enhance Cross-Border Payments 16 October 2024: https://www.swift.com/news-events/press- releases/swift-launch-ai-powered-fraud-defence-enhance-cross-border-payments