“Whether it be detecting fraudulent activities, or optimising compliance processes, AI-driven solutions empower auditors to adapt to an ever-changing environment and deliver actionable insights that drive informed decision-making. With the rapid advancement of AI, machine learning, and data analytics, traditional methodologies are being redefined, offering unprecedented opportunities for innovation and efficiency”

Shri Girish Chandra Murmu,

(Former Comptroller and Auditor General of India)

Introduction: Leveraging AI for a New Era of Auditing in India

As India stands on the cusp of a technological revolution, the field of auditing is experiencing a significant transformation. The vision of the Comptroller and Auditor General (CAG) of India is to leverage Artificial Intelligence (AI) as a catalyst for positive change, enabling auditors to unlock deeper insights, make well-informed decisions, and create greater value for the nation. This vision aligns with the Government of India's efforts to position the country as a global leader in AI innovation as in 2024, India holds the chairmanship of the Global Partnership on Artificial Intelligence (GPAI), underlining its commitment to integrating AI into governance practices.

AI has emerged as a powerful tool in the auditing landscape, offering vast potential to improve efficiency, effectiveness, and insight. By automating routine tasks, AI allows auditors to focus on more strategic analyses and high-value activities, thus enhancing the quality of audit outcomes. Advanced AI algorithms and predictive analytics can process massive datasets with unprecedented speed and accuracy, revealing hidden patterns, anomalies, and potential risks that were previously difficult to detect. This new capability significantly strengthens the role of auditors in maintaining transparency and accountability in public finance.

AI Applications in Tax Administration: Enhancing Efficiency and Compliance

In the realm of tax administration, the Central Board of Indirect Taxes and Customs (CBIC) has taken notable steps in using AI and data analytics to improve compliance and streamline processes. A key initiative in this direction is Project ADVAIT (Advanced Analytics in Indirect Taxes), launched in 2021. ADVAIT uses predictive analytics and pattern recognition to identify tax evasion and optimise revenue collection. It also provides interactive dashboards and models that assist CBIC officers in tasks like tax compliance monitoring and reporting, thus making tax administration more effective.

Similarly, the GST department has developed an AI-driven system that automates the scrutiny of GST returns by cross-referencing data from multiple sources, including bank transactions, invoices, and tax returns. This system ensures accuracy and consistency in taxpayer information, reducing manual interventions and minimising errors. When discrepancies are detected, the system automatically notifies taxpayers, allowing them to rectify any issues promptly. Such AI-enabled automation has significantly improved the efficiency of tax administration.

Infosys has also played a key role in these advancements through its Business Intelligence and Fraud Analytics (BIFA) system, developed for India's GST Network (GSTN). BIFA uses machine learning and data analytics to identify suspicious transactions and assess risks, aiding in the targeted scrutiny of high-risk entities. This sophisticated system supports the CBIC in enhancing the transparency and accountability of the GST regime, contributing to a more robust and data-driven approach to tax administration.

Adopting AI in Public Auditing: A Proactive Approach to Oversight

CAG (SAI India) is responsible for auditing government expenditures and ensuring transparency in public financial management. By integrating AI into its audit processes, auditors could achieve more thorough oversight of public funds and improve the accuracy of audits. Traditional auditing methods often rely on manual analysis of financial records, which can be time-consuming and may limit the scope of audits. AI can streamline these processes by enabling rapid analysis of large and complex datasets, allowing auditors to detect patterns and potential irregularities that might otherwise go unnoticed.

The use of AI in tax administration, exemplified by Project ADVAIT and AI-based GST return scrutiny, demonstrates its effectiveness in detecting non-compliance and fraudulent activities. By adopting similar tools, SAI India can shift from a reactive to a proactive auditing approach, focusing on areas with higher risks. This shift would enhance the SAI’s ability to detect fraud, ensure the proper use of public funds, and make evidence-based policy recommendations. Embracing AI would thus help the CAG maintain its vital role as a guardian of transparency and accountability, especially in the face of increasingly complex government operations.

AI could also be used by SAIs for performance audits, to assess the effectiveness of government programs. AI's capacity to analyse extensive datasets allows it to provide insights into whether these programs are meeting their intended goals. This approach offers a more comprehensive evaluation, moving beyond traditional audit metrics to ensure not only financial compliance but also the efficient delivery of public services.

CEDAR’s Role in Advancing AI and ML: Opportunities for GST Audits

The Centre for Excellence in Digital Audit of Revenue (CEDAR), a specialised wing in the office of Principal Director of Audit(Central), Bengaluru is designed to facilitate data analytics and a digital audit of revenue, is currently exploring the use of machine learning (ML) and artificial intelligence (AI) to enhance its audit processes, particularly for Goods and Service Tax (GST) audits. This initiative aims to improve risk identification, boost fraud detection, and assist in developing audit guidelines.

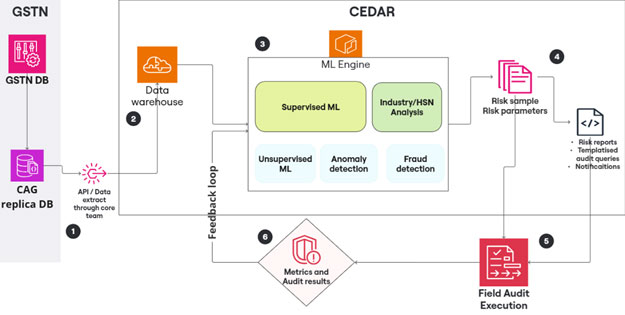

Fig: 6-step process for the use of AI and ML in GST Audit

The proposed application of machine learning in the audit process flow involves several key concepts aimed at enhancing the accuracy and efficiency of GST audits. One of the primary approaches is Multivariate Analysis, which will utilise both supervised and unsupervised ML models.

Supervised Model for Known Risk Patterns: The supervised model will analyse risk parameters and create a multivariate model based on risk dimensions identified in previous GST audits, such as Phase I and II of Centralized Audit and Detailed Audit under Subject Specific Compliance Audit on the Department’s Oversight on Returns Filing and Tax Payment (DORF). It will also incorporate ratios from desk reviews conducted before the start of field audit and use audit results from these phases to form the training datasets. The model will evolve over time, incorporating new audit results and updates to return formats, to better predict deviations based on historical data.

Unsupervised Learning for Detecting Hidden Patterns: In contrast, the unsupervised ML model aims to detect hidden patterns in audit data without relying on predefined risk labels. This model would analyze data from DORF-I and II to identify anomalies that could indicate potential risks. Such an approach could reveal previously undetected patterns, expanding the scope of risk detection and enabling a more proactive identification of audit targets.

Sectoral and Industry Analysis Using Machine Learning: The CEDAR team is also contemplating using ML for sectoral and industry analysis. By utilising data, including the more stringent HSN (Harmonized System of Nomenclature) codes introduced in April 2021, the ML models would be built to detect outliers within specific industries and geographic regions. This sectoral analysis will assist in risk selection for audits and guide the identification of risky or tax evasion-prone industry-specific audit topics for future investigations.

Fraud Detection and Anomaly Assessment Through AI: The ML models would aid in anomaly detection and fraud risk assessment. The models could analyse taxpayers' behaviour by assessing various financial ratios to spot unusual transactions. To detect deliberate omissions and recurring patterns, the model will focus on identified risk areas to detect potentially fraudulent activities. Even though our current audits may not have yielded direct evidence of fraud, these rules can be tested against cases flagged as fraudulent by the department.

AI-Assisted Audit Design Matrix and Guideline Creation

The CEDAR initiative envisions a future where AI not only detects risks but also assists in automating the preparation of audit guidelines. A Large Language Model (LLM), trained with knowledge of relevant statutes, rules, and notifications, could use the insights generated by the ML models to draft Audit Design Matrix (ADM) documents and guidelines for upcoming GST audits. This integration would help streamline the audit process, providing auditors with a ready-made framework for addressing complex audit issues.

Challenges and Future Directions for AI in Auditing

Despite the potential benefits, certain challenges need to be addressed in implementing these technologies, primarily related to data quality and availability. For instance, a significant portion of data from Phase I and II of SSCA on DORF audits remains unavailable due to delays in receiving responses. Additionally, the varying skill levels of audit staff could impact the consistency of the training datasets. The dynamic nature of GSTN returns, with its frequent updates and structural changes, also poses a challenge for maintaining the accuracy of the ML models over time.

Looking ahead, the CEDAR team aims to develop a user interface (UI) that would enable auditors to interact directly with these ML models. This interface would simplify the process of selecting appropriate models and applying them to specific audit requirements, making the benefits of AI accessible to a broader range of auditors. Through such initiatives, SAI India could ensure that its auditing processes remain robust, adaptive, and capable of addressing the complexities of modern taxation systems.

This forward-thinking approach by the CEDAR wing highlights the potential for AI and ML to transform public auditing. By leveraging these technologies, SAI India can improve the efficiency of its audits, enhance fraud detection capabilities, and provide valuable insights into the management of public resources, setting a benchmark for future advancements in government auditing practices.

Collaborations and Building the Future of AI-Driven Auditing

To fully integrate AI into its auditing processes, the CAG would need to build a centralised data repository that consolidates financial data from various government entities. This approach would mirror the CBIC’s data infrastructure, facilitating a unified view of financial information. With access to such a repository, the CAG could use advanced AI tools like natural language processing and machine learning to analyse financial documents, audit reports, and contracts. This would enable the automatic identification of inconsistencies or non-compliance, allowing auditors to focus on more complex aspects of financial oversight.

We can adopt AI-driven tools that are designed to assist in auditing tasks, such as text mining, natural language processing (NLP), and machine learning. These tools can analyse audit reports, contracts, and financial statements, detecting inconsistencies, anomalies and non-compliance issues. The automation of routine audit checks would allow auditors to focus on more complex, strategic assessments of financial records.

Lastly, in-house applications can support in accomplishing our mission, but given the technical expertise required to implement AI solutions, we could benefit from partnerships with technology firms, as seen in the GSTN's collaboration with Infosys for Business Intelligence and Fraud Analytics. We should apart from using our in-house expertise should try to foster collaborations with Tech companies to explore other unknown dimensions.

Conclusion: AI as a Tool for Transparency and Accountability

By adopting AI, SAI India can ensure that its audit processes remain efficient and adaptive to the evolving demands of public financial management. This transformation aligns with India’s broader vision of using AI to enhance governance and create a more transparent, accountable, and data-driven public administration. The initiatives undertaken by the CEDAR wing thus reflect a forward-thinking approach, positioning the CAG to continue playing a pivotal role in ensuring the integrity of government finances in a rapidly changing technological landscape.