Styliani Tori

Judge Rapporteur in the HCA

- The Process of Conducting Thematic Audits

- Follow-up Results

- Challenges and Conclusions

The Hellenic Court of Audit (HCA) stands as both the supreme financial court and the supreme audit institution in Greece. It carries out its jurisdictional, audit, and advisory functions in a way that guarantees the observance of the rule of law, financial sustainability, and fair trial. Moreover, the Court oversees the compliance of all public bodies with principles of legality, regularity, and good governance, ensuring public accounting officers’ accountability.

The HCA operates independently from the legislative, executive, and other branches of the judiciary, maintaining full autonomy in its functions. Its audits adhere to internationally recognised best practices and auditing standards, ensuring not only the highest quality but also transparency, accountability and alignment with global oversight frameworks. In accordance with the Greek Constitution, the Organic Law of the HCA, and the Rules of Procedure for its Administrative and Audit Units, the HCA conducts thematic audits, including performance audits and internal control systems audits. These audits are incorporated in the HCA’s Annual Audit Plan, alongside the audit of the state's financial statements and balance sheet, as well as those of local government organisations and other state legal entities, which are conducted at least once every four years, as well as pre-contractual audits.

The strategy for performance audits is primarily shaped by the President of the Court, who consults with staff to ensure that audits address significant areas of public concern while also incorporating a comprehensive risk assessment. The multiannual and annual audit programs focus on key areas such as fiscal sustainability, the welfare state, the rule of law, and sustainable development. Notably, performance audits are cross-sectoral, covering multiple entities and reflecting the interconnected nature of the issues under review.

The HCA’s Annual Audit Program is drafted by the Eighth Chamber, headed by the President of the Court, taking into account mandatory audits, Parliament’s requests, and proposals from public officials or citizens. Once drafted, the annual program is submitted to the Plenary of the Court, which consists of independent, supreme judges. It is essential to note that the HCA maintains full autonomy, giving due consideration to audit requests from executive or legislative bodies without being bound in any way to incorporate them in its annual planning.

Each performance audit is accompanied by an Audit Planning Memorandum, which includes a detailed questionnaire sent to the audited entities. A supervising judge is assigned to each audit, supported by the Directorate "Quality Control", ensuring adherence to auditing standards throughout the process. The HCA maintains rigorous quality control at two stages: ex-ante and ex-post quality checks. Audit work is carried out by the Audit Directorates at the HCA's Head Office, collaborating with 94 other Directorates across Greece.

The HCA employs a specialised information system to monitor audits, ensuring that findings are based on thorough investigations and that as many relevant cases as possible are included. In cooperation with the criminal justice system, the Court respects the independence of its audit work, but will refer cases to the appropriate authorities when criminal offences are discovered during audits.

During audits, the HCA uses detailed questionnaires to collect data from audited entities. If an entity admits to non-compliance in its response, this admission is accepted as an audit finding. If the entity claims compliance, the reliability of their response is carefully scrutinised. All findings are thoroughly documented, and when a violation is found, appropriate authorities, including public prosecutors, are notified. In the event that an irregularity (deficit) is discovered during the audit, the competent Judicial Section of the Court is responsible for the imputation.

Subsequently, the Specific Preliminary Findings of each audit are communicated to the audited entities, which must respond within a specified timeframe. Once the audit is concluded, the HCA issues a Final Audit Report, which includes recommendations based on the principles of economy, efficiency, effectiveness, and proportionality. These recommendations are aimed at enhancing the performance and compliance of public bodies. The final report is distributed to the audited entities, relevant similar bodies, and sent to the Greek Parliament. The Court ensures that public entities act on these recommendations, monitoring compliance within a set timetable, typically no longer than two years.

Each performance audit report included in the HCA's Annual Audit Programme is submitted to the Parliamentary Committee on Institutions and Transparency before being published on the Court’s website and distributed to the press.

In a rule-of-law state, accountability is closely tied to sound financial management and the performance of public bodies. Public entities are required to manage resources transparently and to report on how they fulfil their public missions. The annual financial statements of public legal entities, which reflect the management of public funds, must be submitted to the HCA on time, ensuring transparency and reliability in the management of public resources.

The HCA’s 3/2024 performance audit report, titled Fiscal Discipline and Transparency in Public Legal Entities, examined 70 public bodies, including local government organisations, universities, hospitals, and more. The report identified reasons for delays or non-submission of financial statements and provided valuable insights into improving financial practices within public institutions.

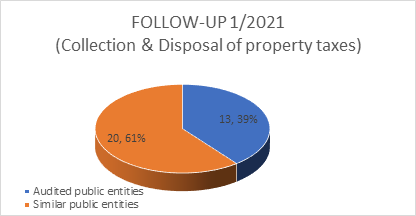

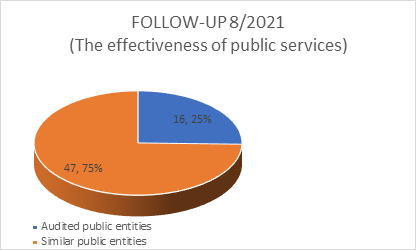

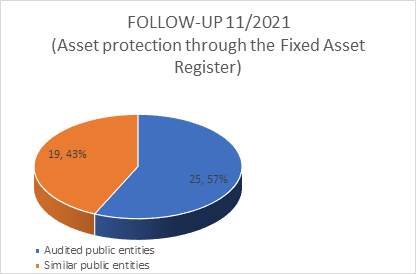

Additionally, the HCA conducts compliance audits on previous years’ reports to ensure that entities follow through on the recommendations provided. For instance, in the 2021 audit reports on various issues, such as the collection and disposal of property taxes, the effectiveness of public services, and asset protection through the Fixed Asset Register—follow-up audits tracked the implementation of corrective actions.

The impact of these audits is clear: many public bodies beyond the audited ones are required to comply with the Court's recommendations. Non-compliance leads to accountability measures, ensuring that public entities rectify identified deficiencies.

Despite the substantial progress made, some challenges remain. General and vague recommendations can sometimes be challenging to implement, particularly for smaller entities such as municipalities, which often face staffing shortages or resource constraints.

However, the HCA’s thematic audits continue to play a vital role in overseeing the actions of public bodies, uncovering systemic weaknesses, and recommending reforms to modernise public administration. The publication of audit reports, along with the entities' responses, increases transparency, allowing citizens to better understand the allocation and effectiveness of public spending, in line with democratic principles and the rule of law.

Ultimately, the Hellenic Court of Audit serves as a guardian of effective public financial management in Greece, promoting good governance and the efficient use of public funds. Through performance audits and rigorous follow-up procedures, it ensures that public bodies are held accountable and continuously improve in their mission to serve the public interest.