Ni Putu Maitri Nara Suari

The Audit Board of The Republic of Indonesia

Introduction

Performance audits have gained renewed importance in Indonesia as part of broader efforts to improve transparency and accountability in the public sector. Globally, since the 1980s, many Supreme Audit Institutions (SAIs) have expanded their mandates to include performance audits or, in some countries, known as value-for-money audits, assessing whether government programs are achieving their intended results efficiently, effectively, and economically (Hazgui et al., 2022). This reflects the transition in the public sector from the New Public Management (NPM) approach—an emphasis on positioning the public sector within a market-driven economy to achieve efficiency as an organisational goal—to a focus on Public Value creation, which prioritises generating outcomes and impact on society (O’Flynn, 2007).

In Indonesia, Law Number 15/2006 grants the Audit Board of the Republic of Indonesia (BPK) the authority to conduct financial audits, special purpose audits, and performance audits. Performance audits serve as a strategic tool to ensure accountability and transparency (Andrianto et al., 2021), enabling government programs not only to adhere to financial regulations but also to achieve meaningful outcomes and impact on society.

This article presents BPK, as Indonesia’s Supreme Audit Institution (SAI) has an evolving role in strengthening public sector accountability through performance audits. It will discuss the recent implementation of performance audits and how performance audits are able to drive public sector accountability, the challenges BPK has faced, alongside opportunities and conclusions from its efforts to embed performance audits within the governance framework.

Recent Implementation of Performance Audit in Indonesia

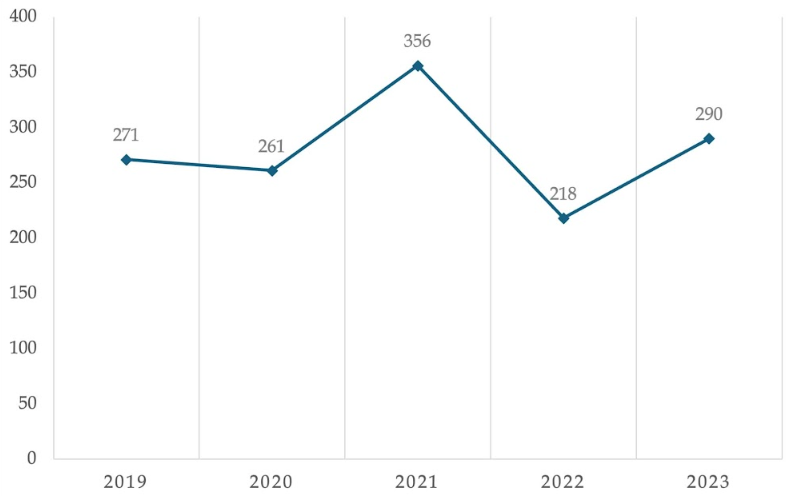

Between 2019 and 2023, performance audits in Indonesia saw significant growth. The increase was attributed to enhancements in financial statement audits, prompting BPK to shift its focus towards conducting more performance audits, although these remain voluntary rather than mandatory (Setyaningrum et al., 2025). The number of performance audits from 2019 to 2023 can be seen in Figure 1.

Figure 1. The Number of Performance Audits From 2019 to 2023

BPK has intensified its use of thematic performance audits since 2011 to evaluate the economy, efficiency, and effectiveness (3Es) of key national programs (Andrianto et al., 2021; Setyaningrum et al., 2025). The percentage of thematic audits in BPK increased significantly after 2016, reaching 72.66% of total performance audits in 2018 (Andrianto et al., 2021). According to BPK’s performance report, one of the strategic efforts undertaken by BPK is aligning the audit theme with Indonesia’s National and Regional Medium-Term Development Plans (RPJMN/RPJMD) 2020-2024 while simultaneously considering the integration of Sustainable Development Goals (SDGs) into these agendas. This alignment ensures that audits are not only responsive to national development priorities but also support global sustainability commitments. In executing SDG-related audits, BPK utilises the IDI’s SDGs Audit Model (ISAM), a structured approach based on international standards (ISSAI), to assess policy coherence and performance outcomes

The implementation of thematic performance audits is further strengthened by BPK’s emphasis on cross-unit collaboration. This cross-unit collaboration ensures that performance audits generate not only technically sound findings but also comprehensive recommendations that support wider public governance reforms and institutional accountability.

For example, BPK conducted a thematic performance audit on one of the Government of Indonesia’s priority programs aimed at accelerating the reduction of stunting prevalence during the 2022-2023 period. Given the cross-unit collaborative approach, the audit involved auditors from both BPK’s central office who are responsible for examining relevant technical ministries at the national level, such as the Ministry of Health, the National Population and Family Planning Board (BKKBN), the National Agency of Drug and Food Control (BPOM), as well as auditors from regional representative offices who assessed the program across 44 local government. The audit revealed several critical findings that, if left unaddressed, could compromise the effectiveness of the program. Key issues included the need to improve the proper integration of policies into planning documents and inadequate execution of data recording and reporting within the relevant information systems.

Performance Audit as a Driver of Public Sector Accountability

Beyond their implementation, some studies showed that performance audits worked as a robust accountability tool for the public sectors. A recent empirical study from Setyaningrum et al. (2025), which surveyed 180 auditees across ministries, agencies, and local governments that underwent performance audits between 2020 and 2022, revealed significant improvements in organisational governance and responsiveness to audit recommendations. The key areas of performance audit impact include strategic shifts in planning, enhanced procedures, improved risk management, regulatory updates, and strengthened governance, which relate to an increase in accountability.

Respondents rated the audits’ usefulness as high in quality and practical in utility, with clear connections between the audit criteria, evidence, and resulting evaluations. This clarity not only reinforced the technical reliability of audits but also increased their legitimacy in the eyes of public officials, which made them more likely to act on recommendations (Setyaningrum et al., 2025).

Similarly, Haliah et al. (2020) found that performance audits in multiple countries, including Indonesia, can enhance accountability when conducted with high-quality methodologies, audit reports, and recommendations. Aligning with these findings to contribute to public sector accountability, BPK has taken steps to strengthen its performance audit framework. Since performance audits were introduced in 2006, BPK has strengthened its audit capacity through bilateral partnerships with other Supreme Audit Institutions such as the Australian National Audit Office (ANAO) and secondment in various SAIs to gain experience and constructive feedback for a better performance audit framework. From 2011 to the present, when this phase marks the maturity of BPK’s performance audit methodology, the adoption of thematic audits has increased, which aligns with Indonesia’s National Medium-Term Development (RPJMN) (Andrianto et al., 2021).

Challenges and Opportunities

Despite the impact of performance audits in strengthening accountability, they may face several challenges. Despite BPK’s audit results in detailed reports with policy recommendations, the implementation depends on institutional readiness and effective mechanisms for follow-up. Talbot and Boiral (2023) argued that a common issue in performance audits is that public organisations may formally accept audit recommendations but face difficulties in integrating them into actual policies and programs. These might be driven by resource constraints where agencies lack the necessary funding or personnel to fully implement recommendations, or variability in enforcement where different organisations may respond to audits with different levels of urgency.

BPK has made significant progress in adopting technology, establishing a robust framework, maintaining a thematic focus, and fostering cross-agency collaboration. However, it is essential to recognise the key opportunities for further strengthening public sector accountability through performance audits. BPK could optimise its use of current technology (Andrianto et al., 2021), including optimising for using BPK Big Data Analytics System (BIDICS), Standardised and Integrated Audit Process (SIAP) for performance audit, follow-up monitoring information systems (SIPTL), and the latest technology of Artificial Intelligence for Data Analytics (AIDA) to support evidence-based audits and data governance compliance. Another key opportunity lies in expanding public engagement. While BPK has made audit results publicly accessible, further efforts to encourage citizen participation in the oversight process can strengthen accountability. This engagement can generate external accountability pressure on government agencies to act on audit recommendations (Brinkerhoff & Wetterberg, 2013; Talbot & Boiral, 2023). Lastly, performance audits could be further institutionalised, such as making performance audits a mandatory part of governance and policy evaluation (Setyaningrum et al., 2025). This would ensure a more consistent approach to using performance audits as an important tool to strengthen public sector accountability.

Conclusion

Indonesia’s experience with performance audits highlights their growing role as a tool for strengthening public sector accountability. BPK’s shift toward thematic audits, alignment with national priorities, and efforts to enhance audit capacity demonstrate meaningful progress. However, the effectiveness of performance audits depends not only on producing findings but also on the public institution’s readiness and commitment to act on performance audit recommendations.

Key lessons indicate that public sector agencies with strong leadership, sufficient resources, and skilled personnel are better equipped to implement audit recommendations. Moreover, citizen participation has an essential role in reinforcing accountability and increasing audit impact. Lastly, institutionalising performance audits within the governance system can transform them from oversight tools into drivers of policy learning and continuous improvement for the public sector to create public value. By reflecting on these lessons, BPK and other institutions can continue to elevate the role of performance audit in achieving accountable governance.

References

Andrianto, N., Sudjali, I. P., & Karunia, R. L. (2021). Assessing the development of performance audit methodology in the supreme audit institution: The case of Indonesia. Jurnal Tata Kelola Dan Akuntabilitas Keuangan Negara.

Laporan Kinerja Tahun 2024 (Performance Accountability Report 2024).