Ms. Sarah Alazmi

Assistant Auditor

State Audit Bureau of Kuwait

It is essential to activate the concepts of economy, efficiency, and effectiveness across public sector operations and programs. Therefore, a rigorous auditing mechanism is required to examine and evaluate such matters, contributing to improved public expenditure and services while enhancing accountability.

There is a pressing need for an independent auditor who represents the public interest, enabling them to think and act autonomously to accurately reflect the true state of performance of the concerned entities.

To begin, let us explore the concept of performance auditing:

Performance auditing is one of the three principal types of audits endorsed in the 1977 Lima Declaration, which serves as the foundational charter for Supreme Audit Institutions (SAIs). It is classified as Standard No. 1 within the INTOSAI criteria Framework, encompassing fundamental auditing principles, including performance auditing.

INTOSAI defines performance auditing as “an independent, objective, and reliable examination of whether government undertakings, systems, operations, programs, activities, or organisations operate in accordance with the principles of economy, efficiency, and effectiveness, and whether there is room for improvement.”

Despite the various definitions of performance auditing, they all encompass the principles of economy, efficiency, and effectiveness, commonly referred to as the Three E’s.

A Historical Perspective on Performance Auditing in the State of Kuwait

The State Audit Bureau (SAB) of Kuwait has demonstrated a keen awareness of the importance and necessity of keeping pace with the latest advancements in the auditing profession, which demands continuous development in line with the most up-to-date practices and professional criteria to enhance its auditing role. Following the maturation of its auditing experience in financial and compliance auditing, this recognition led to the establishment of the Performance Audit Department in 1999 as one of the core types of auditing practised by SAB.

SAB’s Performance Audit Department plays a vital and effective role in evaluating the efficiency and effectiveness of government entities in executing their mandates in accordance with their founding legislation. This article aims to highlight the significance of performance auditing in enhancing accountability, transparency, and governance within public institutions, while also supporting the legislative authority, represented by the National Assembly, in reinforcing accountability.

Performance auditing is particularly relevant as it addresses issues of direct concern to citizens across various sectors, including education, healthcare, social affairs, employment, and housing. Furthermore, it extends to economic matters related to state investments and the oil sector, as well as emerging topics such as environmental sustainability.

In line with the principles of credibility and transparency, and in an effort to reinforce them, the reports of the Performance Audit Department are publicly available on the official website of SAB, allowing all members of society to access them. This practice aligns with the democratic foundations of the State of Kuwait, which emphasise active participation from all segments of society in the democratic process.

As part of this commitment, a report known as the Citizen’s Report has been issued. Its purpose and significance lie in providing a publicly accessible document characterised by clear and simple language, ensuring that all members of society can easily comprehend it. The report covers a wide range of topics, particularly those of direct relevance to citizens.

An important question arises: What are the key achievements following the implementation of performance auditing in Kuwait, and has it contributed to enhancing accountability in the public sector?

It has been observed that performance auditing in Kuwait applies the concept of constructive auditing, playing a crucial role in assisting public sector officials in enhancing and developing their operations. Consequently, this leads to the improvement of services provided to citizens, thereby contributing to the advancement of Kuwait’s Vision 2035.

Since its establishment until 2019, the department has issued approximately 268 reports across various fields in accordance with its annual work plans. This underscores the significant contribution of performance auditing in strengthening accountability.

The Extent of Government Entities’ Engagement and Responsiveness to Performance Auditing Reports:

Answering this question is of great significance, as it serves as an indicator of whether performance auditing plays an effective role in strengthening accountability within the public sector.

In Kuwait, the reports issued by SAB’s Performance Audit Department have garnered considerable attention from the executive authority. Government entities have demonstrated a positive and proactive response, as evidenced by their commitment to adhering to performance auditing reports and implementing the recommendations outlined therein. This responsiveness reflects the state’s and its institutions’ strong commitment to the public interest and their dedication to enhancing governmental performance.

The Importance of Performance Auditing:

1. Governance: Promoting sound governance within government entities.

2. Accountability: Strengthening accountability by assisting government officials and the legislative authority in improving performance. This is achieved by ensuring that decisions are implemented efficiently and effectively, ultimately delivering added value to citizens.

3. Transparency: Achieving transparency by presenting the outcomes of governmental activities to both the legislative authority and the public.

Objectives of Performance Auditing:

- The overarching goal of performance auditing is to establish effective oversight of public funds.

- Informing the legislative authority of audit findings to support its role in exercising public accountability over the executive authority regarding the management of public funds.

- Assisting the executive authority, decision-making centres, and policymakers in evaluating the quality of adopted policies, identifying weaknesses, and making necessary corrections to enhance their effectiveness.

- Guiding audited entities and units toward optimal approaches for improving performance, optimising resource utilisation, and enhancing management practices to achieve their objectives efficiently.

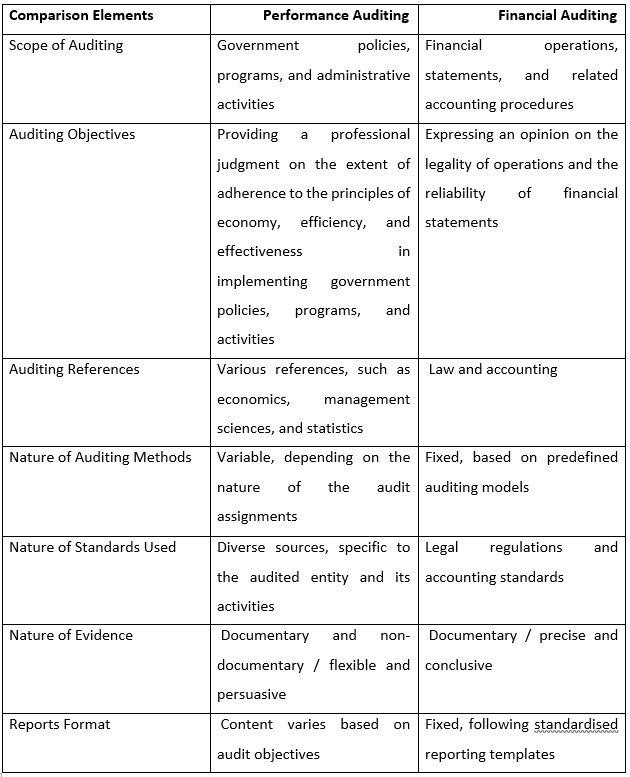

Achieving these objectives necessitates that performance auditing be broad in scope, enabling oversight across all sectors. The extensive reach of performance auditing distinguishes it from traditional forms of auditing, such as financial auditing, by encompassing a wider range of areas. Below is a brief comparison between the two aforementioned types of auditing:

It is worth noting that both financial auditing and performance auditing complement each other, thereby contributing to the enhancement and reinforcement of accountability within the public sector.

The Three E’s is a term that refers to the three fundamental principles upon which performance auditing is based on: economy, efficiency, and effectiveness.

To maximise the benefits of performance auditing in strengthening public sector accountability, it must be applied correctly, ensuring the proper implementation of its underlying principles:

- Economy: Minimising the costs of resources used by ensuring that they are available at the right time, in the appropriate quantity and quality, and at the best possible price. The economy can only be measured effectively if there is a reasonable basis for assessment.

- Efficiency: Maximising the utilisation of available resources by optimising the relationship between inputs and outputs in terms of quantity, quality, and timing. Efficiency also entails the ability to make the best use of resources by streamlining the connection between outputs, whether in the form of services or products, and the resources consumed to produce them.

- Effectiveness: Evaluating the extent to which implemented or planned policies and programs achieve their intended objectives by comparing the set goals with the actual outcomes achieved.

The three principles are deeply interconnected, as no single principle can be fully effective in isolation. These principles complement one another conceptually.

For instance, if we consider the economy alone, ensuring that tasks are accomplished or services are provided at the lowest possible cost, in a timely manner, and with appropriate quality and quantity may not yield the desired benefits if efficiency in resource utilisation is lacking. Without efficiency, the government may fail to optimise the use of resources necessary for carrying out activities or delivering services.

Similarly, focusing solely on effectiveness—achieving the overarching objectives of governmental activities—while neglecting economy and efficiency would be insufficient. If a program achieves its goals without considering the costs incurred, it may meet its intended outcomes, but at the expense of excessive and unsustainable resource consumption. Therefore, balancing all three principles is essential to maximising the benefits of performance auditing and ensuring sustainable public sector management.

In the State of Kuwait, the Performance Audit Department serves as a fundamental pillar in ensuring the efficiency and effectiveness of government institutions and the optimal utilisation of public resources. In this context, performance auditing undertakes several key functions to enhance accountability in the public sector, including:

1. Enhancing Government Performance Efficiency

- Reviewing operational and administrative processes to ensure that predetermined objectives are achieved efficiently and effectively.

- Analysing adherence to strategic plans and approved performance standards.

2. Promoting Accountability and Transparency

- Ensuring the implementation of sound governance principles within public institutions.

- Reviewing performance reports and auditing government entities’ compliance with established policies and regulations.

3. Monitoring the Implementation of Sustainable Development Goals (SDGs)

- Assessing the performance of government entities in achieving the 2035 Sustainable Development Goals.

- Proposing developmental mechanisms that contribute to financial and administrative sustainability in the public sector.

4. Supporting Decision-Making and Strengthening Strategic Planning

- Providing recommendations based on performance analysis reports to enable administrative leadership to make informed decisions.

- Aligning institutional performance with global indicators to ensure adherence to best international practices.

Recommendations:

1. Enhancing the Role of Performance Auditing in Public Sector Accountability

- It is recommended to closely monitor the implementation of programs adopted by performance auditing, as they play a crucial role in ensuring the optimal utilisation of public funds based on its core principles: economy, efficiency, and effectiveness.

2. Adopting a Comprehensive Auditing Approach

- Implementing an integrated oversight framework that combines financial auditing and performance auditing across all government entities under review. This holistic approach enables the state to keep pace with civilisational progress while also addressing political, economic, and social developments.

3. Developing Human and Institutional Capacities

- Proposing training programs and development plans to enhance employee competencies and improve overall performance.

- Updating guidelines and auditing procedures to facilitate the adoption of best practices in auditing and evaluation.

References:

- State Audit Bureau. (2005). Performance Audit Guide. Kuwait.

-Performance Audit Standard (ISSAI 3000). (https://www.issai.org/wp-content/uploads/2019/08/ISSAI-3000-Performance-Audit-Standard.pdf)

-Fundamental Principles of Performance Auditing. (ISSAI 300). (http://ar.issai.org).

- Gulf Cooperation Council (GCC) -General Secretariat. (2012). Performance Audit Guide for Audit and Financial Control Bureaus in GCC Countries (Joint Guides Series No. 3).

-State Audit Bureau. (2019). Guide to Key Operations- Second Edition: Performance Audit Tasks. Kuwait.