Jahandar Gadirov / Leading consultant,

The Chamber of Accounts of the Republic of Azerbaijan

Asian Journal of Government Audit

Jahandar Gadirov / Leading consultant,

The Chamber of Accounts of the Republic of Azerbaijan

Public sector accountability is a fundamental principle of good governance, ensuring that government entities operate transparently, efficiently, and in the best interest of citizens. In an era where transparency, efficiency, and accountability are paramount in governance, performance auditing has emerged as a critical tool for ensuring that public sector entities deliver value for money and achieve their intended objectives. Performance auditing plays a crucial role in enhancing accountability by assessing the effectiveness, efficiency, and economy of public sector activities. Unlike financial audits, which focus on compliance and accuracy of financial statements, performance audits provide insights into whether public resources are managed optimally to achieve intended policy outcomes. This article explores the role of performance auditing in enhancing public sector accountability and its impact on good governance.

Understanding Performance Auditing is an independent and objective evaluation of government programs, projects, and operations to determine their effectiveness and efficiency. It is conducted by Supreme Audit Institutions (SAIs) and other oversight bodies to ensure that public funds are used responsibly and deliver maximum value. Key Objectives of Performance Auditing should be considered as

Accountability is one of the fundamental principles of democratic governance. Citizens have the right to know how their tax dollars are being spent and whether public institutions are fulfilling their commitments. In this context, performance auditing plays a crucial role in ensuring accountability and enhancing the efficiency of public administration.

Firstly, performance audits increase the transparency of government institutions. These audits shed light on the operations of public agencies and enable the dissemination of relevant information to the general public. As a result, by publishing audit reports, governments demonstrate their commitment to open governance and strengthen public trust in state institutions.

Secondly, performance audits often reveal inefficiencies, management errors, and wasteful spending. Identifying such shortcomings in public programs allows policymakers to take timely corrective actions. This ensures that resources are used more efficiently and responsibly.

Thirdly, performance audits contribute to evidence-based decision-making. The data and recommendations obtained from audits provide policymakers with a solid foundation for designing and implementing more effective programs. This reduces the risk of policy failures and enhances the overall quality of governance.

Finally, regular performance audits help foster a culture of accountability within public institutions. When public officials are aware that their performance will be subject to scrutiny, they are more likely to act responsibly, adhere to best management practices, and comply with ethical standards.

Thus, performance auditing not only ensures the proper utilization of financial resources but also improves governance quality while reinforcing public confidence in state institutions.

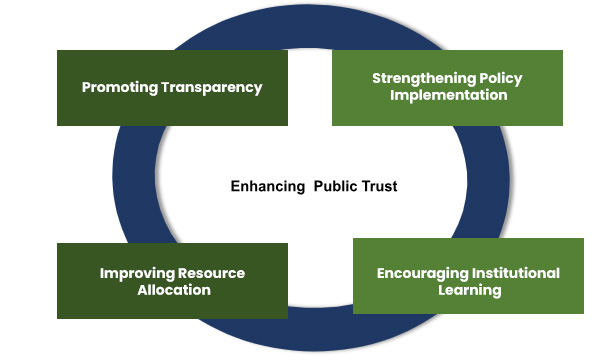

Figure 1. Enhancing Accountability through Performance Auditing

1. Promoting Transparency:

2. Improving Resource Allocation:

3. Strengthening Policy Implementation:

4. Enhancing Public Trust:

5. Encouraging Institutional Learning:

Performance auditing is a key mechanism for ensuring transparency, efficiency, and effectiveness in public sector management. Supreme Audit Institutions (SAIs) worldwide have successfully conducted performance audits that have led to policy improvements, cost savings, and enhanced accountability.

As a crucial oversight tool, performance auditing enables SAIs to evaluate the efficiency, effectiveness, and economy of public sector programs. By identifying inefficiencies, uncovering mismanagement, and ensuring that public funds are used appropriately, these audits strengthen public sector accountability and governance.

In the following tables, we explore real-world examples from various SAIs, demonstrating how performance audits contribute to improved policies, financial savings, and stronger institutional frameworks.

Case Studies: Performance Auditing in Action

#1 UK National Audit Office (NAO) – Evaluating COVID-19 Spending

During the COVID-19 pandemic, the UK government allocated billions of pounds for emergency response programs, including personal protective equipment (PPE) procurement and business support schemes. The National Audit Office (NAO) identified significant irregularities in procurement processes, highlighting a lack of transparency in contract awards, which led to excessive costs. Many contracts were awarded without proper competition, increasing the risks of inefficiency and favouritism.