Rawan Hadi Alhajri,

Associate auditor,State Audit of Bureau of Kuwait

Asian Journal of Government Audit

Rawan Hadi Alhajri,

Associate auditor,State Audit of Bureau of Kuwait

Accountability in the public sector is essential for how well a democracy works and how wisely public money is handled. Governments are trusted with power and public resources to deliver services, implement policies and support national development. Because of this responsibility, having strong oversight systems to make sure they're accountable is key to ensure that public funds are used legally, efficiently, and in alignment with intended policy outcomes.

Supreme Audit Institutions (SAIs) play a central role in ensuring this accountability is maintained. According to the principles established by the International Organization of Supreme Audit Institutions (INTOSAI), public sector auditing must be independent, objective, and transparent (INTOSAI, 2019). The Fundamental Principles of Public-Sector Auditing (ISSAI 100) state that auditing should not only check compliance but also help improve public sector performance.

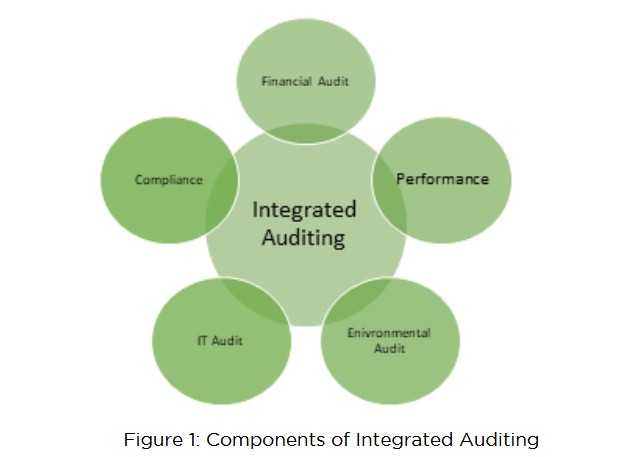

However, the way governments work is more complex than before. Public institutions manage digital service platforms, cybersecurity systems, large procurement processes, and even climate-related investments. These areas are connected and often involve financial, operational, and technological risks at the same time. For this reason, traditional audits that focus only on financial statements are no longer enough, a more comprehensive and integrated approach to auditing is now necessary.

Accountability in Modern Public Governance

Public accountability may be conceptualized through three main aspects:

While traditional audits often assess these areas separately, in practice these area are not isolated. Financial problems may result from weak internal controls, poor IT systems, or ineffective program design. At the same time, weak performance results may be linked to procurement problems or risk management failures. An integrated audit approach recognizes these connections and examines them together instead of separately.

Integrated auditing combines multiple audit disciplines such as financial, compliance, performance, IT, and environmental auditing within a coordinated framework. Instead of conducting separate examinations, auditors apply a structured methodology that connects financial data, operational performance, risk management, and policy outcomes.

Integrated auditing therefore reflects an important shift in public sector oversight. Rather than serving solely as a retrospective control mechanism, auditing increasingly contributes to proactive governance assurance.

Digital Governance and IT Oversight

INTOSAI guidance highlights the importance of integrating IT audit within broader audit frameworks (INTOSAI, 2022). Reviews of digital governance systems in several Asian jurisdictions revealed that financial irregularities were often accompanied by cybersecurity vulnerabilities and weak data controls. By combining IT, compliance, and performance assessments, SAIs strengthened encryption standards, improved system monitoring, and enhanced service reliability. Accountability in the digital era thus extends beyond financial accuracy to include information security and technological resilience.

Performance and Sustainability Auditing in Europe

The European Court of Auditors has increasingly emphasized outcome-oriented and sustainability-focused audits (European Court of Auditors, 2022). This illustrates how audit institutions are broadening their scope to assess public value, environmental impact, and strategic effectiveness and long-term sustainability of government actions rather than focusing only on financial compliance.

Environmental Oversight in Infrastructure Projects

The Asian Development Bank highlights the importance of environmental audits in ensuring compliance with sustainability commitments in infrastructure projects (Asian Development Bank, 2020). Integrated environmental audits have strengthened oversight of contractors and improved environmental impact assessments, helping align public investments with climate and sustainable development objectives.

Capacity Development within ASOSAI

Within the Asian region, the Asian Organization of Supreme Audit Institutions has promoted peer reviews, joint audits, regional workshops, and digital training programs to enhance integrated audit capacity (ASOSAI, 2023). These initiatives encourage knowledge sharing, methodological consistency, and institutional development among member SAIs.

Public Procurement and Service Delivery Reform

Performance audits of healthcare procurement systems, supported by the World Bank, demonstrated how integrated approaches can reduce inefficiencies and improve service delivery (World Bank, 2021). Linking financial data to operational performance enabled cost reductions and improved service quality, illustrating the practical benefits of integrated auditing for citizens.

Innovative Methodologies Supporting Integration

Modern audit practices support integration through:

Collectively, these methodologies demonstrate that auditing is evolving into a forward-looking function that supports effective governance and long-term institutional stability.

Impact on Public Sector Accountability

Integrated auditing strengthens accountability by:

Thus, auditing should not be viewed solely as a technical exercise. It is a democratic safeguard that ensures governments remain answerable to citizens and responsive to the public interest.

The increasing complexity of public administration requires a corresponding evolution in auditing practices. Traditional financial oversight remains essential, but it is no longer sufficient on its own. Comprehensive and integrated auditing provides a structured framework capable of evaluating legality, efficiency, technological integrity, and environmental sustainability within a unified system.

For ASOSAI member SAIs, adopting integrated methodologies represents both a strategic necessity and a valuable opportunity. By aligning with INTOSAI standards and embracing innovation, SAIs can strengthen governance systems, enhance accountability, and sustain public confidence. Integrated auditing is therefore not merely a methodological development; it is a critical instrument for promoting democratic legitimacy and sustainable development.