Mr. Leonardo Tarigan & Mr. Whidas Prihantoro

SAI Indonesia

Asian Journal of Government Audit

Mr. Leonardo Tarigan & Mr. Whidas Prihantoro

SAI Indonesia

Procurement governance in Indonesia’s upstream oil and gas sector plays a pivotal role in ensuring cost efficiency, regulatory compliance, and national energy resilience. This research assesses the implementation of SKK Migas Procurement Guidelines within Indonesia’s upstream oil and gas sector, focusing on moral hazard risks, cost recovery, and production efficiency. Using qualitative analysis of SAI of Indonesia audit reports and relevant literature, the research identifies discrepancies between regulatory frameworks and field practices. Key findings highlight issues in scope of work modifications, pricing inefficiencies, and conflicts of interest among providers, all contributing to inflated operational costs and compromised procurement integrity. Despite PTK-007’s comprehensive structure, its practical application reveals vulnerabilities that may hinder national energy objectives. The study recommends revising procurement regulations, enhancing transparency, and adopting digital technologies to strengthen governance and accountability. These measures are essential to optimize cost recovery, safeguard state interests, and promote sustainable upstream operations.

Keywords: Upstream Oil and Gas, Procurement, Moral Hazard, Operational Cost

Under Presidential Regulation of the Republic of Indonesia No. 9 of 2013, as amended by Regulation No. 36 of 2018, Indonesian governmentmandates the Special Task Force for Upstream Oil andGas Business Activities (SKK Migas) to oversee upstream oil and gas operations through Cooperation Contracts. This mandate ensures that national oil and gas resources are utilized strategically and efficiently for the benefit of the country and its people. SKK Migas operates under the supervision of the Minister of Energy and Mineral Resources and is empowered to regulate, monitor, and assess the activities of Oil and Gas Contractors (KKKS), including their procurement procedures (Ministry of Energy and Mineral Resources, 2022).

International best practices highlight that digital integration across supply chains enhances efficiency, resilience, and project delivery in upstream oil and gas operation. This is achieved through improved planning, proactive risk mitigation, and stronger stakeholder collaboration (Onukwulu et al., 2024a). A strategic approach is vital, emphasizing robust policies and thorough supplier assessments to reduce risks, ensure compliance, and maintain sustainable operations (Onukwulu et al., 2024b). As technology evolves rapidly, continuous evaluation of procurement systems is necessary to improve supply chain maturity and preserve agility (Wang et al., 2025).

Effective and transparent supply chain management is essential for operational success and long-term investment in the upstream sector. SKK Migas’s Work Procedure Guidelines (PTK) No. 007 provide a comprehensive framework governing KKKS activities, including planning, procurement, asset and customs management, and project execution. These guidelines are founded on principles of efficiency, fairness, and transparency, aiming to strengthen domestic capabilities in oil and gas support services.

PTK-007 Book 2 specifically outlines the regulatory structure for supply chain management, ensuring that operational needs are met with optimal cost, quality, and timeliness. It also serves as a tool for promoting national economic growth. Recent revisions to PTK-007 reflect efforts to align with global standards. However, its implementation faces challenges such as moral hazards that inflate production costs, as noted in audits by Indonesia’s Supreme Audit Institution (BPK). This study evaluates PTK-007 Book 2’s effectiveness by examining scope amendments, pricing mechanisms, and supplier selection processes to identify gaps and recommend improvements in procurement governance.

This research conducts a qualitative document analysis of 16 BPK audit reports to understand the risks of moral hazard in upstream oil and gas procurement. The authors specifically sought out audit findings that detail issues with pricing, contract amendments, and potential conflicts of interest. This analysis, supplemented by a literature review of global journals, legislation, media, allows the research to examine how current procurement practices align with established governance frameworks.

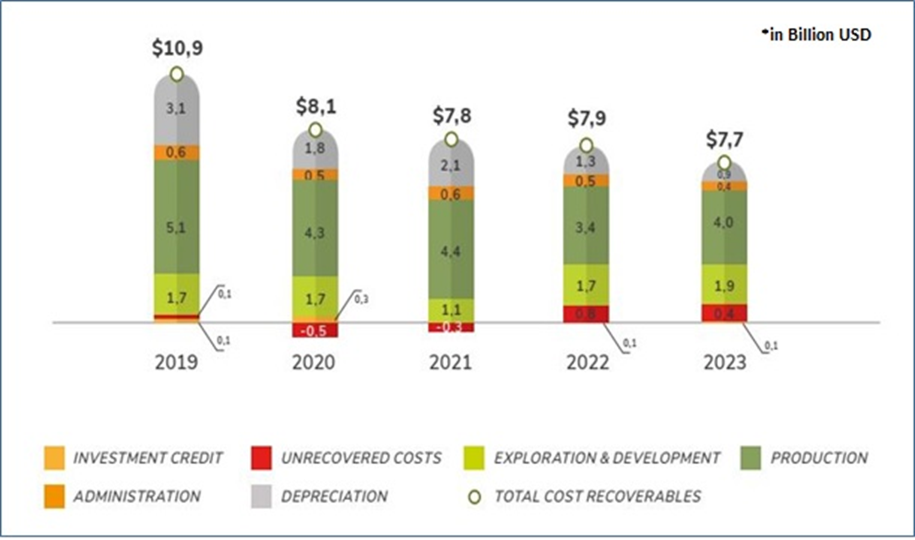

Due to its inherent risk, SKK Migas is required to strictly oversee cost recovery related to KKKS procurement activities. These expenditures directly affect cost recovery calculations and the revenue split between KKKS and the Indonesian government. Additionally, crude oil price volatility significantly influences procurement costs and inventory turnover, especially in Middle Eastern oil-dependent industries. Each unit increase in volatility may raise procurement costs by approximately $3.96 million, prompting firms to prolong inventory holding as a hedge, which impacts turnover rates (Mohammad et al., 2025). The 2023 SKK Migas Annual Report details cost recovery trends from 2019 to 2023.

Figure 1. Cost Recovery 2019 – 2023 (Source : SKK Migas, 2023)

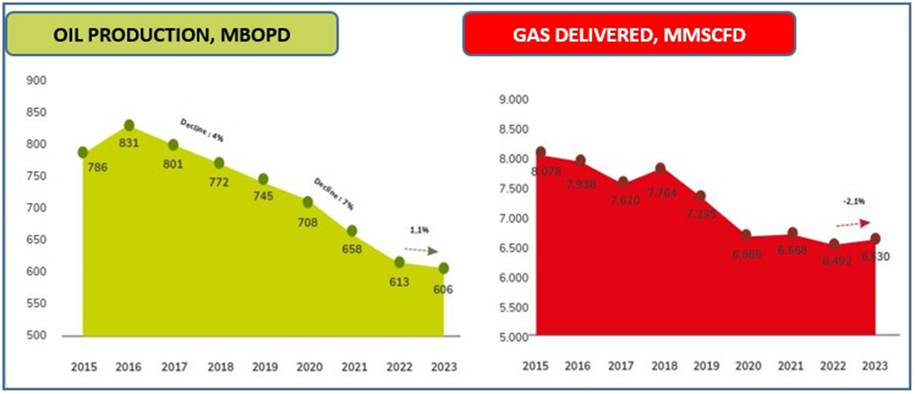

Figure 1 indicates a downward trend in cost recovery between 2019 and 2023. Notably, the depreciation burden in 2023 was relatively low, recorded at USD 0.9 billion. This reduction is likely due to the absence of substantial depreciation charges from major KKKS production facility projects. Furthermore, exploration, development, and production expenditures in 2023 exceeded those of 2021 and 2022. Additionally, the 2023 SKK Migas Annual Report presents oil and gas production data from 2015 to 2023.

Figure 2. Oil and Gas Production 2015 – 2023 (Source : SKK Migas, 2024)

Figure 2 illustrates a steady decline in petroleum production since 2016, reaching 606 million barrels per day by 2023. In contrast, natural gas production has shown volatility, with a substantial drop from 2018 to 2020. Analysis of Figures 1 and 2 highlights a downward trend in oil and gas production, despite the potential for increased cost recovery. This discrepancy may point to inefficiencies in cost recovery implementation or a weak linkage between cost recovery mechanisms and production performance. Accordingly, KKKS must establish robust procurement arrangements to ensure that goods and services expenditures contribute meaningfully to cost recovery outcomes. This finding aligns with research conducted in Nigeria, where asset procurement investments have not consistently translated into profitability gains (Twaliwi et al., 2022). To address these challenges, some studies recommend for adaptive procurement strategies, enhanced buyer-supplier collaboration, and the integration of digital platforms such as SAP Ariba to support data-driven decision-making and strengthen long-term supply chain competitiveness (Alhammadi et al., 2023; Adindu Donatus Ogbu et al., 2024).

Based on the analysis of the BPK audit reports and supporting literature reveals that moral hazard remains a key challenge in the procurement of goods and services within the upstream oil and gas sector, impacting both KKKS and their suppliers. This concern is exacerbated by structural limitations in the PTK-007 policy framework, particularly regarding the clarity and enforcement of procurement guidelines.

The Contract Management provisions in PTK-007 Book 2 outline procedures for modifying scope of work, including price changes and task additions. KKKSmay revise scope if the increase in contract value does not exceed 10% of the original amount. Exceptions apply to specific procurement categories such as drilling rigs, rework, well maintenance, and integrated construction projects with related services (SKK Migas, 2023).

BPK’s report found cases where KKKS altered scope without formal amendments from KKKS or providers. These undocumented changes included unit price revisions, extended timelines, and expanded scopes. To ensure transparency and accountability, all adjustments must be formally documented and contractually validated.

A recurring issue in KKKS procurement is scope amendment due to providers failing to meet original commitments. Timeline extensions - often granted without penalties - typically result from provider delays. In integrated construction, such deviations can cause major cost overruns, increasing the financial burden on the Government of Indonesia under the Production Sharing Contract (PSC). Scope expansions that raise costs are often linked to procedural errors by KKKS and providers. BPK also found cases where additional scope was justified under COVID-19 mitigation claims, raising red flags about the transparency and accountability of those modifications.

PTK-007 Book 2 generally prohibits scope expansions for obligations already assigned through contracts or tenders. Exceptions are allowed only for unforeseen, technically essential changes. However, this clause presents a moral hazard in change management, as the “unpredictability” argument may be misused to justify changes that should remain the responsibility of KKKS or providers.

PTK-007 Book 2 stipulates that goods and services procurement cannot be classified as operational expenditure if the owner's estimate fails to reflect a reasonable market value or if the contract price exceeds the owner's estimate (SKK Migas, 2023). BPK report have identified instances of cost mark-ups resulting from inaccurate cost assessments and the use of overly complex or inefficient estimation formulas, leading to inflated unit prices and reduced procurement efficiency. These practices pose fiscal risks to the Government and undermine the integrity of procurement management.

Additionally, contract pricing is vulnerable to moral hazard, particularly in the rental of operational assets where rental costs frequently surpass purchase prices. This is due to the absence of regulatory provisions in PTK-007 Book 2 requiring KKKS to compare owner estimates for both rental and purchase options prior to procurement. Although purchasing typically involves higher upfront costs and maintenance obligations, it enables asset ownership by the Government and offers potential residual value through resale. For example, in vehicle procurement, decommissioned units can be resold, generating returns that help offset total procurement expenditures.

PTK-007 Book 2 emphasizes the critical importance of avoiding conflicts of interest in the procurement of goods and services (SKK Migas, 2023). A conflict arises when KKKS personnel, acting individually or collectively, exert influence, whether directly or indirectly, to affect procurement decisions in favor of specific individuals, groups, affiliates, or providers. Such conduct undermines the integrity of the procurement process and exposes the Government and other legally bound parties to significant risk. BPK audit report have highlighted procurement irregularities involving provider companies with direct or indirect ties to the KKKS operators overseeing the procurement process. In several cases, KKKS granted leniency on late penalties despite providers failing to meet contractual deadlines. Moreover, affiliated providers often operated as intermediaries rather than asset owners, contributing to inflated rental costs. These affiliations extended beyond the immediate KKKS operator, involving other KKKS entities with participating interests. The relationships took various forms, including KKKS subsidiaries, foreign companies from the operator’s country of origin, and even familial connections between provider company owners and stakeholders in participating interests.

The interactions between providers and KKKS whether direct or indirect, can substantially influence procurement outcomes and decision-making processes. Providers with established ties to KKKS may gain early access to procurement details, including owner estimates, giving them a competitive edge during tender preparation. These relationships may also enable access to privileged information or shape the development of tailored technical specifications, potentially resulting in exclusive eligibility during technical evaluations. In some cases, such affiliations foster ongoing collaboration, leading to recurring procurement needs and the establishment of subscription based arrangements. While such practices can undermine the integrity and transparency of procurement, they also present opportunities for operational efficiency.

Despite the inherent risk of moral hazard, strategic relationships between KKKS and providers can yield cost-saving benefits. Subscription models, for instance, may reduce rental expenses, and long-term partnerships can result in preferential pricing. Furthermore, fostering synergy among state-owned enterprises (BUMNs) is essential, with BUMN entities ideally prioritized as suppliers in KKKS operations, particularly in cases where both the operator and the provider are BUMNs. Accordingly, PTK-007 Book 2 must embed robust safeguards to prevent moral hazard by ensuring that procurement remains cost-effective, accountable, and free from undue leniency in penalty enforcement.

Procurement plays a critical strategic role in the upstream oil and gas sector, serving as a cornerstone for operational efficiency and cost control. Although PTK-007 Book 2 provides a comprehensive regulatory framework, evaluations particularly those reflected in BPK audit findings highlight persistent gaps between policy and practice. Key vulnerabilities include inconsistencies in scope modification procedures, pricing methodologies, and vendor selection processes, which collectively expose KKKS to moral hazard. These shortcomings risk inflating operational expenditures, placing fiscal pressure on the Indonesian government and undermining the integrity of procurement governance.

To mitigate these risks, SKK Migas and KKKS must prioritize a thorough revision of PTK-007 Book 2, reinforcing regulatory provisions with stricter controls on scope changes, transparent and market-aligned pricing mechanisms, and robust safeguards against conflicts of interest. The integration of digital technologies should be actively advanced to improve efficiency, traceability, and accountability across the procurement lifecycle. Additionally, fostering strategic collaboration among BUMNs through the optimal engagement of BUMN vendors can enhance value creation, provided that transparency and fair competition remain central to procurement practices.

Adindu Donatus Ogbu, Williams Ozowe, & Augusta Heavens Ikevuje. (2024). Solving procurement inefficiencies: Innovative approaches to SAP Ariba implementation in oil and gas industry logistics. GSC Advanced Research and Reviews, 20(1), 176–187. https://doi.org/10.30574/gscarr.2024.20.1.0260

Alhammadi, A., Soar, J., Yusaf, T., Ali, B. M., & Kadirgama, K. (2023). Redefining procurement paradigms: A critical review of buyer-supplier dynamics in the global petroleum and natural gas industry. In Extractive Industries and Society (Vol. 16). Elsevier Ltd.https://doi.org/10.1016/j.exis.2023.101351

Mohammad,S. I. S., Al-Daoud, K. I., Al Oraini, B. S., Alqahtani, M. M., Vasudevan, A., & Ali, I. (2025). Impact of Crude Oil Price Volatility on Procurement and Inventory Strategies in the Middle East. International Journal of Energy Economics and Policy, 15(2), 715–727. https://doi.org/10.32479/ijeep.18950

Onukwulu, E. C., Dienagha, I. N., Digitemie, W. N., Egbumokei, P. I., & Oladipo, O. T. (2024a). Advanced supply chain coordination for efficient project execution in oil & gas projects. International Journal of Multidisciplinary Research and Growth Evaluation, 5(4), 1255–1272. https://doi.org/10.54660/.ijmrge.2024.5.4.1255-1272

Onukwulu, E. C., Dienagha, I. N., Digitemie, W. N., Egbumokei, P. I., & Oladipo, O. T. (2024b). Ensuring compliance and safety in global procurement operations in the energy industry. International Journal of Multidisciplinary Research and Growth Evaluation, 5(4), 1311–1326. https://doi.org/10.54660/.ijmrge.2024.5.4.1311-1326

Presidential Regulation of the Republic of Indonesia Number 9 of 2013. (2023). The Implementation of Management of Upstream Oil and Gas Business Activities.

Presidential Regulation of the Republic of Indonesia Number 36 of 2018. (2018). Amendments to Presidential Regulation Number 9 of 2013 on the Implementation of Management of Upstream Oil and Gas Business Activities.

Regulation of the Minister of Energy and Mineral Resources of the Republic of Indonesia Number 2 of 2022. (2022). The Organization and Work Procedures of SKK Migas.

SKK Migas. (2023). PTK-007 Book 2 SKK Migas Number PTK-007/SKKIA0000/2023/S9 (Revision 05) Second Book on Guidelines for the Implementation of Procurement of Goods and Services.

SKK Migas. (2024). Annual Report SKK Migas 2023

Twaliwi, Z. C., Aderinola, A. E., & Okon, E. U. (2022). Procurement Management and its Impact on the Performance of Oil and Gas Industry in Nigeria. INDO-ASIAN JOURNAL OF FINANCE AND ACCOUNTING, 3(2), 175–191. https://doi.org/10.47509/iajfa.2022.v03i02.09

Wang, X., Wei, W., Xie, S., Pu, J., Song, X., & Wang, L. (2025). Evaluation of Management Level of Procurement Service-oriented Supply Chain in Oil and Gas Enterprises Based on Analytic Hierarchy Process. Procedia Computer Science, 266, 667–674.https://doi.org/10.1016/j.procs.2025.08.084