Manish Kumar

Pr. Accountant General SAI India

Asian Journal of Government Audit

Manish Kumar

Pr. Accountant General SAI India

Public sector accountability refers to the obligation of government institutions, public officials, and state-funded bodies to explain and justify their decisions, actions, and use of public resources to stakeholders, including citizens, legislatures, audit institutions, and oversight bodies. Accountability ensures that public sectors are subjected to scrutiny, review, and corrective mechanisms.

In practical terms, accountability operates through systems of reporting, auditing, performance measurement, and legislative oversight. It links policy intent with outcomes and connects resource allocation with results. Instruments such as internal controls, performance audits, social audits, and parliamentary committees form the backbone of this system. An integrated cross-cutting audit approach strengthens accountability by examining how financial management, compliance, service delivery, and governance intersect across departments rather than in isolated silos.

Supreme Audit Institutions (SAIs) derive their authority from the Constitutional or Statutory provisions that empower them to audit government revenues and expenditures. The audit mandate ensures SAI’s independence, allowing it to examine whether public resources are used in accordance with laws, regulations, and legislative intent. By auditing government accounts and reporting their findings to the Parliament/Legislatures, SAIs act as a key pillar of democratic governance and financial oversight. Their reports enable elected representatives to scrutinize executive actions and hold public officials accountable for the management of public funds.

In India, the Comptroller and Auditor General of India (SAI India) is established under Articles 148–151 of the Constitution of India. As the governance in India is federal in nature, SAI assumes the role of the federal auditor auditing the accounts of the Union (Central) and State (Provincial) governments, its parastatals and local bodies. Through financial, compliance, and performance audits, the SAI India provides objective assurance on whether public expenditure is legal, economic, efficient, and aligned with policy goals. The constitutional mandate ensures that the audit function remains independent from executive influence.

SAIs contribute to improving governance and public service delivery by focusing on outputs and outcomes in performance audit. They identify systemic weaknesses, inefficiencies, and policy implementation gaps that may hinder programme success. This approach encourages governments to shift from input-based administration toward results-based management.

Transparency and accountability are essential for maintaining public trust in government institutions. When audit findings are publicly reported and debated in legislative forums, citizens gain confidence that public resources are subject to independent scrutiny.

Public sector schemes are implemented through a structured institutional framework that connects policy formulation with on-ground execution. Typically, schemes originate at the Central or Provincial government level where policy objectives, guidelines, funding patterns, and implementation mechanisms are defined. Ministries or departments design the scheme, allocate budgetary resources, and issue operational guidelines that outline eligibility criteria, monitoring mechanisms, and reporting requirements. These guidelines form the administrative blueprint for implementation and ensure uniformity across implementing agencies.

Once the policy framework is established, implementation responsibilities are distributed across multiple government bodies, public agencies, and sometimes private or non-governmental partners. Financial flows are routed through treasury systems, dedicated funds, or centrally sponsored schemes where both Central and State governments share responsibilities.

For instance, the Pradhan Mantri Awaas Yojana–Gramin (PMAY-G) housing scheme is implemented through coordination between the Union government and state administrations, demonstrating how multiple levels of governance collaborate to deliver public services.

Public sector programmes in India typically operate across multiple levels of governance, creating a vertical hierarchy that connects national, state, district, and local administrations. In this vertical structure, responsibilities are distributed along the administrative chain. Central ministries may design and fund the scheme, state departments adapt the implementation strategy to local contexts, district authorities coordinate execution, and local bodies or field offices deliver services directly to beneficiaries. This layered structure ensures wider outreach but also introduces complexities in coordination, monitoring, and accountability.

In addition to vertical linkages, public programmes also function through horizontal coordination among departments and agencies operating at the same administrative level. Many development schemes—such as those related to infrastructure, MSME development, or social welfare—require collaboration among departments dealing with finance, industry, land, environment, and local governance. Such horizontal coordination helps integrate resources and expertise but also creates risks of duplication, gaps in responsibility, or delays if coordination mechanisms are weak. For auditors and policymakers, understanding both vertical and horizontal linkages is essential to evaluate programme performance and identify systemic issues that may affect implementation outcomes.

Para 3.8 of Performance Audit guidelines provide for selection of subjects which cuts across various departments or entities. They provide a platform for performance audit on a theme or thrust area over a cross section of entities, who are entrusted with the responsibility for the programme and activity.

Traditional audit approach (Compliance and Financial Audits) and oversight mechanisms often focus on individual departments, agencies, or financial transactions. Although these approaches are essential for maintaining fiscal discipline and legality, they may not fully capture how complex government programs actually function. Many government schemes today involve multiple ministries, implementing agencies, and layers of administration, making it difficult to assess the overall effectiveness of a program when each entity is audited in isolation.

As a result, traditional oversight may overlook systemic issues such as coordination failures, duplication of efforts, delays in service delivery, or gaps between policy intent and implementation outcomes. This limitation highlights the need for a more integrated audit approach that evaluates the entire program ecosystem rather than isolated institutional components.

An integrated cross-cutting audit is an approach that evaluates a public sector program holistically by examining all institutions, processes, and stakeholders involved in achieving its objectives. Instead of focusing solely on individual organizations, the audit places the program or policy initiative at the center of analysis. The audit then traces how different departments, agencies, and implementation mechanisms contribute to the program’s design, funding, execution, and monitoring.

Integrated audits also allow for a more comprehensive assessment of whether government interventions are producing intended results. In doing so, they complement traditional financial and compliance audits by adding a strategic perspective on governance and program performance.

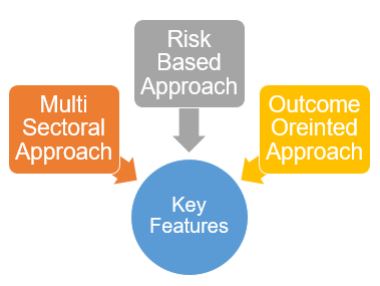

Integrated audits recognize that many public programs operate across multiple sectors. A single scheme may involve collaboration among departments responsible for finance, infrastructure, technology, environmental regulation, and social development. Therefore, the audit examines interactions among these sectors rather than reviewing them independently.

Integrated audits use risk-based methodologies to focus on areas with the greatest potential impact on program success. Instead of examining all components equally, auditors identify critical risk points such as financial flows, procurement systems, inter-agency coordination, and beneficiary targeting.

Unlike traditional audits that emphasize procedural compliance, integrated audits focus on outcomes and impact. They evaluate whether programs achieve policy objectives and deliver measurable benefits to citizens.

They examine whether public resources are used economically across the entire program framework, helping identify wasteful expenditure and improving budget planning.

By analyzing administrative processes across departments, integrated audits detect bottlenecks, redundancies, and coordination failures.

They evaluate whether programs achieve intended objectives and deliver services to beneficiaries in a timely and equitable manner.

Integrated audits verify adherence to statutory provisions, financial rules, procurement guidelines, and policy directives across all government agencies.

Comprehensive program analysis enhances transparency by providing stakeholders with a clear understanding of how public resources are used.

By mapping the decision-making and implementation across administrative levels, integrated audits help identify responsible entities and strengthen accountability.

Government programs are often administered by multiple departments operating within their own mandates. Institutional silos can hinder access to information and complicate program evaluation.

Establishing cross-sector audit teams and adopting program-based audit planning can help overcome these challenges.

Integrated audits require large volumes of data from multiple sources. Differences in information systems and lack of interoperability can limit data availability.

Developing standardized data formats, integrated reporting systems, and advanced analytical tools can address these challenges.

Auditors conducting integrated audits require multidisciplinary skills, including policy analysis, program evaluation, and sector-specific knowledge.

Regular training programs, interdisciplinary collaboration, and involvement of subject-matter experts can strengthen audit capacity.

Since integrated audits involve multiple stakeholders, effective coordination mechanisms are essential. Establishing communication channels, standardized reporting templates, and collaborative platforms can improve coordination between auditors and implementing agencies.

Institutionalizing integrated audits requires supportive policies, standardized methodologies, and strategic planning within audit institutions. Integrating program-based auditing into long-term audit frameworks can ensure sustainability.

SAI India has applied integrated audit approaches in several major audits involving multiple ministries, state governments, and public sector entities. These include:

These audits involved coordination among multiple audit offices at the Union and State levels and examined complex programs involving numerous government agencies. The integrated approach enabled auditors to evaluate program performance across institutional boundaries.

In the audit cycle of 2026-27, SAI India has under two audit subjects involving integrated audit approach. These include:

Integrated cross-cutting audits represent an important evolution in public sector oversight by shifting the focus from isolated institutional reviews to comprehensive evaluation of entire government programs. This approach enables auditors to examine financial management, operational efficiency, compliance, and service delivery outcomes within a single analytical framework. By capturing inter-departmental linkages horizontally as well as vertically and systemic risks, integrated audits help identify coordination gaps and policy implementation challenges that traditional audits may overlook. They therefore, strengthen transparency, improve accountability across multiple levels of governance, and support evidence-based decision-making.