Tamerlan Yusif-zada

Chief of Staff of the Chamber of Accounts of the Republic of Azerbaijan

Asian Journal of Government Audit

Tamerlan Yusif-zada

Chief of Staff of the Chamber of Accounts of the Republic of Azerbaijan

Narmin Jafarova

Advisor of the Chamber of Accounts of the Republic of Azerbaijan

Over the past 20–25 years, strategic management has been widely accepted as one of the methods for modernizing public policy. The success of steps taken by public institutions to align their operations with high standards and to respond appropriately to ongoing changes is closely related to how correctly strategic management is implemented.

Strategic management is defined as the art of formulating, implementing, and evaluating functional decisions that enable an organization to achieve its objectives. Although there are various definitions of strategic management, the following definitions are among the most understandable and widely accepted:

Strategic management is the process of defining an organization’s goals by considering both internal and external environments, and making decisions to achieve those goals.

Strategic management is a continuous process of strategic analysis, strategy creation, implementation, and monitoring aimed at achieving competitive advantage.

The main objective of implementing strategic management in the public sector is to achieve better results in public services. In other words, the core goal in this sector is to create added value for citizens and society by improving the quality of public services, enhancing public welfare, and strengthening accountability and transparency

Different sources classify the strategic management process in various ways. However, the most common classification groups this process into three main stages:

1. Strategy Formulation - This is the core part of the strategic management process, and it characterizes the consolidation of actions aimed at the development of the institution into a realistic and ambitious plan.

The strategic plan is based on assessing the institution’s key operational needs and identifying the gaps or areas that require improvement. It requires defining clear steps, roles, responsibilities, and timelines. The strategy formulation process includes evaluating the current situation (using tools like SWOT analysis, PESTLE analysis, etc.), stakeholder expectations, and defining vision, mission, values, strategic issues, and priorities. Good strategic planning:

During strategy formulation, four main questions must be answered:

2. Strategy Implementation This stage involves carrying out the process, taking into account the organization’s structure and resources. It is important to develop an operational plan that aligns well with the strategy and considers financial and human resources. Each operational plan serves as a tool to translate strategic intent into actionable steps. At this stage, risk management must also be carefully addressed.

3. Monitoring and Accountability of Strategy Implementation This is the next stage, involving periodic assessment of the effectiveness of actions and planning for the future based on lessons learned. It is very important to monitor the implementation of strategic and operational plans through monitoring frameworks, which should include indicators, baseline and target values. The framework should cover both quantitative and qualitative aspects in Strategic Management.

Six Fundamental Principles ensure that an organization can design and implement an effective strategic management process while staying true to its mandate and mission at every stage:

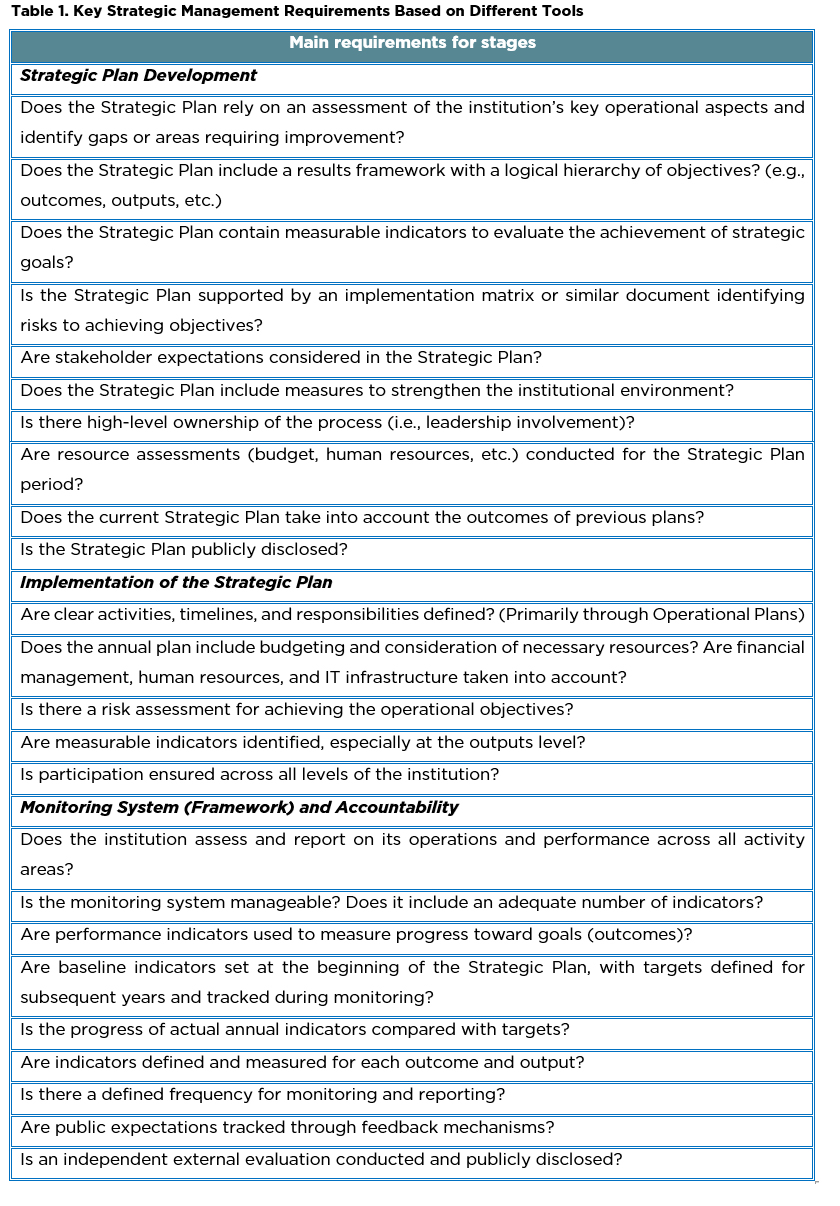

Various assessment tools (such as PEFA, SAI PMF, Public Sector Scorecards, etc.) define requirements for the strategic management framework. These requirements, when consolidated, lead to the conclusion that effective strategic management at the institutional level must take the following into account across different stages (Table 1).

The Strategic Plan of the Chamber of Accounts for 2021–2025, which outlines the Chamber's long-term development, reflects its vision, mission, core values, outcomes and outputs, and relevant activities. It was developed based on international expert evaluations and recommendations, progressive practices, the “Strategic Management Handbook for Supreme Audit Institutions,” and the principles of INTOSAI P-12 (The Value and Benefits of SAIs – Making a Difference to the Lives of Citizens). The Strategic Plan serves as a roadmap for the Chamber of Accounts’ operations from 2021 to 2025. It aims to strengthen institutional capacity and enhance the role of high-quality auditing in public financial management and oversight, through greater engagement with the parliament, government, and society.

The Strategic Plan Preparation Process, including the tools applied and the key steps taken, along with their characteristics, was reflected in the article “The Role of Strategic Development Plans in Strengthening the Activities of Supreme Audit Institutions. The Strategic Plan of the Chamber of Accounts for 2021–2025” published in Issue No. 1 (2021) of the official quarterly bulletin “State Audit”. This article, however, focuses on the next stages of strategic management, particularly on monitoring.

The Strategic Plan is characterized as a somewhat conceptual document. Its implementation mechanism is ensured through an Operational Plan.

To implement the Strategic Plan of the Chamber of Accounts for 2021–2025, an annual Operational Plan was developed, covering all outcomes and outputs. This plan includes measures aimed at addressing weak points and potential gaps across different areas of activity, and improving performance in various dimensions — institutional, organizational, and professional.

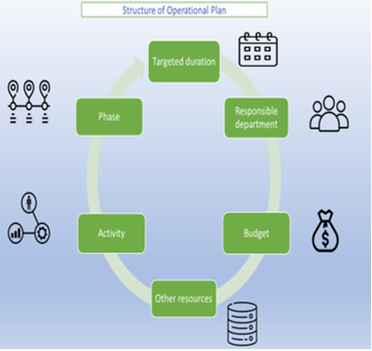

The structure of Operational Plans may consist of various elements. While the addition or removal of elements depends on the discretion of the institution applying strategic management, the core components are reflected as follows.

At the heart of the Operational Plan lie the "activities". The most important requirement for this element is its capacity to contribute to the achievement of the goals set out in the Strategic Plan. Analyses show that one of the main shortcomings in many institutions' strategic plans is the inclusion of predominantly routine (day-to-day) activities.

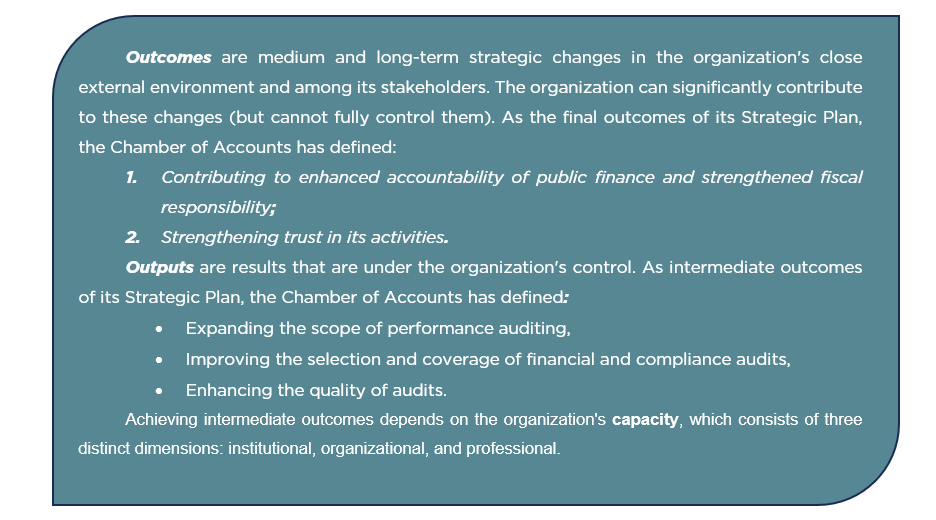

It should be noted that monitoring and accountability are sometimes treated as components of the overall strategy implementation process. Establishing a monitoring framework for outcomes and outputs during the preparation of the strategy allows for the methods of measuring outcomes to be defined in advance, and helps to specify the outcomes more precisely.

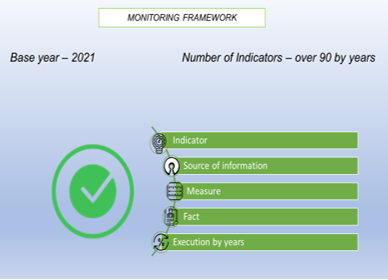

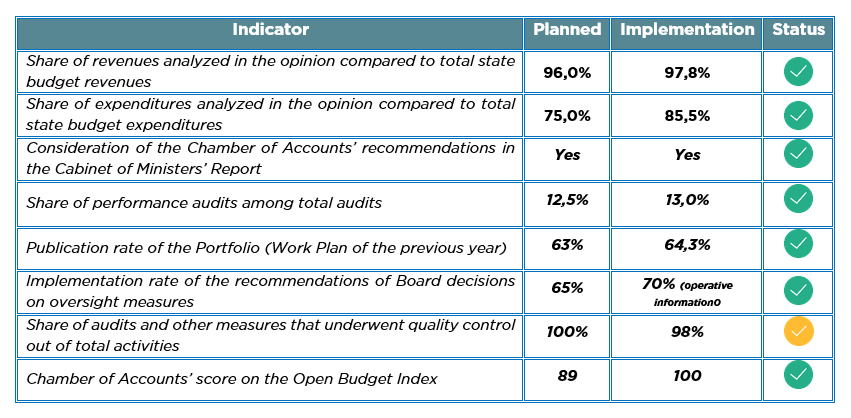

At the Chamber of Accounts, a system of indicators has been developed to monitor the implementation of the Strategic Plan. This system includes over 90 key performance indicators (KPIs). It sets the frequency of assessments and defines quantitative and qualitative targets to be achieved.

To ensure that the implementation of the planned activities is measurable, at the end of each year, actual implementation is assessed by comparing it against the planned indicators.

A dedicated section on the implementation of the Strategic Plan was included in the Annual Activity Reports of the Chamber of Accounts for 2021–2024, marking the first such practice in the country. In addition, for the first time in Azerbaijan, the reporting on the implementation of the Strategic Plan was also linked to budget indicators.

As seen in Table 2, the implementation of activities exceeded the level of budget execution.

Table 2 . Execution of the Operational Plan and the budget of Strategic Plan,%

Furthermore, the overall implementation status of the indicators within the Monitoring Framework remained at or above 80% during these years, which, being higher than the corresponding budget execution level, serves as an additional indicator of the effective implementation of the Strategic Plan.

The reporting practice of the Chamber of Accounts on its Strategic Plan has been recognized by international organizations (e.g., IDI) as one of the best in the field, and was recommended to other Supreme Audit Institutions (SAIs). The Chamber of Accounts has even been involved as an expert in projects aimed at establishing similar processes in the SAIs of other countries.

Table 3. Extract from the 2024 Implementation Status of the Strategic Plan Monitoring Framework

As previously mentioned, this article focuses more on the next stages of strategic management, particularly on monitoring. In this regard, the identification of appropriate indicators for measuring progress toward objectives becomes especially important. The article also highlights the significance of key performance indicators (KPIs) in various activities and emphasizes the importance of tracking implementation status using these indicators. The goal is to support public institutions in implementing this process and to contribute to the improvement of the indicator systems in use.

The Chamber of Accounts applies outcome indicators to measure the impact of its work by utilizing strategic management principles in both its core function — public auditing — and other activities.

However, it should be noted that some indicators are not included in the Strategic Plan's Monitoring Framework, either because the Chamber of Accounts does not have direct control over the collection of relevant data or because such indicators cannot be planned in advance. For example: Recommendations with financial impact — such as recovery of public funds, cost savings, prevention of overspending, or increased public revenues; Recommendations with procedural or compliance effects (i.e., those without direct financial effect) — such as improved legal compliance or the adoption of new regulatory documents. Although these are among the main indicators of audit activity, they are not part of the Monitoring Framework of the Strategic Plan. Nevertheless, data on these indicators are included in the Annual Activity Reports.

Thus, it can be concluded that not all good indicators can be applied for monitoring the implementation of strategic documents.

As mentioned, one of the most important aspects regarding the Monitoring Framework is the correct identification of indicators. Failure to define appropriate indicators may result in significant progress going unnoticed, even when the implementation rate of the Strategic Plan appears high.

Indicators must be directly linked to capacity, outputs, and outcomes. They can be expressed in quantitative or qualitative terms. Quantitative indicators are relatively easy to measure. Qualitative indicators, on the other hand, tend to be more descriptive in nature and often require additional criteria for measurement. A successful practice is to combine both types of indicators in the Monitoring Framework.

It should also be noted that including too many indicators in the Monitoring Framework can negatively impact the monitoring process (i.e., the system must remain manageable). In this regard, it is considered optimal to define 2–3 indicators for each outcome, and 1–2 (sometimes 3–4) indicators for each outputs. Additionally, indicators related to capacity may also be included in the relevant framework.

The inclusion of a large number of indicators in the Monitoring Framework by the Chamber of Accounts is due to various reasons. Broadly, this reflects the first-time application of a results-based framework, with plans to optimize the number of indicators in future strategic documents. It also includes the use of indicators that can measure not only outcomes and outputs but also capacity, and considers the Chamber’s ability to collect relevant data within a short timeframe. For example, indicators such as: Number of audits, ratio of published audit reports to the total portfolio, number and implementation rate of recommendations issued, number of quality-controlled audit activities are all under the direct control of the institution.

At the same time, it is possible to classify indicators in the Monitoring Framework as "good" or "poor". The table below provides some examples in the context of training activities.

Table 4. Good and Poor Indicators (Using Training Activities as an Example)

This aligns with Ward (2024), which notes that the use of GenAI for fraud detection and prevention in construction faces several challenges, including data quality and availability. GenAI relies on large and diverse datasets to train and evaluate models, yet construction data are often scarce, incomplete, and/or inconsistent due to the heterogeneous nature of the industry. Moreover, construction data are frequently sensitive and confidential, and accessing or sharing such data may raise privacy and security concerns. Ward (2024) further highlights challenges related to model validity and reliability. GenAI models are often complex, making their outputs difficult to interpret and verify, which raises questions regarding the accuracy, reliability, and suitability of the models for fraud detection and prevention purposes. Finally, Ward (2024) emphasizes regulatory and ethical considerations. The deployment of GenAI can have legal and ethical implications, particularly when used to inform decisions affecting stakeholders’ rights and interests. Consequently, the application of GenAI for fraud detection and prevention in construction requires compliance with relevant laws and regulations.