Oktarika Ayoe Sandha, Wahyudi, & Chandra Puspita Kurniawati

SAI Indonesia

Asian Journal of Government Audit

Oktarika Ayoe Sandha, Wahyudi, & Chandra Puspita Kurniawati

SAI Indonesia

E-purchasing has become a cornerstone of procurement reform in Indonesia. Yet e-audit monitoring result has revealed potential anomalies that signal vulnerabilities to fraud, including repeated transactions with the same supplier, unusually rapid transaction times, accelerated first purchases of newly listed products, and significant price changes at the point of transaction. While anomalies do not constitute proof of fraud, they serve as critical early warning indicators that auditors must integrate into risk-based audit planning. Their presence calls for more targeted testing of internal controls and closer evaluation of how procurement entities respond to irregularities. Thus, strengthening collaboration between BPK and government internal auditors is essential to safeguard accountability and integrity in public procurement.

Keywords: anomaly; e-purchasing; fraud; public procurement

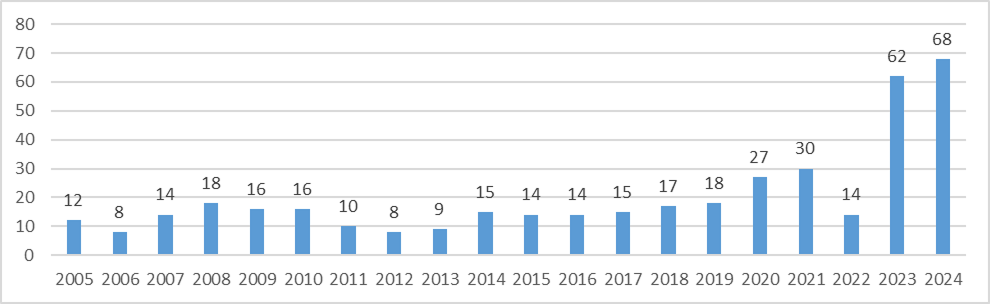

Governments worldwide are increasingly using public procurement as a strategic instrument to achieve policy objectives, making it a crucial pillar of public service delivery. On the contrary, because of the sheer volume of spending public procurement represents, corruption is especially prevalent in public procurement. This makes corruption in public procurement one of the most serious problems of modern public administration system (Chornyi et al., 2025). Consistent with this finding, Indonesian Corruption Eradication Commission showed hundreds of corruption cases in public procurement (see Figure 1 below) highlighting the ongoing challenges in ensuring transparency and accountability of public procurement.

Figure 1. Trends in corruption cases in government procurement (2005-2025) Source: (BPKP, 2025)

Moreover, many studies reveal that the complexity of public procurement process creates opportunities for fraud, especially whenthe process employs a manual system(Rachman& Alamsyah, 2023). This situation led to initiatives to transform public procurement into an electronic process to minimize interactions between parties and to eventually closing the gaps for corruption. Magakwe (2023) even believes that e-procurement is an important instrument for reducing the risk of fraud and corruption in private and government agencies.

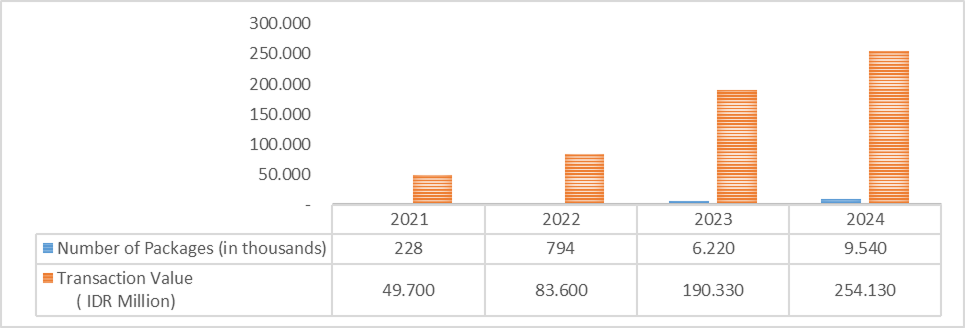

In Indonesian context, Government of Indonesia has issued some policies concerning public procurement as a basis for e-procurement system. Following up the issuance of Presidential Regulation 54/2010 on Public Procurement, Government of Indonesia had introduced e-purchasing method in 2015 allowing government entities to purchase directly from an electronic catalog (e-catalog). Further, presidential instruction has boosted the number of products listed in e-catalog leading to an increasing trend in e-purchasing (see Figure 2). The enactment of Presidential Regulation 46/2025 on Public Procurement, which mandates the use of e-purchasing for all public procurement when the goods/services are available in the e-catalog, further drives the adoption and growth of the trend in the future.

Figure 2. Profile of e-purchasing utilization (2021 – 2024) Source: Processed from LKPP Data, 2021 - 2024

Even though various studies have revealed the success of e-purchasing to prevent fraud in public procurement in Indonesia, Indonesia Corruption Watch has highlighted several potential fraud within the e-purchasing system (Rachman & Alamsyah, 2023). Accordingly, to effectively anticipate potential fraud risks in e-purchasing, the detection of anomalies in public procurements is critical (Niessen et al., 2020).

Considering the aforementioned condition, this study aims to provide information about potential anomalies in Indonesian e-purchasing system. Thus, this study is significant since it offers auditors a deeper understanding of the potential procurement anomalies. Consequently, auditors can develop more focused and effective audit programs to examine how the audited entities design and implement internal controls to respond these issues, helping to promote transparent and accountable e-purchasing process.

This study employs a series of Focus Group Discussions (FGDs) with public procurement policymaker, government internal oversight officials, as well as BPK officials including public procurement officials, IT officials, and BPK auditors, as outlined below.

| No. | Topics | Profile of Resources | Time Schedule | Key Questions |

|---|---|---|---|---|

| 1. | The investigation of e-purchasing cases and the utilization of big data analytics to reveal fraud in e-purchasing system | The investigative unit and IT Bureau of the Audit Board of the Republic of Indonesia (Badan Pemeriksa Keuangan – BPK) | January 2025 |

– E-purchasing audit and tools utilized – Detected anomalies |

| 2. | Policy implementation and evaluation on the utilization of e-catalog 5.0 and 6.0 |

– National Public Procurement Agency (Lembaga Kebijakan Pengadaan Barang/Jasa Pemerintah – LKPP) – Financial and Development Supervisory Board (Badan Pengawasan Keuangan dan Pembangunan – BPKP) – Public procurement official – BPK |

January 2025 |

– Relevant government policies – Challenges in the utilization of e-catalog 5.0 and 6.0 – Detected anomalies |

At the initial stage of the FGD process, a proposal and a set of key questions were developed to serve as guiding instruments for the discussion. These documents were subsequently distributed to the resource persons to facilitate their preparation and ensure focused deliberation. During the discussions, participants’ responses were systematically documented. Following the FGDs, a thorough literature review was conducted by analyzing recent studies and key regulatory documents on the relevant subject. Lastly, the most relevant keywords related to potential anomalies in e-purchasing, identified through FGDs and literature reviews, were analyzed to determine the key categories of anomalies that warrant particular attention from auditors in e-purchasing audits.

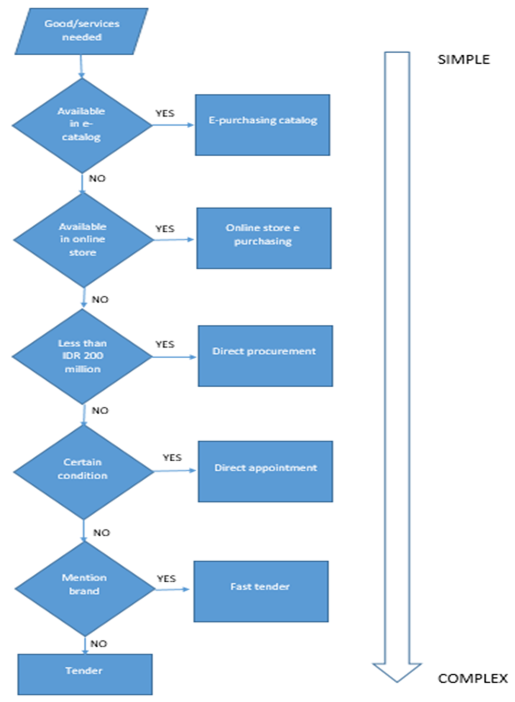

Public procurement covers the entire process - from the identification of needs to the final handover of completed work - conducted by ministries, agencies, local government, other public institutions, or village governments, and financed through the State/Local/Village Budget. In accordance with prevailing regulations, the selection of goods/services through suppliers can be conducted using several methods, including e-purchasing via e-catalog, online store e-purchasing, direct procurement, direct appointment, fast tender, and tender as illustrated in Figure 3.

Figure 3. The Selection of Goods/Services through Suppliers Source: Proceeded from Available Regulation

Under Presidential Regulation 46/2025, the government is required to use e-purchasing when the required goods/services are available in the e-catalog. If the goods/services are not listed in the e-catalog but can be accessed through online stores, the online store e-purchasing method should be applied. In other cases, several alternative procurement mechanisms are available. Direct procurement is permitted when the value of goods/services does not exceed IDR200million. Direct appointment may be used under specific conditions as specified in the regulation. Furthermore, a fast tender can be applied when suppliers are pre-qualified in the supplier performance information system and the project’s specifications and volume are clearly defined, or when a specific brand is required. Finally, a standard tender process is usedwhen the other procurement methods are not applicable. Among these options, e-purchasing is generally considered the simplest method due to its streamlined procedures and minimal administrative requirements. In contrast, the tender process remains the most complex, involving multiple stages and detailed evaluation criteria.

E-purchasing refers to the process of acquiring goods/services through an e-catalog system. The e-catalog itself is a digital platform that provides information on goods/services, including their prices, suppliers or self-managed implementers, and other relevant data. Initially, Article 72 of Presidential Regulation 16/2018 stipulated that the selection of commodities to be listed in the e-catalog was conducted by government agencies/LKPP, and the inclusion of goods/services in the e-catalog must undergo a series of verification process by the LKPP team. However, the issuance of Presidential Regulation 12/2021 devolved LKPP’s authority for selecting commodities to be listed in the e-catalog to the buyers. According to Rachman & Alamsyah (2023), this amendment introduced a new burden and shared responsibility for buyers in managing procurement decisions.

In addition, this amendment eliminated the tender and negotiation process prior to commodity listing. Consequently, price negotiation is no longer applied at the listing stage, and the prices published in the e-catalog now represent themaximum retail price rather than the best-negotiated price. Under this regulation, the buyers are expected to conduct their own negotiations to obtain the most favorable price.

Furthermore, the issuance of Decree of Head of LKPP 122/2022 introduced a more streamlined process, reducing the number of product listing phases from eight to two. While this simplification facilitates faster and easier product inclusion in the e-catalog, it also places greater responsibility on buyers to carefully select products, assess supplier qualifications, and negotiate prices. Conversely, this simplified procedure may also create opportunities for fraud in e-purchasing if adequate oversight and control mechanisms are not effectively implemented.

As part of the National Strategy for Corruption Prevention, particularly to strengthen preventive controls in public procurement, BPKP has introduced a monitoring feature within the e-catalog system, known as e-audit. This feature enables government internal auditors to detect anomalies in a timely manner. These anomaly indicators serve as valuable inputs for BPK in its role as the external auditor. In this context, internal auditors play a preventive role through continuous monitoring, while BPK evaluates whether these anomalies indicate weaknesses in governance, accountability, or internal controls.

BPK auditors rely on e-audit monitoring results to identify where fraud risks may exist within e-purchasing activities. By reviewing detected anomalies prior to commencing an audit, BPK auditors can determine which audit tests should be conducted and what supporting data need to be collected. Moreover, auditors can assess how entities respond to identified anomalies—whether they implement corrective measures, strengthen internal controls, or disregard the warning signals. However, auditors must exercise caution: anomaly detection functions as an early warning mechanism rather than definitive evidence of fraud. Such indicators signal potential irregularities that still require verification through substantive testing. Therefore, BPK must align its audit response with the type and objective of the audit to ensure that conclusions remain objective, evidence-based, and reliable. The potential anomalies and auditors’ respond may include:

This analysis aims to identify behavioral patterns of Procurement Officers (Pejabat Pengadaan/PP) and Commitment-Making Officers (Pejabat Pembuat Komitmen/PPK) by examining the ratio between the number of procurement packages and the number of unique suppliers involved. A disproportionately high ratio may suggest that procurement officials are concentrating transactions with a limited number of suppliers, potentially indicating conflicts of interest, preferential treatment, or collusion. For BPK, this anomaly highlights the importance of testing whether procurement entities adhere to fair competition principles and whether internal controls effectively prevent supplier concentration. Audit procedures may include reviewing vendor selection records, analyzing supplier diversity, and assessing whether procurement planning aligns with competition requirements.

This analysis monitors procurement packages completed within an unusually short period between the product’s initial listing and the finalization of the contract. Transactions executed within such compressed timeframes may indicate prearranged agreements between suppliers and procurement officials (PP/PPK) outside formal procurement procedures. In such cases, BPK auditors should perform detailed reviews of procurement documentation to verify whether evaluation, comparison, and negotiation processes were properly conducted. Data analytics can also be used to assess whether transaction speed is reasonable in relation to the complexity of the goods or services procured.

This analysis tracks procurement packages completed within a short interval between the creation of a purchase order and the contract signing. Such rapid status changesmay indicate insider knowledge or collusion. A particular concern observed through e-audit monitoring is the growing number of transactions completed in less than one hour, suggesting that contracts may be finalized without adequate review or negotiation. In response, BPK auditors should verify whether procurement officers complied with all procedural requirements, including supplier evaluation and price verification.

This analysis evaluates variations in product prices over a defined period. A sharp increase in price immediately

before a transaction—followed by a decrease afterward—may signal price manipulation or collusion between

suppliers and procurement officials. For BPK auditors, this anomaly requires testing the reliability of pricing

mechanisms, comparing price trends across suppliers, and assessing whether internal controls are capable of

preventing opportunistic or coordinated price adjustments.

Conclusion and Recommendation

This study demonstrates that anomaly detection in e-purchasing provides valuable early warning signals of potential fraud risks in public procurement. Although anomalies do not constitute direct evidence of fraud, they reveal systemic vulnerabilities that auditors must address through timely and evidence-based responses. Incorporating anomaly detection into risk-based audit planning may allow SAIs to shift from reactive investigation to proactive risk identification and triage.

The findings implies that the effective utilization of anomaly detection requires institutional, methodological, and capacity-related adjustments within SAIs. First, anomaly detection should be formally embedded in the audit planning and risk assessment frameworks to ensure that audit resources are allocated toward high-risk procurement activities. Second, SAIs should strengthen data collaboration with internal audit institutions and procurement regulators to enable real-time exchange of anomaly monitoring results. Third, enhancing auditors’ competencies in data analytics and digital audit tools is critical to ensure that anomaly indicators are correctly interpreted and effectively integrated into audit testing. Finally, SAIs can assume a strategic governance role by communicating systemic anomaly trends and control weaknesses to policymakers, thereby supporting continuous improvement of procurement systems.

BPKP. (2025). Pengawasan Intern E-Katalog dalam Mendukung Tata Kelola Pemerintahan yang Baik dan Bebas KKN.

Chornyi, K., Shilo, G., & Lebedieva-Dychko, A. (2025). Analysis of state register data to identify anomalies and corruption threats in tenders and procurements. CEUR Workshop Proceedings, 3974, 235–243.

Magakwe, J. (2023). The root causes of corruption in public procurement: A global perspective. In Corruption -New Insights. IntechOpen. https://doi.org/10.5772/intechopen.105941

Niessen, M. E. K., Paciello, J. M., & Fernandez, J. I. P. (2020). Anomaly detection in public procurements using the Open Contracting Data Standard. International Conference on EDemocracy and EGovernment, 127–134. https://doi.org/DOI: 10.1109/ICEDEG48599.2020.9096674

Rachman, S. J., & Alamsyah, W. (2023). Mapping fraud potentials in e-purchasing procurement in Indonesia (A. T.Husodo (ed.)). Indonesia Corruption Watch.